Auto Insurance for the Elderly: Complete Guide

Turning 65 doesn’t mean you have to accept higher insurance premiums without a fight. At Direct Insurance Services, we’ve helped countless seniors find affordable auto insurance coverage that actually fits their needs and budget.

This guide walks you through exactly why rates climb with age, what discounts you’re likely missing, and how Utah-specific factors affect your policy.

Why Auto Insurance Costs More for Seniors

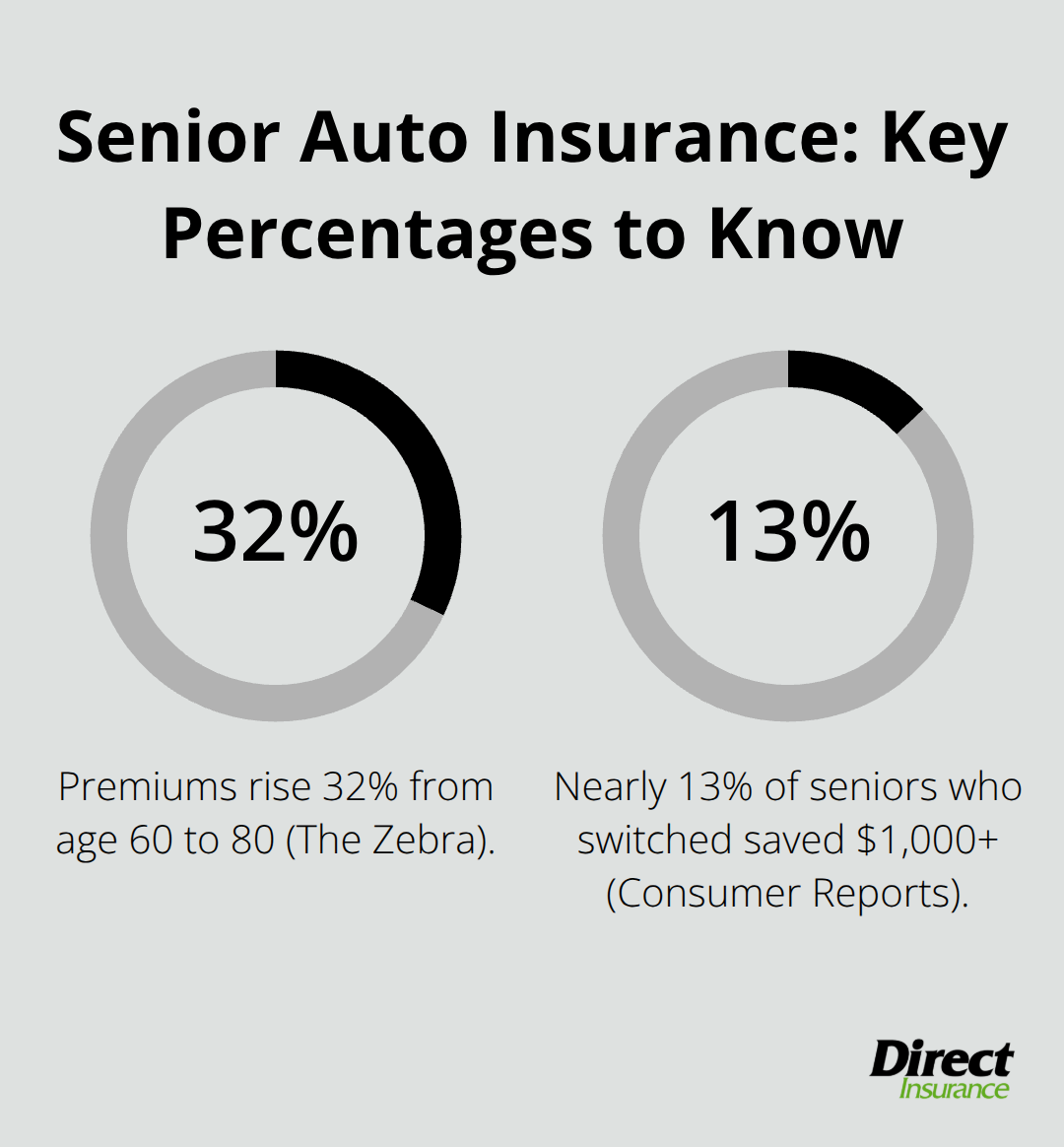

Insurance companies aren’t being arbitrary when they raise your rates after 65. The numbers tell a clear story that shapes how they price your policy. According to data from The Zebra, premiums for drivers at age 60 average around $1,934 annually, jumping to approximately $2,089 at age 70 and reaching $2,545 by age 80. That’s a 32% increase over two decades.

Progressive’s analysis from September 2023 through August 2024 shows a similar pattern: drivers aged 65 to 74 pay an average of $122.26 per year, while those 75 and older jump to $127.96. These aren’t random figures. Insurers base them on actuarial data showing that fatal crash rates per 100,000 licensed drivers increase significantly after age 74, according to the National Safety Council. Slower reaction times, vision changes, and medication interactions that can affect driving ability all factor into these calculations. Older drivers also sustain more severe injuries in crashes, which means higher medical payouts for insurers. Your state matters tremendously in how much this age factor affects you. In Ohio, premiums rise about 53% from age 60 to age 80, while Maine and North Carolina show almost no age-related increase at all. California, Hawaii, and Massachusetts actually ban age-based rating factors entirely, meaning your age alone cannot drive your premium up in those states.

The misconception that costs you the most money

The biggest myth seniors believe is that their clean driving record and lower mileage automatically protect them from rate increases. That’s backwards thinking that costs you money. Insurers acknowledge your good habits through discounts, but they don’t eliminate the base rate increase tied to age-related risk factors. A Consumer Reports survey of more than 40,000 policyholders found that senior drivers experienced higher rate increases in the past year than younger drivers, yet the same survey showed older drivers are involved in fewer fatal crashes per capita. This paradox exists because insurance pricing isn’t about your actual driving-it’s about statistical risk pools. You could drive 3,000 miles annually on perfect roads and still face the same age-based premium structure as someone commuting 30,000 miles.

Where shopping around actually saves you money

What actually works is shopping around. Among seniors who switched insurers in the past year, the median annual savings was $461, according to Consumer Reports. Nearly 13% saved $1,000 or more. That’s substantial money left on the table if you assume your current rate is locked in by your age.

The median annual car insurance premium for seniors sits just under $1,500, roughly the same as the median for all ages, which means rate differences between insurers can be dramatic. When you compare quotes from multiple carriers, you expose how differently each one prices your risk profile. Some insurers weight age more heavily than others. Some reward your low mileage more aggressively. Some offer senior discounts that others don’t. The only way to find these differences is to get quotes and compare them side by side. This comparison process becomes your next step toward finding coverage that actually reflects your driving situation rather than a generic age-based assumption.

Ways to Lower Auto Insurance Costs as a Senior

Defensive Driving Courses Deliver Immediate Savings

Defensive driving courses offer real savings that most seniors overlook. AARP provides an online defensive driving course specifically designed for older drivers, and completing an approved course typically qualifies you for a discount on your premiums. This discount applies immediately after you finish the course and provide proof of completion to your insurer. Defensive driving courses help reduce premiums for up to three years. The course itself costs around $15 to $20 and takes roughly four hours to complete online, which means you recover that cost in a single premium payment. Beyond the discount, the defensive driving training addresses the specific challenges seniors face: slower reaction times, vision changes, and managing medications that affect alertness. You gain practical strategies that reduce your actual crash risk, which is what insurers care about when they calculate your rates.

Bundling Policies Cuts Premiums Far More Aggressively

Bundling your auto insurance with home or renters coverage cuts your premiums far more aggressively than relying on age-based discounts alone. Combining auto and home policies typically saves 10% to 25% according to industry data, while adding renters coverage to auto can save 5% to 15%. If you own your home outright or carry a mortgage, this bundling option likely sits unused. Many seniors assume their current insurer offers the best bundle rates, but different insurers weight bundle discounts differently. Some carriers specialize in senior-focused pricing that makes bundling even more valuable. Compare top-rated auto and home insurance providers to expose these differences and find the insurer that rewards your specific situation most generously.

Usage-Based Programs Reward Your Actual Driving Habits

Usage-based insurance programs like Progressive Snapshot reward you directly for how you actually drive rather than guessing based on your age. These programs use telematics technology to monitor your driving habits, and if you drive safely with fewer miles, your premium drops accordingly. For seniors driving 5,000 miles annually or less, usage-based programs can offset the age-related premium increases entirely. You install a small device in your vehicle or use a mobile app, and the insurer tracks metrics like hard braking, rapid acceleration, and time of day you drive. Seniors who adjust their driving patterns by traveling during daylight hours and avoiding busy roads-habits Consumer Reports found most seniors already follow-see the biggest savings with these programs.

Vehicle Safety Features Lower Your Insurance Costs

Vehicle safety features matter more for your insurance costs than most seniors realize. Automatic emergency braking, blind spot warnings, rear cross-traffic warnings, and lane keeping assist all reduce crash likelihood, and insurers increasingly offer discounts for vehicles equipped with these systems. If you consider a new vehicle, prioritizing these safety features can lower your insurance costs over the life of the car while also reducing your actual crash risk. Rearview cameras and rear parking sensors, standard on all vehicles since 2018, specifically reduce backing accidents that are common among older drivers. Anti-theft devices and alarm systems also qualify you for modest discounts with some carriers, though the savings are typically smaller than safety feature discounts. These vehicle choices directly influence both your safety on Utah roads and the rates you pay for coverage.

Auto Insurance in Utah

Weather and Road Conditions Shape Your Coverage Needs

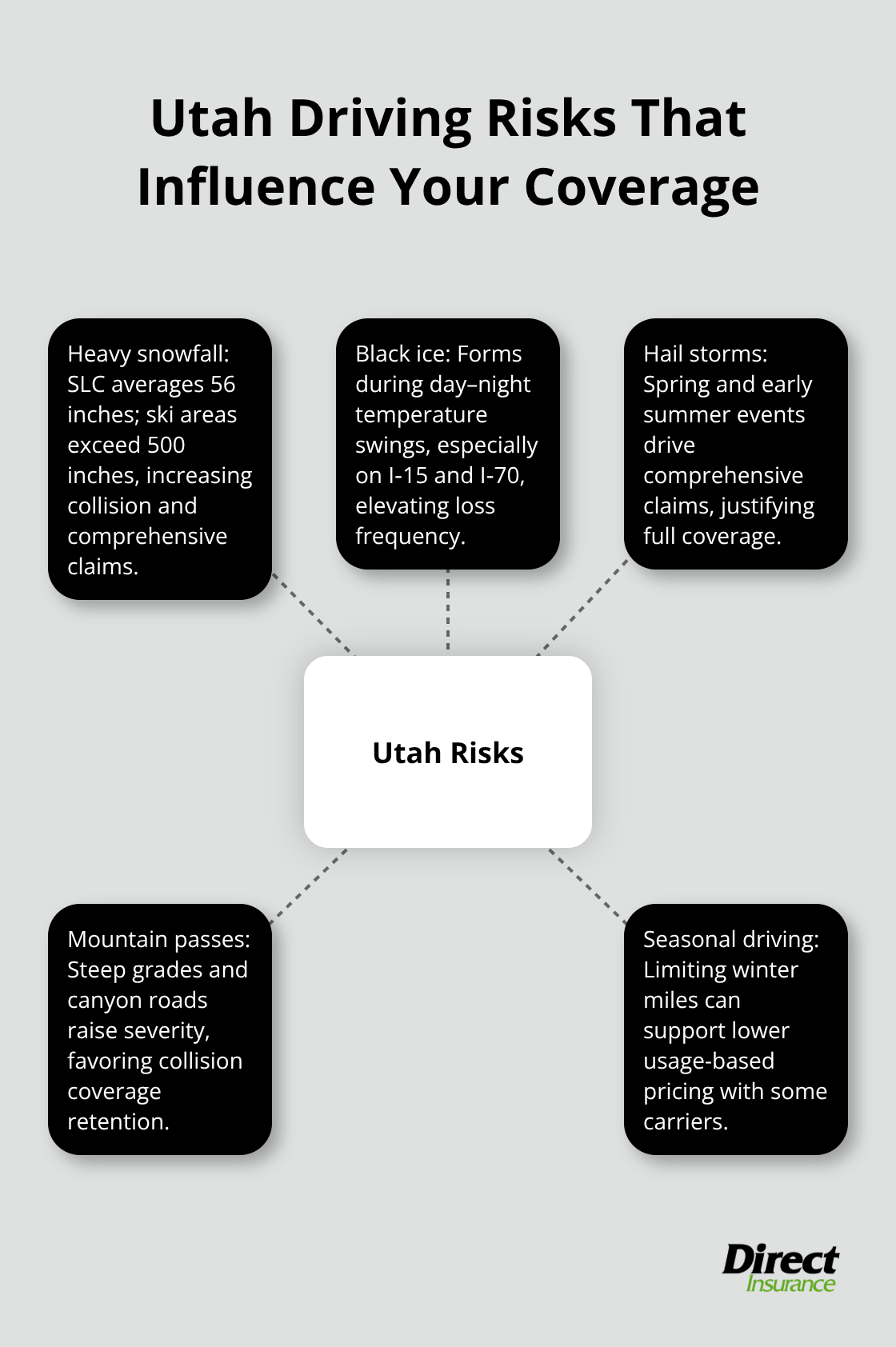

Utah’s weather and road conditions create specific insurance challenges that differ from national averages, and your policy must account for these regional realities. Winter driving across Utah’s mountain passes introduces hazards that significantly affect your insurance rates and coverage needs. Salt Lake City experiences an average of 56 inches of snow annually, with ski country areas like Alta and Snowbird receiving over 500 inches per year. Black ice forms unpredictably on Utah’s highways during temperature fluctuations between day and night, particularly on I-15 and I-70 corridors where seniors frequently travel. Hail storms occur regularly in spring and early summer across the Wasatch Front, causing comprehensive claim damage that justifies maintaining full coverage rather than reducing it to save money.

Older drivers adjust their driving patterns by avoiding busy roads and hazardous weather-habits that Utah seniors should formalize into your insurance strategy. If you restrict your winter driving or avoid peak travel times during storms, tell your insurer about these patterns because some carriers adjust rates based on seasonal mileage reduction. Utah’s specific road conditions also mean you should prioritize collision and comprehensive coverage over minimum liability limits, especially if you navigate mountain terrain or live outside Salt Lake City’s urban core. Dropping these coverages to reduce premiums exposes you to thousands in out-of-pocket repair costs when weather-related accidents occur, which they inevitably do in Utah.

Local Insurance Options and Utah-Specific Pricing

Local insurance options in Utah vary significantly in how they price senior drivers and what discounts they prioritize. Some carriers heavily weight Utah’s winter conditions into premiums, while others focus more on your individual driving record and habits. State requirements mandate minimum liability coverage of 25/65/15, meaning $25,000 per person and $65,000 per accident for bodily injury plus $15,000 for property damage, but these minimums leave you dangerously underinsured given Utah’s weather hazards and canyon roads.

Many seniors carry these minimum limits to reduce premiums, a false economy when a serious accident on I-80 through the mountains could result in liability claims exceeding $100,000. Uninsured and underinsured motorist coverage protects you against other drivers lacking adequate insurance, particularly important in Utah where many drivers carry only state minimums. Utah also allows you to stack uninsured motorist coverage across multiple vehicles if you own more than one car, a strategy that costs little but provides substantial protection.

Resources and Support for Utah Seniors

The Utah Division of Aging and Adult Services connects older drivers to transportation alternatives and safety programs that can reduce your actual driving frequency. AARP’s online defensive driving course remains available to Utah residents and qualifies you for discounts across most major carriers operating in the state. The Utah Department of Public Safety offers resources on age-appropriate driving and vehicle maintenance that directly reduce crash risk on Utah’s challenging roads. Taking advantage of these resources demonstrates to insurers that you actively manage risk, information you should communicate when obtaining insurance quotes.

Final Thoughts

Managing auto insurance for the elderly requires three concrete actions that directly reduce what you pay. Shop around every one to two years, compare quotes from at least three carriers, and expose how differently insurers price your profile-seniors who switched carriers saved a median of $461 annually, with some saving over $1,000. Claim every discount you qualify for, from defensive driving courses ($15 to $20 with three years of savings) to bundling auto with home or renters coverage (10% to 25% off) to usage-based programs that reward your actual driving habits.

Adjust your coverage strategy for Utah’s specific conditions rather than accepting state minimums that leave you underinsured. Winter driving, mountain terrain, and weather hazards justify maintaining collision and comprehensive coverage, while uninsured motorist protection matters more in Utah than national averages suggest. If you restrict winter driving or avoid peak traffic times, tell your insurer because some carriers adjust rates based on seasonal mileage reduction.

Auto insurance for the elderly doesn’t have to drain your retirement budget when you take control of your policy. We at Direct Insurance Services shop multiple top-rated insurance companies to find coverage that reflects your driving situation and budget rather than penalizing you solely for your age. Contact us today to get quotes from carriers that reward your safe driving habits and low mileage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation