VRBO Insurance for Owners What You Need to Know

VRBO insurance for owners presents unique challenges that standard homeowner’s policies simply don’t address. Short-term rental properties face different risks than traditional homes.

We at Direct Insurance Services see property owners struggle with coverage gaps that could cost thousands in unprotected losses. The right insurance strategy protects both your investment and your rental income.

What Insurance Gaps Are Costing VRBO Owners

Standard homeowner’s insurance policies exclude short-term rental activities entirely. Insurance companies classify vacation rentals as commercial enterprises, which leaves property owners with zero coverage during guest stays. VRBO owners face claim denials worth $15,000 to $50,000 because their traditional policy considers the rental activity a business operation.

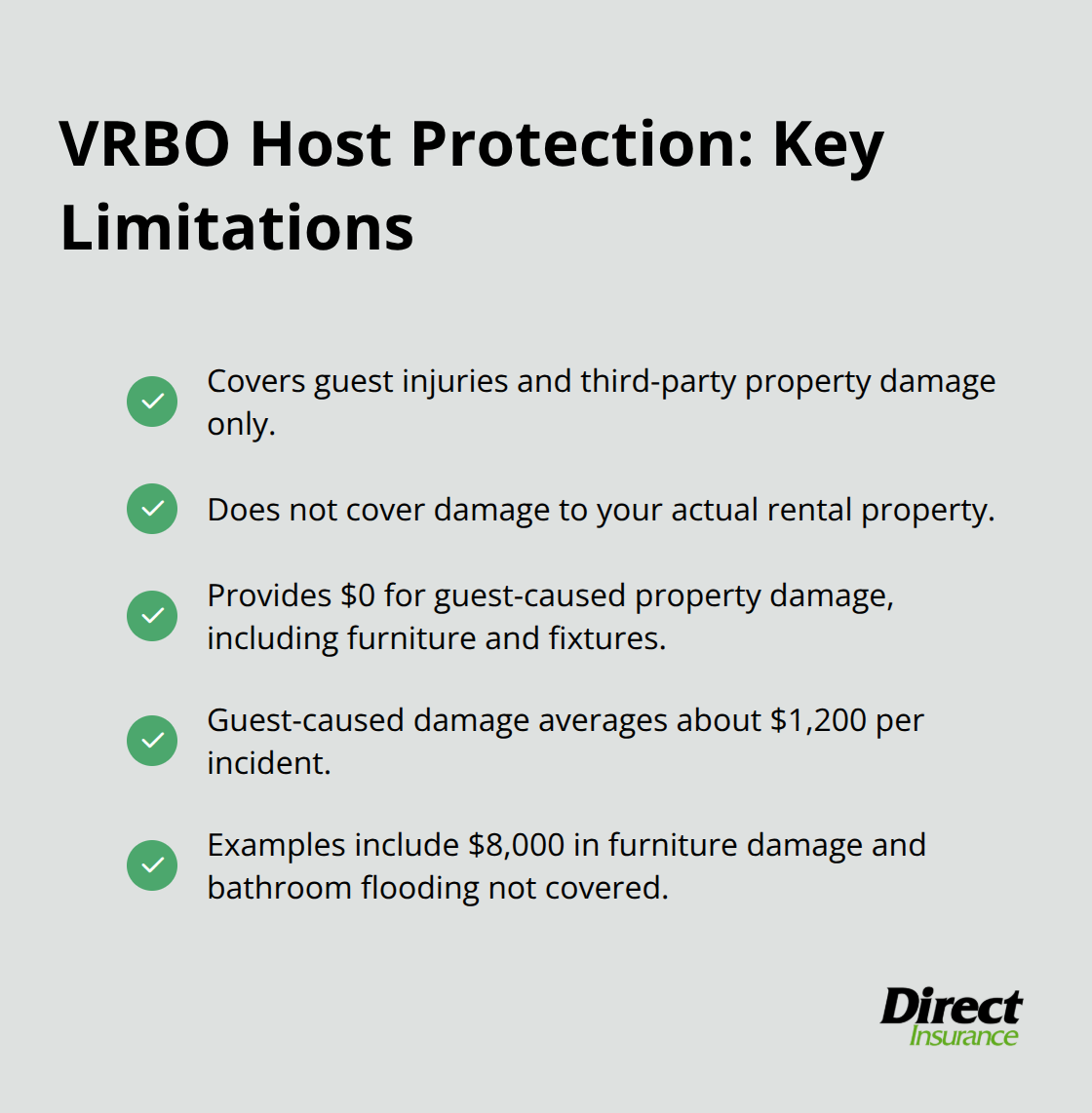

VRBO Host Protection Provides Limited Coverage

VRBO provides liability coverage through Generali Global Assistance, but this protection has major limitations. The coverage only applies to guest injuries and third-party property damage – not damage to your actual rental property. When guests cause $8,000 in furniture damage or flood your bathroom, VRBO Host Protection pays nothing.

Property owners need separate policies that cover guest-caused damage, which can average $1,200 per incident according to vacation rental damage reports.

State Requirements Create Additional Pressure

Cities like San Francisco require $500,000 minimum liability coverage for short-term rentals, while Austin mandates $1 million. These municipal requirements often exceed what VRBO provides, which forces owners to purchase commercial policies or face permit violations. Colorado recently passed legislation that requires vacation rental insurance disclosure to guests (adding compliance complexity). Property owners who operate without proper coverage risk losing their rental permits and face municipal fines that range from $500 to $2,000 per violation.

Commercial Policies Bridge the Gap

Commercial vacation rental policies typically cost $1,500 to $3,000 annually but provide comprehensive protection that standard homeowner’s insurance and VRBO Host Protection cannot match. These specialized policies cover property damage, liability, and business interruption – three areas where traditional coverage fails. This coverage costs $200-500 annually but prevents gaps when personal policies exclude business activities. The next step involves understanding exactly what types of coverage your VRBO property needs to operate safely and profitably.

Essential Coverage Types for VRBO Property Owners

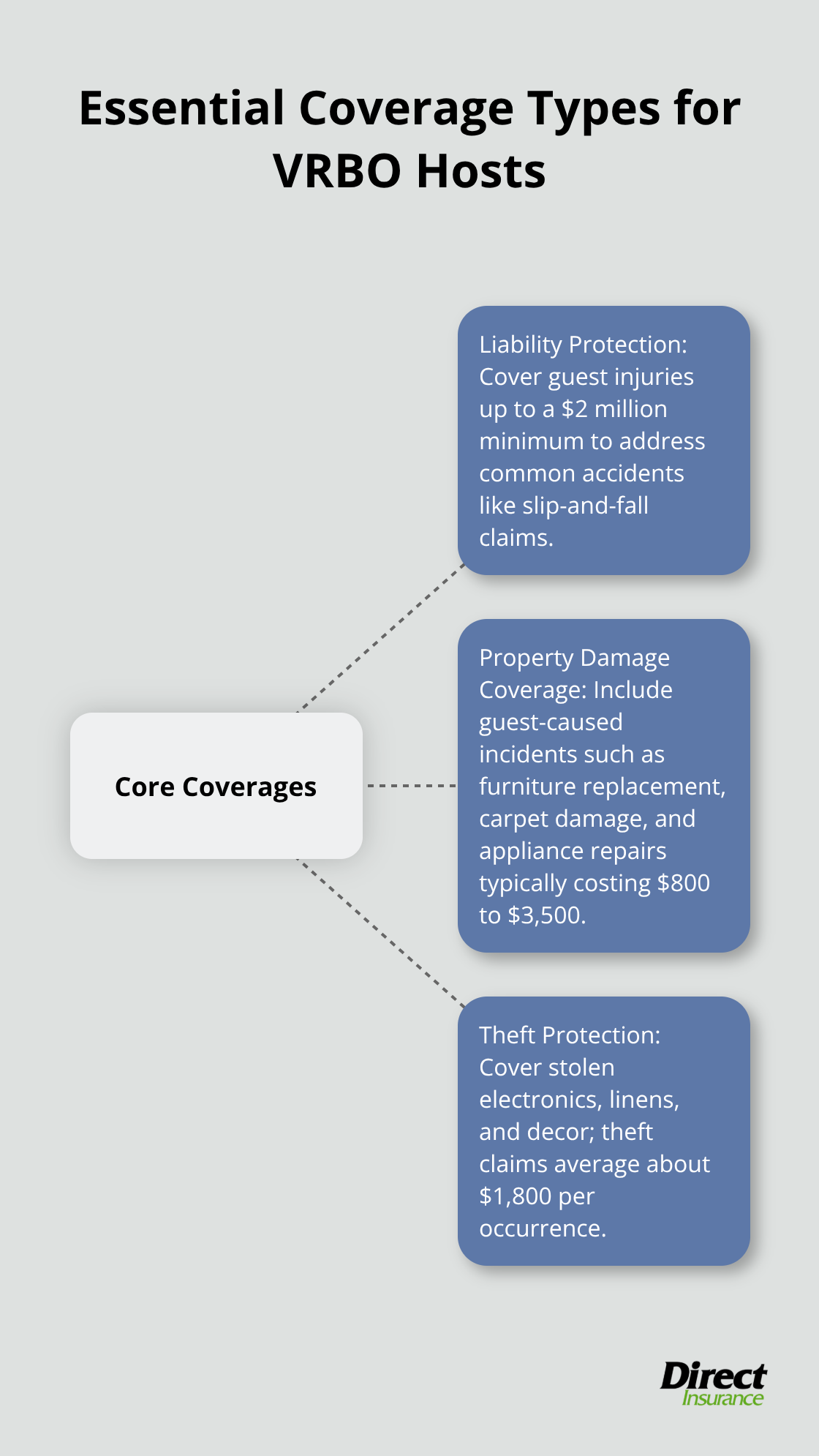

VRBO property owners require three specific coverage types that traditional homeowner’s policies exclude completely. Liability protection must cover guest injuries up to $2 million minimum, as slip-and-fall claims are among the most common accidents in the US according to safety data. Property damage coverage should include guest-caused incidents, with policies that cover furniture replacement, carpet damage, and appliance repairs that typically cost $800 to $3,500 per incident. Theft protection becomes vital when guests steal electronics, linens, or decorative items – vacation rental theft claims average $1,800 per occurrence based on insurance industry data.

Liability Protection Against Guest Injuries

Guest injury lawsuits can destroy VRBO businesses overnight without proper liability coverage. Pool drowning incidents result in settlements that exceed $500,000, while balcony falls generate claims between $75,000 and $200,000. Hot tub injuries produce average settlements of $85,000, which makes liability coverage the most important protection for vacation rental owners. Standard VRBO Host Protection caps at $1 million, but serious injury claims often exceed this limit (particularly in states with high medical costs).

Property Protection Against Guest Damage

Guest-caused property damage extends beyond normal wear and tear to include intentional destruction, floods from clogged toilets, and kitchen fires from unattended cooking. Vacation rental policies cover these incidents while homeowner’s insurance excludes them entirely. Water damage from guest negligence averages $4,200 per claim, while fire damage can reach $15,000 to $30,000 for kitchen incidents. Specialized policies protect against these risks that standard coverage ignores.

Business Interruption Coverage for Lost Income

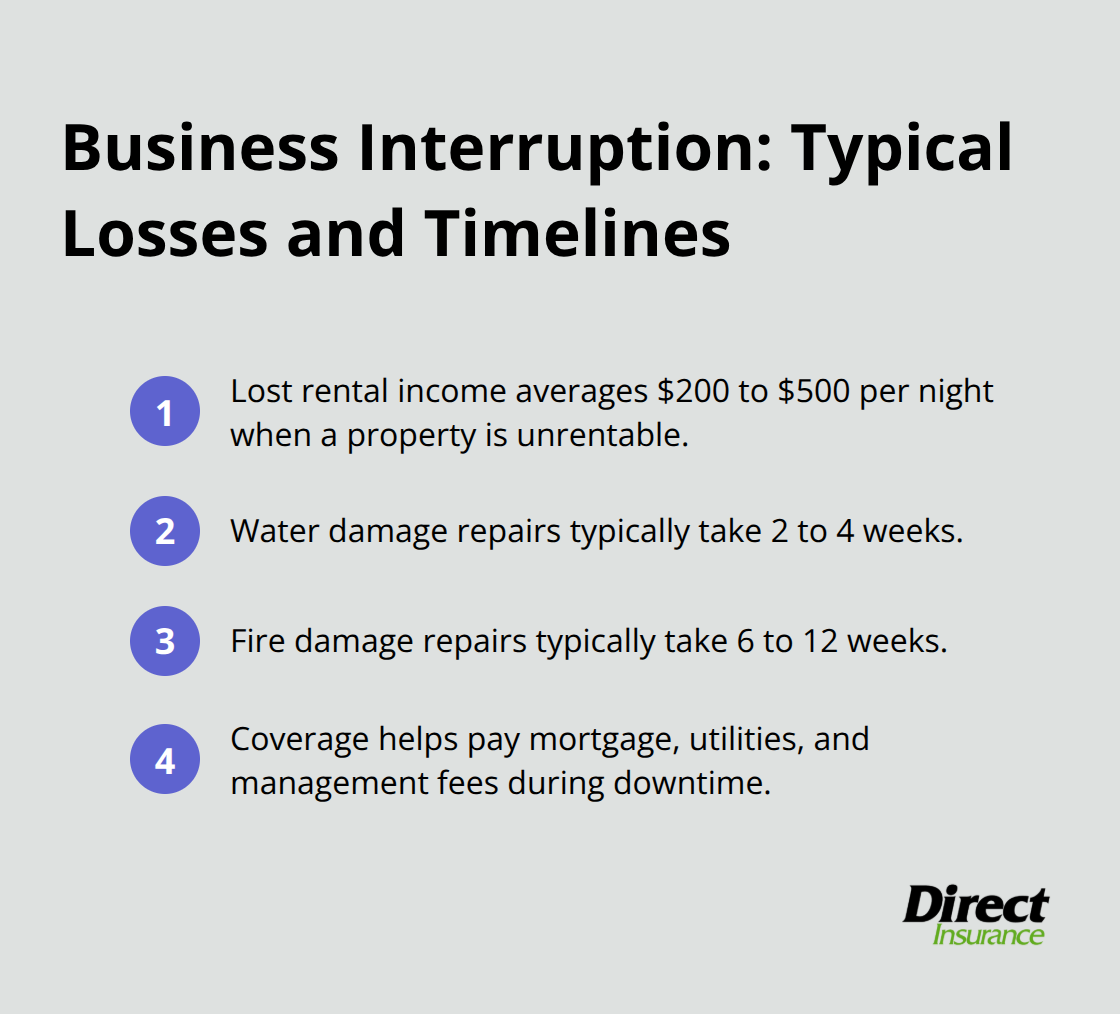

VRBO owners lose $200 to $500 per night when properties become uninhabitable after damage incidents. Business interruption insurance replaces this lost rental income during repair periods, which average 2-4 weeks for water damage and 6-12 weeks for fire damage.

This coverage pays ongoing expenses like mortgage payments, utilities, and property management fees while the property remains unrentable (protecting cash flow during repairs).

Even comprehensive coverage leaves dangerous gaps that traditional policies create through specific exclusions and limitations.

Common Insurance Gaps and How to Address Them

Traditional homeowner and landlord insurance policies contain specific exclusions that eliminate coverage for short-term rental activities entirely. Most policies include commercial use exclusions that void coverage when properties generate rental income for periods shorter than 30 days. Homeowner policies exclude business activities, while landlord policies only cover long-term tenant situations – neither addresses the unique risks of VRBO operations. State Farm and Allstate policies explicitly state that coverage terminates when properties are rented for commercial purposes (which includes vacation rentals). These exclusions mean that property damage, liability claims, and theft incidents during guest stays receive zero coverage from traditional policies.

Commercial Vacation Rental Policies Fill Coverage Voids

Commercial vacation rental policies from carriers like Proper Insurance and Safely provide comprehensive protection that traditional policies exclude completely. These specialized policies offer property managers essential coverage for vacation rental operations, addressing the unique risks and requirements of short-term rental businesses. Commercial policies include coverage for property damage, guest liability, and business interruption without commercial use exclusions. These policies also provide protection for periods when properties remain vacant between bookings, eliminating the coverage gaps that occur with traditional homeowner insurance during unoccupied periods.

Independent Agents Navigate Complex Coverage Requirements

Independent agents who specialize in vacation rental insurance prevent costly coverage mistakes that property owners make when they purchase policies directly from carriers. Independent agents access multiple commercial carriers simultaneously and can compare coverage terms, exclusions, and rates across different insurance companies. These agents evaluate each property’s specific risk profile, rental frequency, and local insurance requirements to recommend optimal coverage combinations that traditional agents cannot provide. Independent agents also handle claims advocacy when disputes arise, which can improve claim outcomes compared to property owners who file claims without professional assistance. Utah hosts face significant insurance gaps that require specialized coverage solutions beyond standard homeowner policies.

Final Thoughts

VRBO insurance for owners demands a strategic approach that moves beyond basic homeowner coverage. Property owners who rely on traditional policies face claim denials that average $25,000 per incident, while those with specialized vacation rental insurance receive full protection for guest-caused damage, liability claims, and business interruption losses. The most successful VRBO owners purchase commercial vacation rental policies that cost $1,500 to $3,000 annually but prevent devastating financial losses.

These policies cover property damage during guest stays, liability protection up to $2 million, and lost rental income during repair periods. Property owners must verify that their coverage meets local requirements, as cities like Austin mandate $1 million minimum liability coverage for short-term rentals. Regular policy reviews become essential as rental operations expand or local regulations change (particularly when adding new properties to portfolios).

Property owners should evaluate their coverage annually and after major operational changes. We at Direct Insurance Services help Utah property owners navigate these complex insurance requirements by shopping multiple carriers to find comprehensive vacation rental coverage at competitive rates. Our team provides personalized solutions that protect both properties and rental income streams.