Liability Bodily Injury Auto Insurance Explained

A car accident can happen in seconds. If you’re at fault and someone gets injured, you could face medical bills, lost wages claims, and lawsuits that drain your savings.

Liability bodily injury auto insurance protects you from these financial disasters. At Direct Insurance Services, we help drivers understand their coverage options so they can make informed decisions about the protection they actually need.

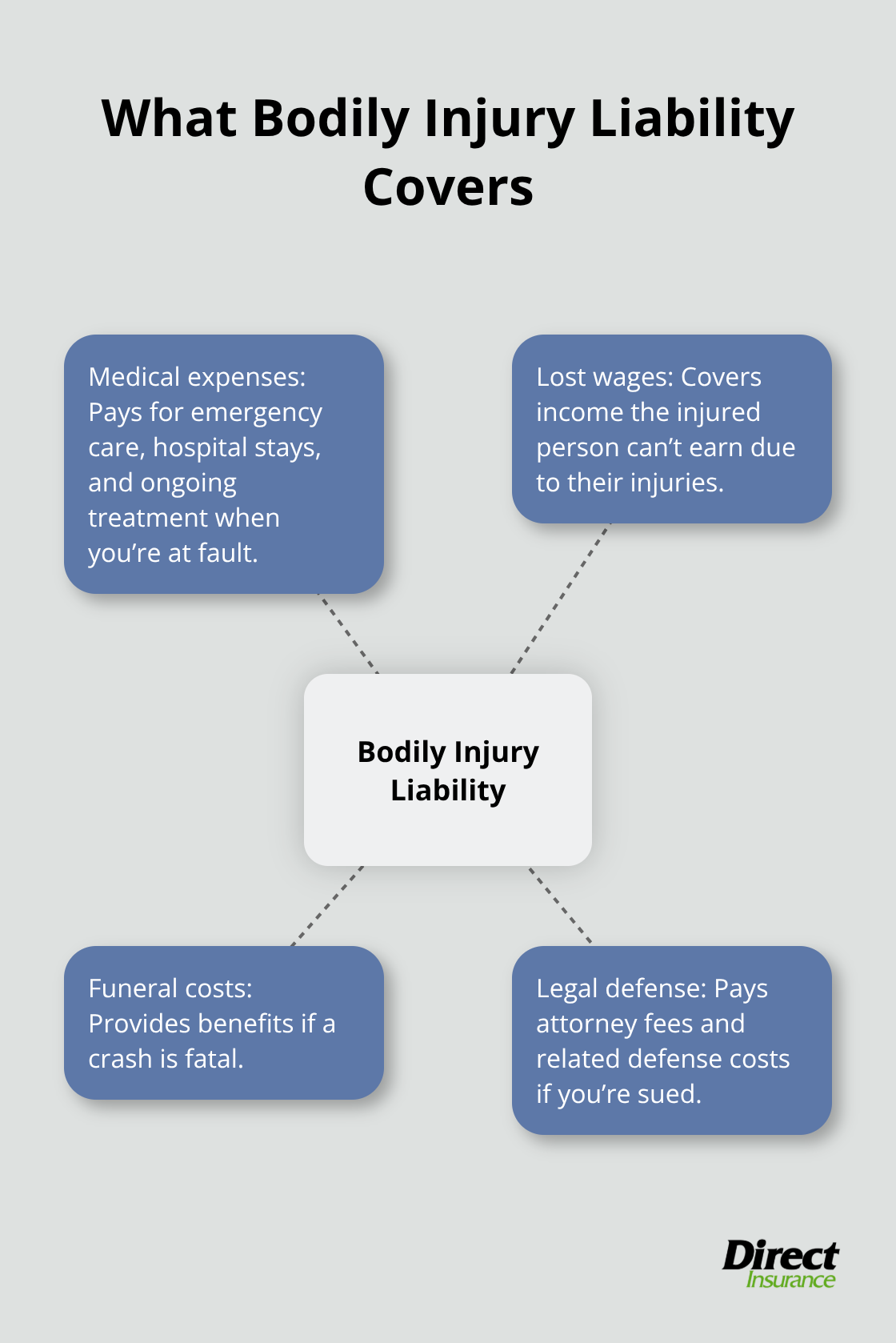

What Bodily Injury Liability Actually Covers

Bodily injury liability is the part of your auto insurance that pays for injuries you cause to other people when you’re at fault in a crash. It covers medical expenses for the injured party, including emergency care, hospital stays, and ongoing treatment. It also pays for lost wages if the injured person can’t work due to their injuries, funeral costs if the accident is fatal, and legal defense fees if you’re sued.

This coverage does not apply to your own injuries-that’s what medical payments coverage or Personal Injury Protection handles. Nearly every state requires bodily injury liability as a minimum, though the amount varies. New York, for example, is a no-fault state where you file bodily injury claims through your own Personal Injury Protection rather than pursuing the other driver’s liability, but you still need bodily injury coverage to protect yourself if you’re found at fault.

Understanding Your Coverage Limits

Bodily injury limits appear on your policy as two numbers in a per-person/per-accident format, like 25/50 or 100/300. The first number is what the insurer pays to any single injured person, and the second is the maximum they’ll pay total for all injuries from that one accident. With 25/50 limits, you’d pay up to $25,000 per person and $50,000 total per accident.

State minimums often fall well short of real medical costs-a serious injury requiring surgery and months of rehabilitation can easily exceed $100,000. Progressive recommends choosing limits at least equal to your net worth to protect your assets from lawsuits. If your net worth exceeds $500,000, an umbrella policy adds another layer of protection beyond your standard liability limits. Most drivers significantly underestimate how much coverage they need, which is why upgrading from state minimums to 100/300 or higher is common advice.

When Claims Get Filed

When someone files a bodily injury claim against your policy, your insurer investigates the accident, reviews medical records, and determines liability. If you’re found responsible, the insurer pays the injured party’s medical bills up to your coverage limits and handles legal defense if a lawsuit follows. The process typically takes weeks to months depending on claim complexity.

If multiple people are injured, the per-accident limit divides among them-if you have 100/300 limits and two people are injured, the insurer might pay $100,000 to each person up to the $300,000 total, or adjust payouts to stay within that cap. This is why adequate limits matter: insufficient coverage leaves injured parties undercompensated and can result in them suing you personally for damages beyond your policy limits. Understanding how these limits work in real accidents helps you make the right choice about the protection you actually need.

Why Bodily Injury Liability Matters

A serious car accident can cost far more than your savings account can handle. Medical treatment for severe injuries runs into six figures quickly-a single hospitalization with surgery and rehabilitation often exceeds $150,000, and that’s before accounting for lost wages or legal fees. Bodily injury liability protects your personal assets when you’re responsible for injuring someone and ensures that injured parties receive the compensation they need for medical expenses, lost wages, and other damages. Without adequate coverage, a lawsuit can attach your wages, freeze your bank accounts, and force you to sell property to pay damages. State minimum limits like 25/50 or 30/60 offer almost no real protection because they barely cover initial emergency care, let alone ongoing treatment or compensation for pain and suffering. One accident where you’re at fault can follow you financially for years, which is why bodily injury liability isn’t optional-it’s essential risk management.

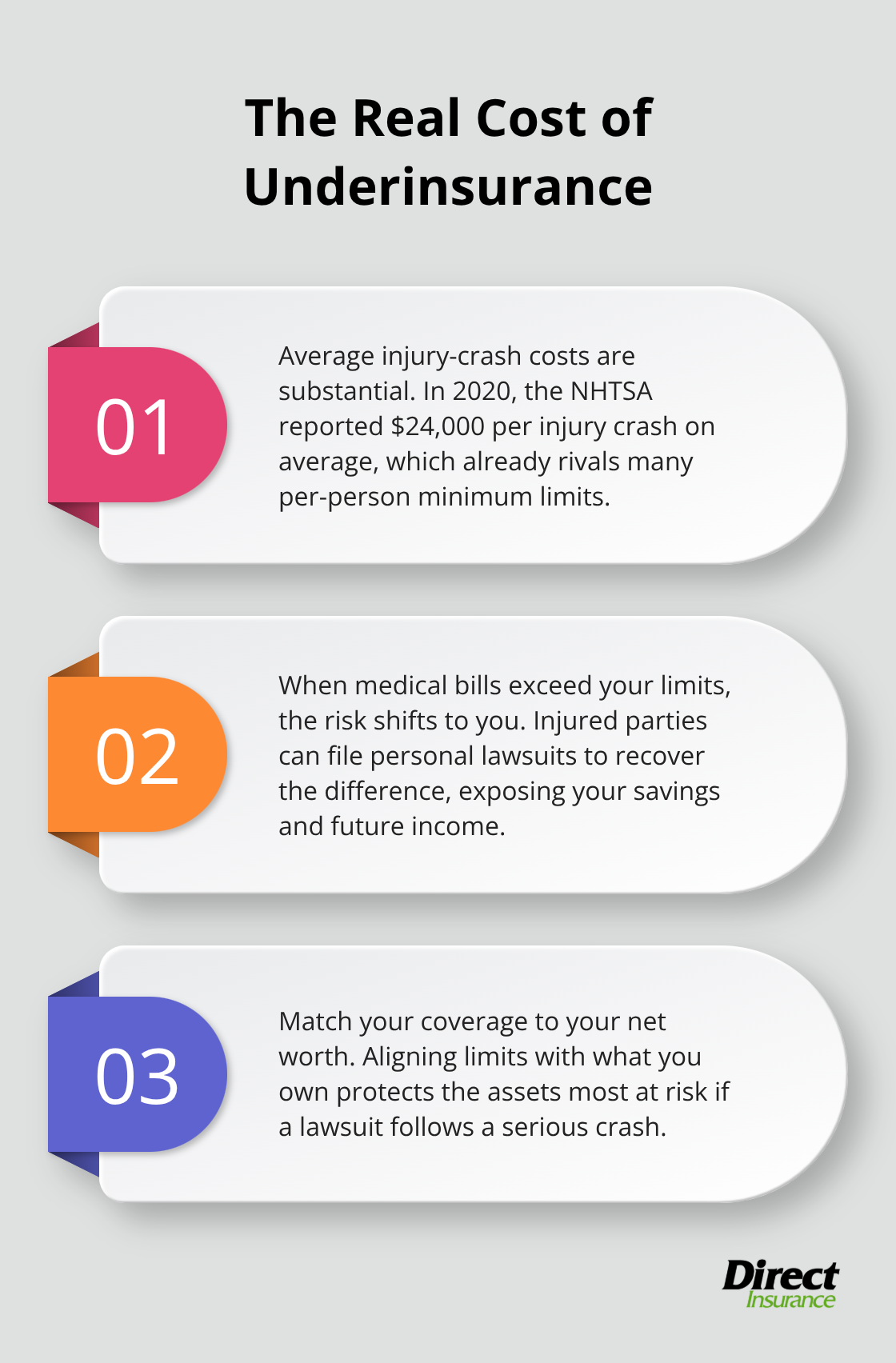

The Real Cost of Underinsurance

Most drivers carry state minimums because they’re cheaper upfront, but this creates massive exposure. The National Highway Traffic Safety Administration found that the average cost of a crash involving injury was $24,000 in 2020, yet many policies cap coverage at $25,000 per person. When medical bills exceed your limits, injured parties pursue personal lawsuits against you directly. Progressive recommends setting bodily injury limits equal to your net worth because that’s what’s at stake in a lawsuit.

If you own a home worth $400,000 and have $150,000 in retirement savings, your net worth is $550,000-yet a 25/50 policy leaves you vulnerable to losing it all. The cost difference between 25/50 and 100/300 limits is modest for most drivers, typically $30 to $50 per six-month term, but the financial protection is exponentially greater. Upgrading to higher limits is one of the best decisions you can make for your financial security.

Long-Term Liability and Your Future

Bodily injury claims don’t always settle quickly, and court judgments can follow you for years. A settlement or judgment for catastrophic injuries might include structured payments over a decade or more, meaning your liability exposure extends far beyond the accident date. If you’re sued and lose, wage garnishment can continue until the judgment is paid in full. This affects your ability to borrow money, refinance your home, or make major purchases. Uninsured or underinsured motorist coverage helps when someone else hits you, but it doesn’t protect you when you’re at fault. The only real protection is carrying bodily injury limits high enough to cover worst-case scenarios. As your assets grow-through home equity, retirement savings, or business ownership-your bodily injury limits should grow with them. Many people increase their coverage when they buy a home or reach certain financial milestones, which is smart planning. Your bodily injury limits should reflect your actual financial exposure, not just what the state requires.

How to Choose the Right Coverage Limits

Calculate Your Net Worth First

Your net worth determines how much bodily injury coverage you actually need, and most drivers miscalculate this figure. Progressive recommends setting bodily injury limits equal to your net worth because that’s exactly what you stand to lose in a lawsuit. Start by adding up your assets: bank accounts, retirement savings, home equity, and any investments. Then subtract your debts: mortgage balance, car loans, credit cards, and other liabilities. If you own a home worth $350,000 with a $200,000 mortgage, plus $80,000 in retirement savings and $15,000 in a checking account, your net worth is roughly $245,000. A 25/50 policy leaves you exposed to losing nearly all of it if you cause a serious accident.

Why Upgrading Makes Financial Sense

Upgrading to 100/300 coverage limits typically costs $30 to $50 per six-month term, which amounts to $60 to $100 annually for protection of an extra $75,000 per person and $250,000 per accident. That’s exceptional value considering a single serious injury claim can exceed $200,000 before accounting for lost wages or legal fees. Young drivers and those with significant assets should treat 100/300 as a baseline, not an upgrade. The math is straightforward: you pay a small premium increase to protect substantially more of your wealth.

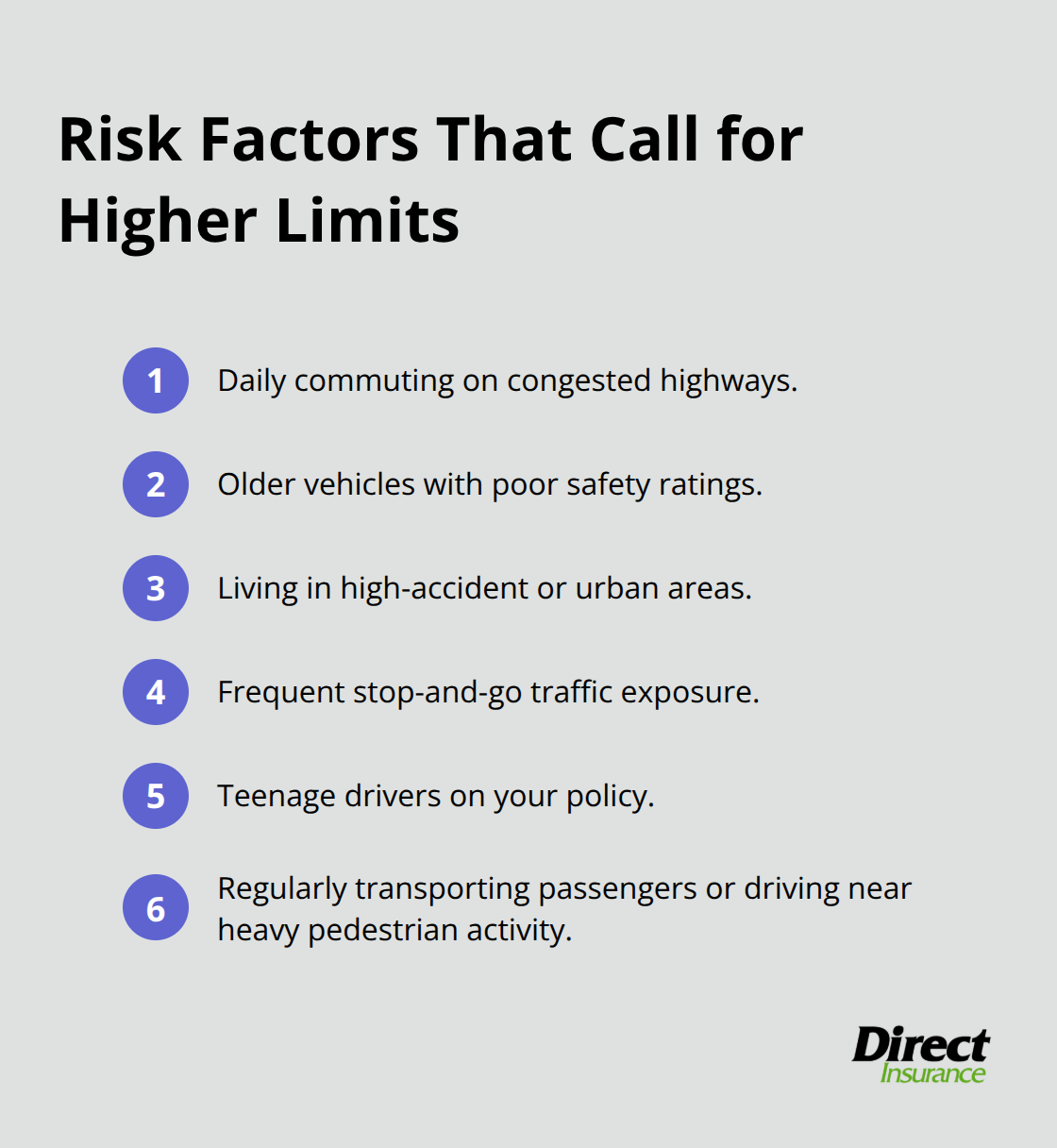

Assess Your Personal Risk Profile

Your actual risk profile matters significantly, and some drivers need even higher limits. If you commute on congested highways daily, drive older vehicles with poor safety ratings, or live in areas with high accident rates, you expose yourself to more claims. Urban drivers in dense traffic face statistically higher accident frequencies than rural drivers.

If you have teenage drivers on your policy, accident risk increases substantially since drivers under 20 have crash rates nearly three times higher than drivers aged 20 to 24. Similarly, if you regularly transport passengers, passengers in other vehicles, or drive in areas with significant pedestrian traffic, your liability exposure multiplies. These factors should push you toward higher limits, possibly 250/500 or even umbrella coverage.

Compare Quotes From Multiple Insurers

Getting quotes from multiple insurers reveals the actual cost difference in your specific situation. Some insurers charge minimal premiums for moving from 100/300 to 250/500, while others charge substantially more. The only way to know your true options is to compare actual quotes side by side rather than guessing based on general advice. When you shop multiple top-rated insurance companies, you see exactly what different limits cost before you decide on coverage.

Final Thoughts

Bodily injury liability auto insurance protects your financial future when you cause an accident that injures someone. Your coverage limits should reflect your actual assets and risk exposure, not just what your state requires. State minimums like 25/50 offer virtually no protection against real medical costs, which routinely exceed $100,000 for serious injuries, while upgrading to 100/300 costs only $30 to $50 per six months but shields substantially more of your wealth from lawsuits.

Calculate your net worth by adding what you own and subtracting what you owe, then set your bodily injury limits accordingly. If you own a home, have retirement savings, or earn a solid income, state minimums leave you dangerously exposed (a single accident where you’re at fault can result in wage garnishment, frozen bank accounts, and years of financial recovery). The modest premium increase for higher limits represents one of the smartest financial decisions you can make.

Contact Direct Insurance Services to review your current limits and explore options that match your actual financial exposure. We compare quotes from different insurers so you see exactly what various coverage levels cost before you decide. Our team helps you find the right balance between cost and protection for your liability bodily injury auto insurance needs.