Airbnb Insurance Coverage for Hosts A Must-Read

Hosting on Airbnb brings unique insurance challenges that standard homeowners policies don’t address. Property damage from guests and liability claims create significant financial risks.

We at Direct Insurance Services see hosts facing coverage gaps that could cost thousands. Understanding Airbnb insurance coverage for hosts protects your investment and peace of mind.

What Insurance Risks Do Airbnb Hosts Actually Face?

Property Damage Beyond Normal Wear and Tear

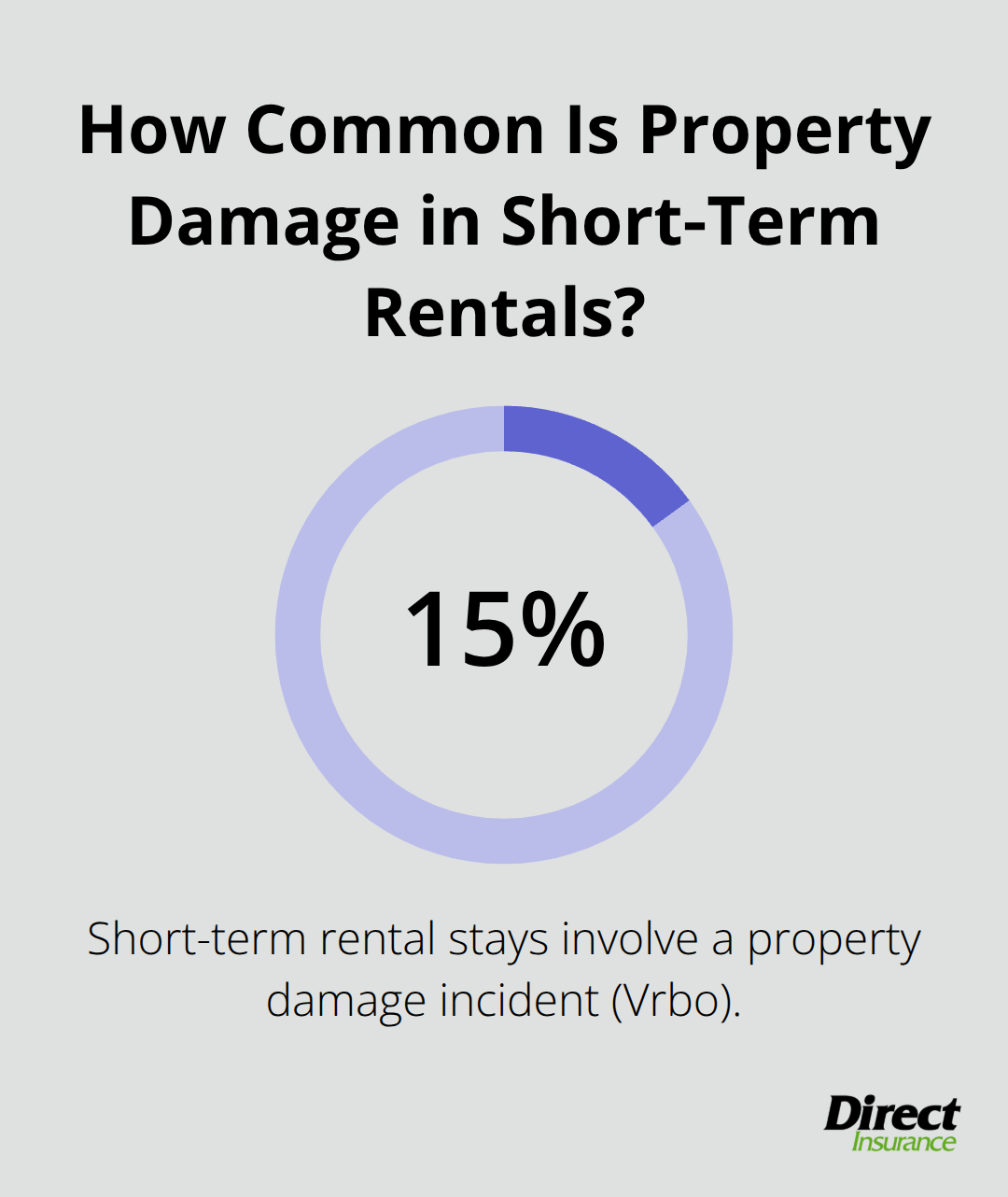

Airbnb hosts face property damage risks that extend far beyond typical rental scenarios. Guest parties result in thousands of dollars in damages, with broken furniture, damaged walls, and stained carpets as common outcomes. Vrbo data shows that property damage incidents occur in approximately 15% of short-term rental stays, which creates substantial financial exposure for unprepared hosts. Malicious damage from disgruntled guests represents another significant risk, as intentional destruction of electronics, fixtures, and personal items can devastate your property value.

Liability Exposure Creates Major Financial Threats

Guest injuries on your property create immediate liability concerns that can devastate your finances. Slip and fall accidents, burns from faulty appliances, or injuries from defective stairs result in lawsuits that exceed $100,000. Pool accidents result in significant injury incidents annually according to the Consumer Product Safety Commission, which makes liability protection essential for hosts with water features. Third-party property damage claims occur when guests damage adjacent properties, and this creates additional liability exposure that most hosts never consider.

Standard Homeowners Insurance Fails Short-Term Rental Hosts

Traditional homeowners insurance specifically excludes business activities, which leaves Airbnb hosts completely unprotected during guest stays. Insurance companies classify short-term rentals as commercial operations and void coverage for any incident that occurs during a paid stay. The number of short-term rentals in the U.S. has grown from 200,000 to over 2,000,000 in the past decade, yet most hosts remain dangerously underinsured. Coverage gaps include theft by guests, vandalism, lost rental income, and business liability claims that can bankrupt unprepared property owners.

Commercial Activity Changes Everything

Your property transforms from a personal residence to a commercial operation the moment you accept payment from guests. This fundamental shift triggers exclusions in standard policies that most hosts don’t realize exist until they file a claim. Insurance carriers view short-term rentals as hospitality businesses (similar to hotels), which requires specialized coverage to protect against unique risks.

Airbnb recognizes these coverage gaps and provides its own protection programs to help hosts bridge the insurance divide.

What Does Airbnb’s Host Protection Actually Cover

Airbnb’s AirCover for Hosts provides $1 million in liability insurance and $3 million in Host Damage Protection at no cost to hosts. The liability coverage protects you when guests suffer injuries on your property, while damage protection reimburses property repairs when guests cause destruction. However, Airbnb’s coverage operates as secondary insurance, which means your personal insurance must respond first before AirCover activates. This creates complications during claims because most homeowners policies exclude short-term rental activities entirely.

Claims Require Immediate Action

You must report incidents within 24 hours through Airbnb’s specialized intake form to maintain coverage eligibility. Late reports can void your claim entirely and leave you responsible for thousands in damages. Third-party adjusters handle all claims processing (not Airbnb staff), which often extends resolution timelines beyond 60 days. Documentation requirements include photos, police reports, medical records, and repair estimates, which makes thorough record-keeping essential for successful claims.

Coverage Gaps Leave Hosts Exposed

AirCover excludes intentional damage, normal wear and tear, and incidents outside active reservations. The program doesn’t cover lost rental income, business interruption, or damages that exceed policy limits. Hosts with six or more active listings face additional coordination requirements with existing insurance policies starting March 2025, which potentially reduces coverage effectiveness.

Theft by guests, vandalism during vacant periods, and liability claims from adjacent properties remain completely unprotected under Airbnb’s program.

Secondary Coverage Creates Problems

Airbnb’s insurance only pays after your primary insurance denies the claim or pays its portion first. Most homeowners policies exclude business activities entirely, which creates a coverage gap where neither policy responds. This secondary structure often leaves hosts without any protection during the claims process, as traditional insurers reject short-term rental claims immediately.

These limitations highlight why many professional hosts seek additional insurance options beyond Airbnb’s basic protection programs.

What Insurance Options Fill the Gaps

Specialized Short-Term Rental Insurance Provides Complete Protection

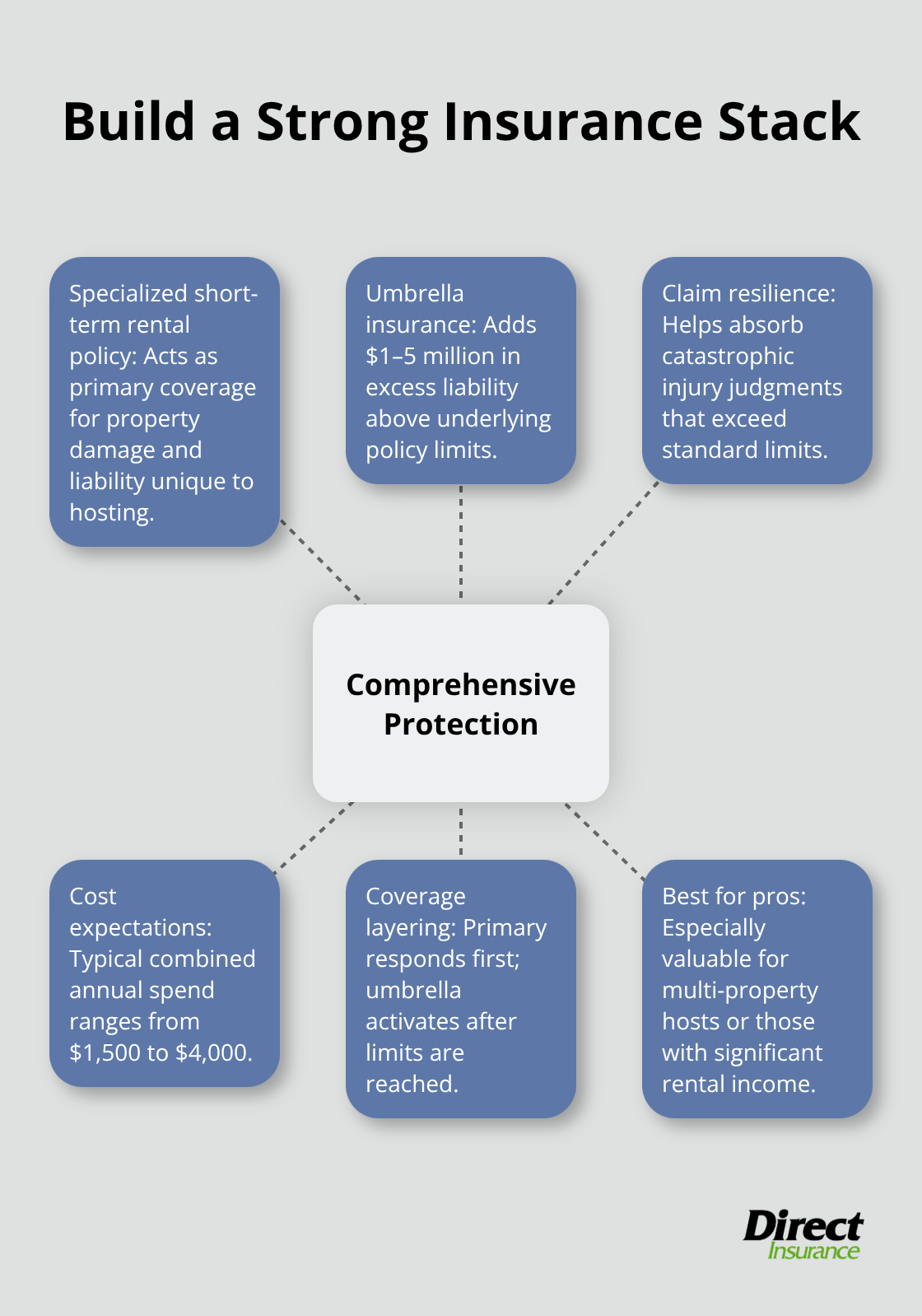

Proper Insurance offers comprehensive short-term rental policies that cover property damage, liability claims, and business interruption risks that Airbnb’s AirCover excludes entirely. Their policies provide replacement cost coverage with no damage limits from renters, plus first-to-market bed bug protection that covers extermination costs, guest liability up to $1 million, and up to 7 days of lost rental income for infestations. Liquor liability coverage protects hosts when guests consume alcohol and cause injuries, while commercial general liability starts at $1 million per incident. These specialized policies cost between $1,200-$3,000 annually but cover risks worth hundreds of thousands in potential claims.

Umbrella Insurance Multiplies Your Protection

Umbrella policies add $1-5 million in additional liability coverage above your existing insurance limits for just $200-400 per year. This extra protection activates when your underlying policies reach their limits, which provides essential coverage for serious injury claims that exceed standard policy limits. However, umbrella insurance only works when your underlying policies respond to claims first. Since most homeowners policies exclude short-term rental activities, umbrella coverage becomes ineffective without proper underlying short-term rental insurance.

Business Insurance Protects Professional Operations

Hosts who manage multiple properties or generate over $50,000 in annual rental income need commercial business insurance beyond standard short-term rental policies. General liability insurance protects against third-party injury claims, while commercial property insurance covers multiple properties and higher property values. Workers compensation becomes mandatory when hosts employ cleaners, maintenance staff, or property managers as regular employees rather than independent contractors.

Smart Hosts Combine Multiple Coverage Types

Professional hosts stack specialized short-term rental policies with umbrella insurance to create comprehensive protection against catastrophic liability claims. This combination approach (specialized primary coverage plus umbrella excess limits) provides the most robust protection available in today’s market. The total annual cost typically ranges from $1,500-$4,000 but protects against claims that could destroy your financial future and force property sales to cover judgments.

Final Thoughts

Utah Airbnb hosts face significant insurance gaps that standard homeowners policies don’t address. Property damage from guests, liability claims from injuries, and business interruption losses create financial risks that can destroy your investment property value overnight. Airbnb insurance coverage for hosts through AirCover provides basic protection, but secondary coverage structure and major exclusions leave dangerous gaps.

Professional hosts need specialized short-term rental insurance that covers theft, vandalism, lost income, and liability claims as primary coverage rather than secondary protection. Smart hosts combine specialized rental policies with umbrella insurance to create comprehensive protection against catastrophic claims. This approach costs $1,500-$4,000 annually but protects against lawsuits that exceed $100,000 (which could force property sales).

We at Direct Insurance Services help Utah hosts shop multiple top-rated insurance companies to find the best coverage at competitive rates. Our local team understands Utah’s unique risks and provides personalized service with flexible payment options to fit any budget. Contact Direct Insurance Services when your rental income exceeds $25,000 annually, you manage multiple properties, or standard policies deny claims.