Home Insurance for Condos: Complete Coverage Guide

Condo owners often assume their HOA’s master policy covers everything. It doesn’t.

At Direct Insurance Services, we’ve seen too many condo residents face unexpected gaps in their coverage. Home insurance for condos requires a different approach than standard homeowners policies, and understanding those differences can save you thousands in potential losses. This guide walks you through exactly what you need to protect your investment.

What Makes Condo Insurance Different from Homeowners Insurance

Master Policy Coverage Provided by the HOA

Your condo association’s master policy protects the building structure and common areas, but it stops at your unit’s interior walls. The master policy covers the roof, exterior walls, hallways, elevators, and shared spaces. It does not cover your personal belongings, interior improvements you’ve made, or liability if someone gets injured inside your unit. According to the Insurance Information Institute, most master policies exclude interior renovations, fixtures, appliances, and interior walls entirely. This means if you’ve upgraded your kitchen cabinets, installed new flooring, or replaced countertops, those improvements become your responsibility to insure.

The master policy also typically carries a deductible that can range from $1,000 to $5,000 or higher. If the association files a claim for damage to common areas, you could face an assessment for your portion of that deductible through a special HOA levy. This is where loss assessment coverage becomes critical. Standard condo policies offer loss assessment limits of $1,000 to $2,000, but if your HOA has a high deductible or faces a major claim, you could owe significantly more out of pocket.

Individual Coverage Gaps You Need to Fill

Your furniture, electronics, clothing, and other belongings inside your unit remain completely unprotected by the master policy. A standard condo insurance policy provides personal property coverage using named perils, which means it covers specific events like fire, theft, wind, and hail. The typical deductible for personal property claims is $500 to $1,000, meaning you pay that amount before insurance kicks in.

NerdWallet’s analysis shows that personal property coverage amounts directly impact your premium. If you own high-value items like jewelry, art, or expensive electronics, standard personal property coverage may not be enough. These items often have sub-limits within your policy, typically capping out at $2,500 per item. You’ll need to schedule these valuables separately on your policy to get full replacement cost coverage.

Personal Property Protection Requirements

The key decision involves choosing replacement cost coverage instead of actual cash value. Replacement cost reimburses you for what it costs to replace an item today, while actual cash value deducts depreciation. After a claim, replacement cost coverage ensures you can actually replace what you lost rather than receiving a reduced payout. Understanding these distinctions between coverage types sets the stage for selecting the right policy limits and endorsements that match your specific condo situation.

Types of Coverage You Need for Your Condo

Dwelling Coverage for Interior Improvements

Interior improvements you make to your condo need dedicated coverage because the HOA’s master policy won’t reimburse you for them. Dwelling coverage for your unit-sometimes called walls-in coverage-protects the fixtures, flooring, cabinetry, and permanent upgrades inside your four walls. If you install hardwood floors, replace kitchen appliances, or upgrade bathroom tiles, these improvements represent real money that disappears in a fire or water damage event without proper coverage. The Insurance Information Institute emphasizes that most master policies explicitly exclude these interior components, making your individual policy the only protection you have.

When you set your dwelling coverage limit, add up the cost of everything you’ve installed or upgraded since buying your condo. Many condo owners underestimate this amount and end up with insufficient limits that won’t fully rebuild their unit after a major loss.

Personal Liability and Medical Payments Protection

Personal liability coverage protects you when someone gets injured inside your condo and sues you for damages. A guest slips on your freshly waxed floor, or your visitor’s child breaks a tooth on something in your kitchen-these situations expose you to liability claims that can reach hundreds of thousands of dollars. Try starting with at least $300,000 in liability coverage, though higher limits like $500,000 make sense if you have significant assets to protect.

Medical payments coverage is separate from liability and pays small injury-related expenses without requiring a lawsuit, typically covering up to $5,000 per person. This coverage prevents minor incidents from becoming legal battles and shows good faith when someone gets hurt on your property.

Loss Assessment Coverage for Special Expenses

Loss assessment coverage functions as a financial safety net when your HOA faces unexpected costs that exceed their master policy limits. If the association’s master policy has a $5,000 deductible and a major roof failure costs $50,000 to repair, you could face an assessment of $5,000 or more as your share of that deductible. Standard loss assessment coverage provides $1,000 to $2,000 in protection, but this amount often falls short in real-world scenarios.

Carriers like Travelers and USAA offer higher loss assessment limits-up to $50,000 in some cases-which provides genuine security against surprise HOA levies. Calculate your potential exposure by reviewing your HOA’s master policy deductible and asking about recent special assessments or planned major repairs to the building. Understanding these three coverage types positions you to make informed decisions when comparing policies from different insurers.

How to Choose the Right Condo Insurance Policy

Request Your HOA’s Master Policy Document

Start by requesting your HOA’s master policy document directly from the association office. This single step separates condo owners who obtain proper coverage from those who overpay or underpay. Your master policy statement shows property limits, liability insurance limits, common areas coverage, and expiration dates. Many condo owners skip this step and purchase coverage based on guesses about what their HOA provides. Read the declarations page and coverage sections carefully, or ask your insurance agent to review it with you. Once you understand the master policy’s scope, you’ll know precisely what coverage gaps your individual policy must fill.

Compare Quotes from Multiple Insurers

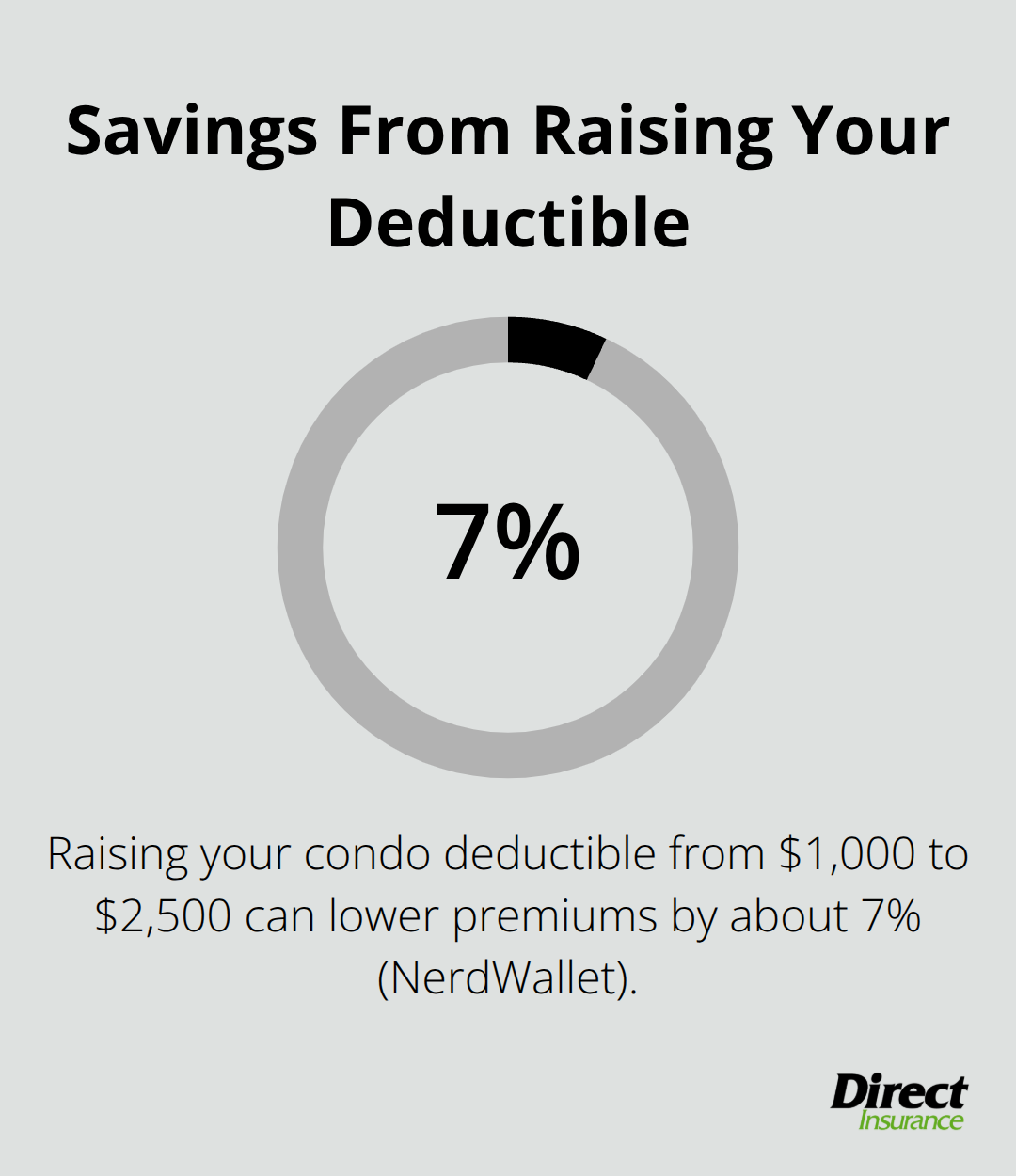

After reviewing your master policy, obtain quotes from at least three different insurers using identical coverage amounts and deductibles for accurate comparison. NerdWallet’s analysis of more than 450 million insurer rates shows State Farm averages around $360 per year while American Family runs about $835 annually for similar coverage, demonstrating that carrier selection dramatically impacts your cost. Allstate, Travelers, and Nationwide average between $460 and $645 per year. Request quotes that include the same personal property limit (NerdWallet data shows $50,000 costs roughly $490 annually while $100,000 reaches about $645), the same deductible, and the same liability limit so you compare apples to apples. Ask each insurer about their specific discounts-bundling auto and condo insurance typically saves 10 to 25 percent, while installing smoke detectors and security systems can reduce premiums further. Higher deductibles also cut costs noticeably; raising your deductible from $1,000 to $2,500 saves approximately seven percent according to NerdWallet.

Find affordable home insurance without sacrificing coverage by exploring smart strategies to reduce premiums.

Calculate Your Coverage Needs and Verify Requirements

Once you have quotes in hand, calculate your actual coverage needs by inventorying your belongings and adding up interior improvements. Your liability coverage should at minimum equal your net worth, though $300,000 to $500,000 provides solid protection for most condo owners (this range accounts for varying asset levels across different households). Verify that your mortgage lender and HOA both approve the coverage limits before purchasing, since both typically enforce minimum requirements that your policy must meet. Contact your lender’s insurance department and your HOA board to confirm their specific thresholds, ensuring your selected policy satisfies all external requirements.

Final Thoughts

Condo insurance operates fundamentally differently from standard homeowners policies because your HOA’s master policy only protects the building structure and common areas. Your personal belongings, interior improvements, and liability exposure remain entirely your responsibility, which means you cannot rely on assumptions about what the master policy covers. You must actively review that document, identify the gaps, and purchase individual coverage that fills those specific holes.

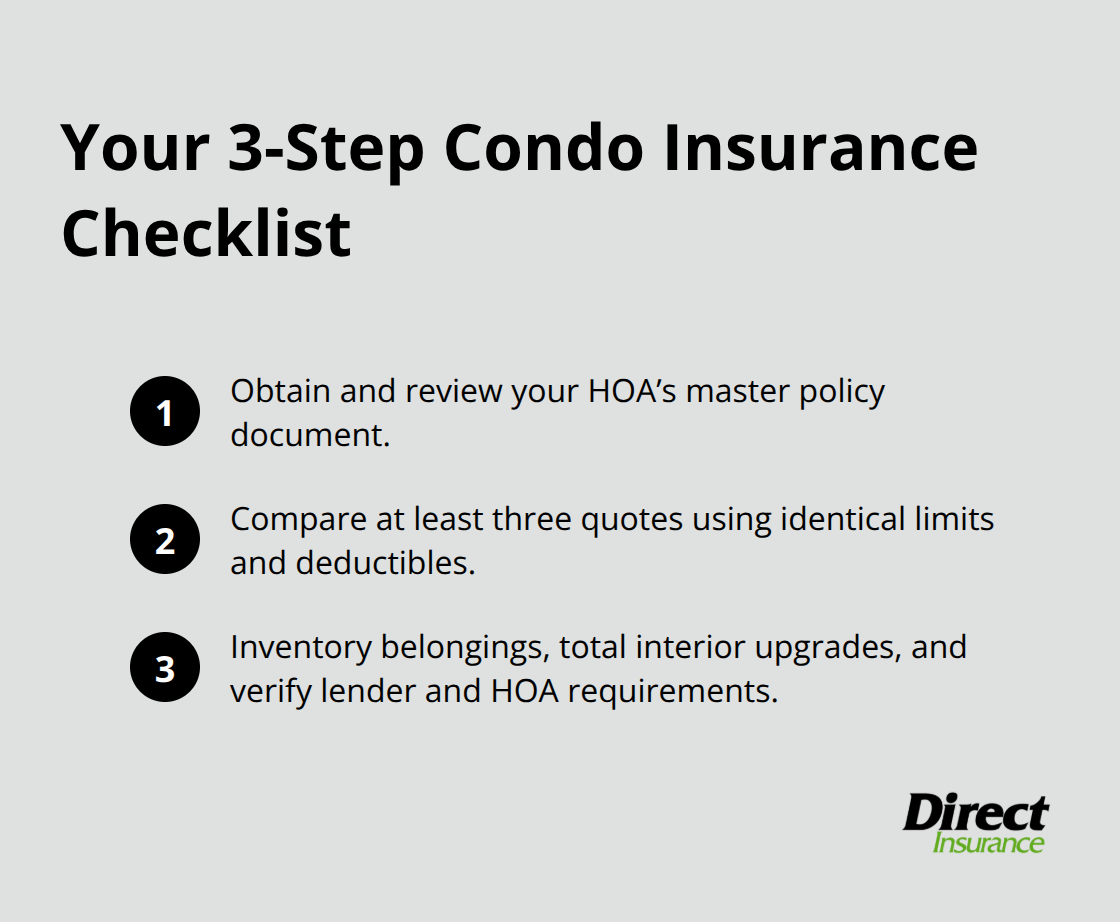

Getting properly insured requires three concrete steps that take control of your protection. First, obtain your HOA’s master policy document and review it carefully to understand exactly what remains uninsured. Second, compare quotes from at least three different carriers using identical coverage limits and deductibles so you see real price differences. Third, calculate your actual coverage needs by inventorying belongings and interior improvements, then verify that your selected policy meets both your lender’s and HOA’s minimum requirements (this final verification prevents costly coverage disputes down the road).

Home insurance for condos demands more attention than standard homeowners coverage because the responsibility for protection splits between two policies. At Direct Insurance Services in Salt Lake City, our team specializes in helping condo owners navigate these complexities and find coverage that actually protects their situation. Contact us today to review your condo insurance needs and receive a personalized quote that addresses your specific gaps.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation