Best Homeowners and Auto Insurance Companies

Finding the right homeowners and auto insurance companies takes more than just picking the cheapest option. You need coverage that actually protects your assets, customer service that responds when you need it, and rates that fit your budget.

At Direct Insurance Services, we’ve helped thousands of customers navigate these choices. This guide breaks down what separates the best insurers from the rest, so you can make a decision based on facts rather than guesswork.

What Makes Top Homeowners Insurers Stand Out

Coverage That Actually Protects Your Assets

Consumer Reports rated 28 homeowners insurers and found that only three earned their recommendation-a stark reminder that price alone doesn’t guarantee quality protection. The real difference between top performers and the rest comes down to three concrete factors: how well they handle claims, what coverage options they actually offer, and whether they’ll stick with you when disaster strikes. Top-rated insurers offer extended replacement cost coverage, which pays what it actually costs to rebuild rather than an arbitrary limit. Auto-Owners, Erie, and USAA all report complaint levels well below the national average according to NAIC complaint statistics, meaning when you file a claim, these companies process it without unnecessary delays or denials. Erie specifically offers accident forgiveness, gap insurance, and vanishing deductibles that reward you for claim-free years. State Farm bundles home and auto policies to save customers an average of 23% on premiums, translating to roughly $787 annually.

Why You Can’t Trust Loyalty to Your Current Insurer

The worst move you can make is staying loyal to an insurer simply because you’ve been with them for years. Consumer Federation of America data shows homeowners with the same insurer for five or more years experienced an average 24% premium increase over three years. Yet 83% of long-term customers reported rate increases, and many discovered they could cut costs by 30% or more by shopping competing quotes. When evaluating any homeowner insurer, verify they offer guaranteed or extended replacement cost coverage in your state, check their complaint history through NAIC filings, and confirm they write new policies in your area.

Allstate and State Farm have stopped accepting new homeowners customers in California, leaving many shoppers scrambling for alternatives.

Claims Handling Beats Discounts Every Time

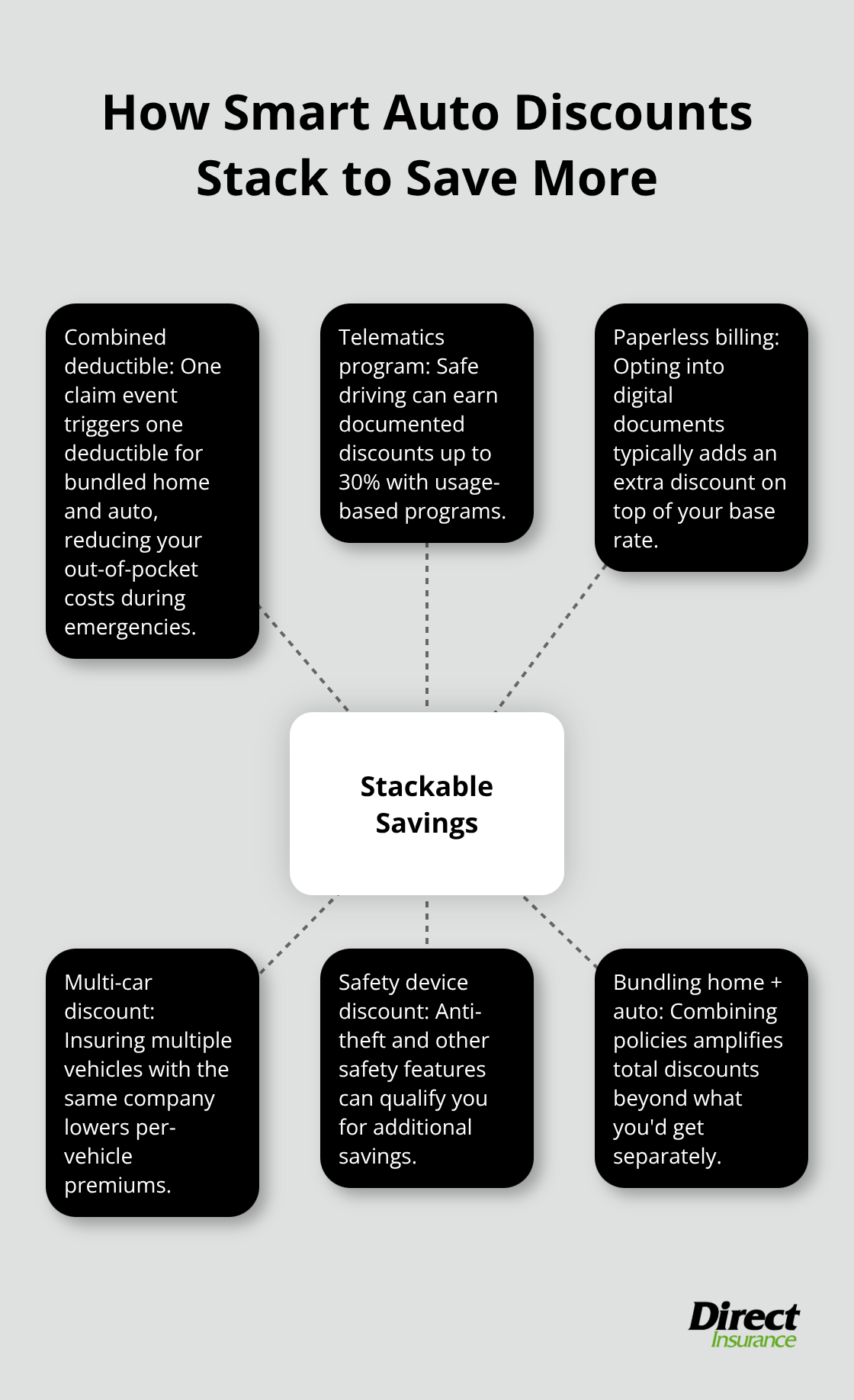

An insurer’s discount might save you $200 today, but poor claims handling costs you thousands when your roof leaks or pipes burst. Consumer Reports surveyed 23,917 policyholders and found that claims handling quality and policy clarity ranked among the top reasons customers switched insurers. NAIC complaint statistics show which insurers process claims efficiently and which ones deny legitimate claims or drag out settlements for months. When you compare quotes, ask each insurer specifically how they handle water damage claims and whether they offer replacement cost or actual cash value coverage. Replacement cost always costs slightly more but pays what you actually need to rebuild; actual cash value deducts depreciation, leaving you thousands short. Ask whether the insurer uses their own adjusters or third-party contractors, since in-house adjusters tend to process claims faster and more fairly than outside firms incentivized to minimize payouts. Progressive offers a combined deductible option for bundled policies, meaning if your home and car are both damaged in the same event, you pay one deductible instead of two-a feature that saves money when you need it most.

Shopping Multiple Quotes Reveals Hidden Savings

Most homeowners never compare quotes from more than one or two insurers, which means they miss substantial savings opportunities. When you request quotes from at least three providers, you’ll see how dramatically rates vary for identical coverage and deductibles. Some insurers charge 40% more than others for the same protection, yet many customers never discover this gap because they accept the first quote they receive. The companies that stand out typically offer multiple discounts (security devices, bundling, paperless billing) that stack together to reduce your final premium. An independent agency approach shops multiple top-rated insurance companies to help clients find the best coverage at competitive rates-an approach that reveals options you won’t find by contacting insurers directly.

Which Auto Insurers Deliver Real Value Beyond Low Rates

Top Performers in the 2026 Auto Insurance Market

The auto insurance market has stabilized compared to the chaos of 2023 and 2024, but that doesn’t mean all insurers are equal. NerdWallet’s January 2026 analysis ranks Travelers as the top car insurer overall, with Amica and State Farm also performing well for most drivers, while USAA excels specifically for military members and veterans. The critical difference isn’t just the monthly premium you pay today-it’s what happens when you need to file a claim. Travelers ranks number one for bundling home and auto policies and offers eco-friendly discounts for hybrid vehicles and green home materials, which compounds your savings when you combine policies.

Bundling Delivers Substantial Savings Most Drivers Miss

Amica leads for homeowners coverage and delivers up to 30% off when bundling, though auto premiums can run higher than competitors, making bundling especially valuable for Amica customers. State Farm bundles can save you around $1,356 annually, with their Drive Safe & Save telematics program delivering discounts up to 30% for drivers who maintain safe habits. Auto-Owners consistently shows the lowest complaint levels among bundled policies according to NAIC data and costs roughly $1,878 per year for bundled coverage, making it the cheapest option among large insurers. These numbers matter because bundling home and auto cuts total premiums by up to 40% according to NerdWallet’s 2026 analysis, yet many drivers miss this savings simply because they don’t request bundled quotes.

Digital Tools and Discount Stacking Separate Winners from the Rest

Progressive offers a combined deductible option for bundled policies, meaning one claim event triggers one deductible instead of two-a practical feature that saves real money during emergencies. State Farm’s Drive Safe & Save telematics program tracks your actual driving behavior and rewards safe habits with documented discounts reaching 30%, unlike vague promises from competitors. When comparing auto insurers, ask whether they offer paperless billing discounts, multi-car discounts, and safety device discounts, since these stack together and reduce your final premium far more than a base rate ever will.

How to Find Your Best Rate and Coverage Combination

The mistake most drivers make is comparing only the advertised rate without asking about discount combinations that apply to their specific situation. An independent agency approach shops multiple top-rated insurers simultaneously to reveal which company offers the best combination of base rate, available discounts, and bundling opportunities for your exact profile-an approach that typically saves customers 15% to 25% compared to calling insurers individually. This comparison process becomes even more important when you factor in coverage options, since the cheapest quote often excludes features you actually need.

How to Select Insurance That Matches Your Real Situation

Document Your Home’s True Replacement Cost

Start with what you actually own and what could go wrong. For homeowners, this means calculating your home’s actual replacement cost, not its market value. A $400,000 house in Salt Lake City might cost $550,000 to rebuild due to labor and material inflation. If you insure for $400,000, you’ll face substantial out-of-pocket costs after a total loss. Construction costs continue rising from supply chain disruptions and labor constraints, pushing rebuild expenses higher each year. When you request quotes, specify the exact dwelling limit that matches your replacement cost, not what you paid for the property.

Determine Your Auto Coverage Based on Your Assets

Your auto insurance coverage needs depend on your vehicle’s age, your assets, and your liability exposure. A driver with $200,000 in savings should carry higher liability limits than someone with minimal assets, since liability coverage protects you when you’re found at fault and the other party sues. Most drivers carry 100/300/100 liability limits, but you should carry 250/500/100 or higher if you own a home or have significant savings. For deductibles, ask yourself whether you can afford a $1,000 deductible or if $500 makes more sense for your budget. The difference between a $500 and $1,000 deductible often amounts to only $100 annually, making the lower deductible a better value for many households.

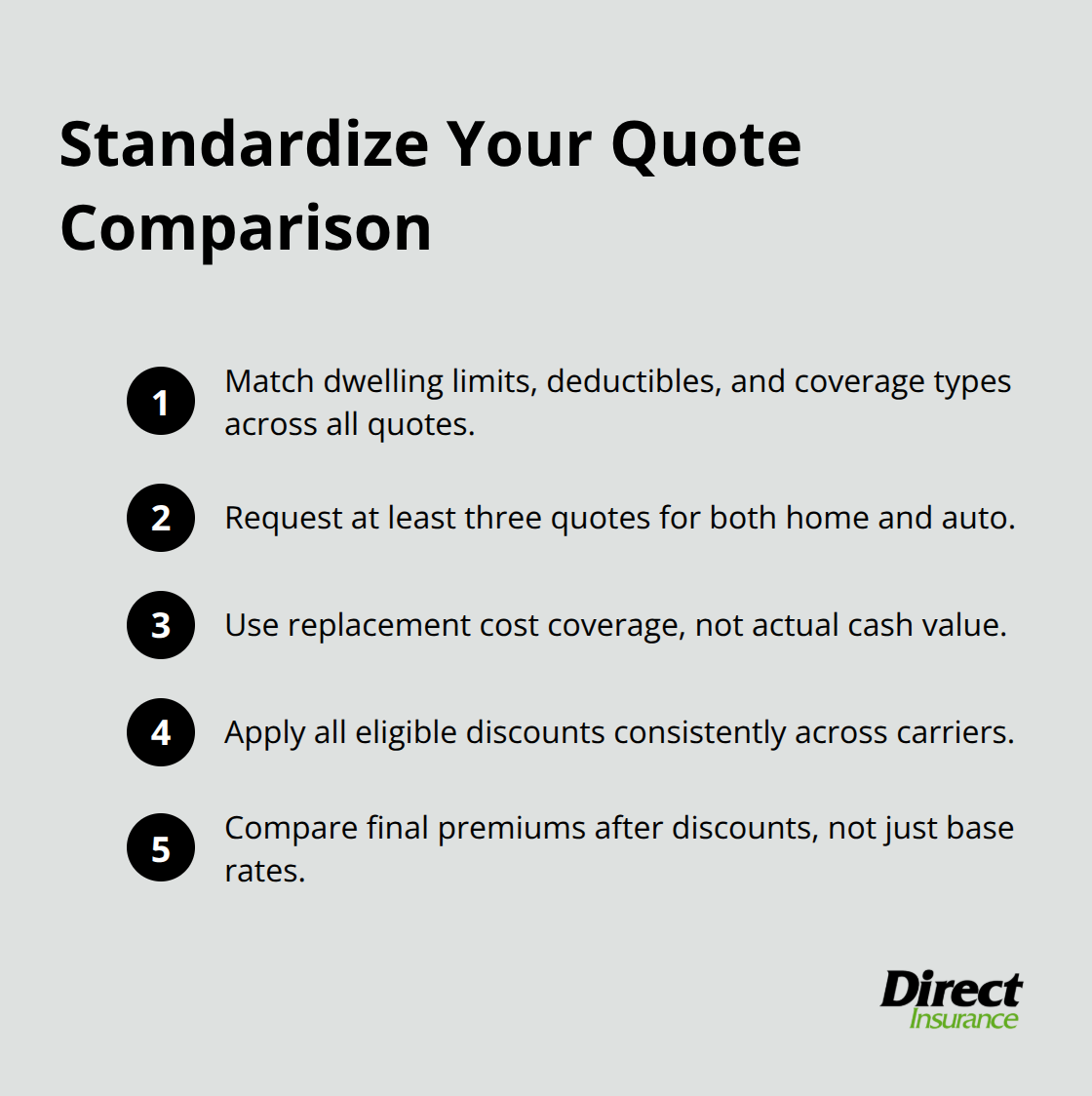

Request Identical Coverage Across All Quotes

Comparing quotes requires identical coverage across all providers-a step most people skip and then wonder why one quote seems cheaper. When you request quotes, specify the exact same dwelling limit, deductible, and coverage types (replacement cost, not actual cash value) for every company. Obtain quotes from at least three insurers for both home and auto, then stack the discounts each company offers. Security system discounts, bundling, paperless billing, and multi-car discounts often combine to reduce your final premium by 20% or more.

Prioritize Claims Handling Over Price Alone

Customer reviews matter, but read them strategically. An insurer’s discount might save you $200 today, but poor claims handling costs you thousands when your roof leaks or pipes burst. When you compare quotes, ask each insurer specifically how they handle water damage claims and whether they offer replacement cost or actual cash value coverage. Replacement cost always costs slightly more but pays what you actually need to rebuild; actual cash value deducts depreciation, leaving you thousands short.

Shop Multiple Insurers to Reveal Your Best Options

Direct Insurance Services shops multiple top-rated insurers for clients in Utah, comparing coverage options and discount combinations to reveal which company delivers the best protection at the lowest cost for your specific situation. This approach typically saves customers 15% to 25% compared to requesting individual quotes directly from insurers. Most drivers and homeowners never compare quotes from more than one or two companies, which means they miss substantial savings opportunities. When you request quotes from at least three providers, you’ll see how dramatically rates vary for identical coverage and deductibles. Some insurers charge 40% more than others for the same protection, yet many customers never discover this gap because they accept the first quote they receive.

Final Thoughts

Selecting the best homeowners and auto insurance companies requires three concrete decisions: comparing coverage options across multiple insurers, prioritizing claims handling over discounts alone, and verifying that your protection matches your actual assets and replacement costs. Drivers and homeowners who shop only one or two quotes miss savings of 15% to 25%, while those who accept renewal offers without comparison face rate increases averaging 24% over three years. Your loyalty to an insurer does not protect you; only accurate coverage limits and reliable claims handling do.

The insurance market in 2026 rewards shoppers who request identical quotes from at least three providers and ask specific questions about how each company handles water damage, what discounts stack together, and whether they write new policies in your state. Top performers like State Farm, Amica, Erie, and Auto-Owners consistently deliver strong claims handling and competitive rates, but the best choice for your situation depends entirely on your home’s replacement cost, your vehicle’s value, your assets, and the discounts you actually qualify for. Local expertise matters because we at Direct Insurance Services understand the specific risks of living in Utah-from wildfire exposure to winter weather damage to the unique liability concerns of our communities.

Rather than calling multiple insurers individually and comparing spreadsheets yourself, contact Direct Insurance Services to let our team shop the best homeowners and auto insurance companies on your behalf. We compare coverage options, discount combinations, and bundling opportunities across top-rated carriers to reveal which company delivers the protection you need at the lowest cost for your exact situation. Your next step is simple: reach out to discuss your coverage needs and let us handle the comparison work.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation