Utah Homeowners Insurance Basics: A Quick Overview

Homeowners insurance in Utah protects your biggest investment from unexpected financial losses. Whether you’re dealing with weather damage, theft, or liability claims, the right policy makes all the difference.

At Direct Insurance Services, we help Utah homeowners understand their coverage options and find policies that fit their needs and budgets. This guide walks you through the essentials so you can make informed decisions about your protection.

What Your Utah Homeowners Policy Actually Covers

A standard Utah homeowners policy protects three main areas of your financial life. Dwelling coverage shields your home’s physical structure from fire, windstorms, hail, lightning, theft, and vandalism. Wind and hail accounted for the largest share of claims, with 2.8 percent of insured homes having such a loss, making this protection genuinely important.

Personal Property and Belongings

Personal property coverage reimburses you for belongings inside your home-furniture, electronics, clothing, appliances-even if someone steals them outside your house. The critical difference lies between replacement cost and actual cash value. Replacement cost pays what it costs to replace your item today; actual cash value deducts depreciation. If your five-year-old television burns in a fire, replacement cost might pay $600 while actual cash value pays $250. We strongly recommend replacement cost coverage whenever your budget allows it because the alternative leaves you significantly underprotected.

Liability Protection and Additional Living Expenses

Liability protection covers legal fees and medical expenses if someone is injured on your property and sues you. A visitor slips on your icy walkway in January-your liability coverage pays their medical bills and legal costs up to your policy limit, typically $100,000. Additional living expenses, sometimes called loss of use coverage, pays for hotel stays or rental housing if a disaster forces you to temporarily leave your home. National data from the Insurance Information Institute shows roughly one in 18 insured homes files a claim annually, so this protection matters more than many homeowners realize.

What Utah Policies Exclude

Standard homeowners insurance does not cover flood damage or earthquakes. Utah faces real earthquake risk in certain areas, and St. George and Ogden residents particularly benefit from adding earthquake endorsements to their policies. Flood coverage requires a separate policy entirely. Termite infestations, pest damage, and routine wear and tear also fall outside coverage.

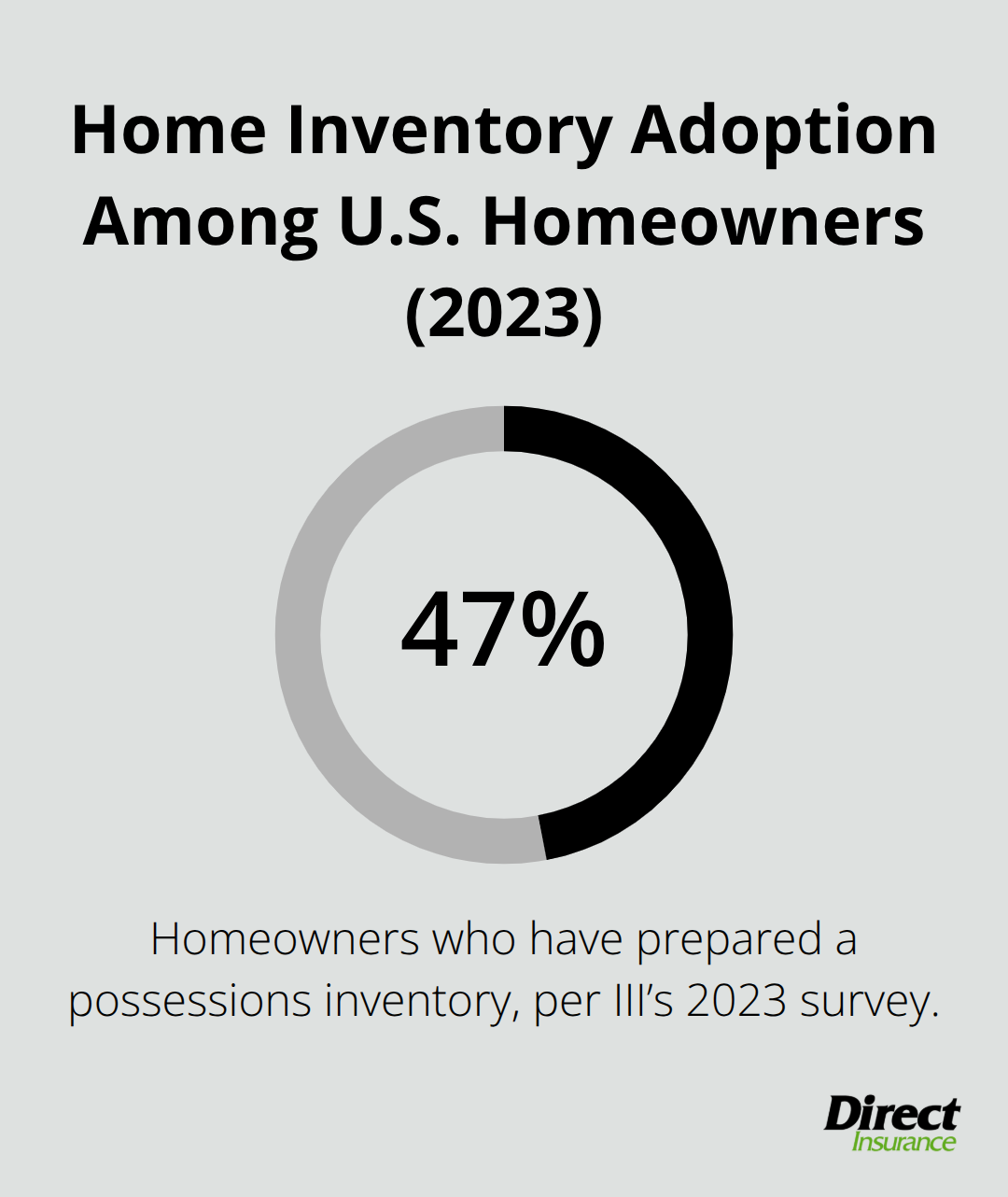

Protect Your Belongings with a Home Inventory

Many Utah homeowners underestimate how much they need to protect their belongings. A home inventory-photographing or listing your possessions with approximate values-dramatically simplifies claims when losses occur.

The Insurance Information Institute’s 2023 consumer survey found that 47% of homeowners had prepared a possessions inventory, yet most still underestimate their total personal property value. Solar panels, outdoor structures like sheds, and basement finishing may or may not be covered depending on your insurer, so you must verify these details before assuming protection exists. Understanding what your policy covers sets the foundation for choosing the right coverage limits-a decision that depends directly on your home’s replacement value and your personal belongings.

Factors That Affect Your Utah Home Insurance Rates

Your Utah homeowners insurance rate reflects factors you control and factors you cannot. Location matters most. ZIP code determines your rate more than almost anything else because it reflects local risk exposure. According to Insure.com data analyzing quotes from 82 national and regional insurers across Utah, the ZIP code 84015 averages around $1,498 annually while 84080 runs approximately $2,133 for the same coverage level. That $635 difference stems purely from where your home sits.

How Location and Local Risk Shape Your Premium

Areas with higher wildfire exposure, greater theft rates, or more frequent hail and wind damage cost substantially more to insure. St. George and Ogden residents face elevated earthquake risk, which directly impacts your base premium before you even consider optional earthquake coverage. Your home’s physical characteristics also influence pricing significantly. Newer homes with updated electrical systems, plumbing, and roofing cost less to insure than homes built in the 1970s with original materials. Brick and concrete block construction typically costs less than wood frame construction because these materials resist fire and weather damage more effectively.

Claims History and Credit Score Impact

Your claims history and credit score round out the major pricing factors. Insurers view your claims history as a predictor of future losses, so filing multiple claims in five years raises your rate substantially. Your credit score reflects financial responsibility in the lender’s view, and homeowners with lower credit scores pay more across nearly all carriers.

Understanding Your Specific Rate Drivers

Understanding your specific rate drivers matters more than memorizing national averages. Some people can reduce rates by improving their credit score before shopping. Others live in high-risk ZIP codes where location is unchangeable, so they should focus on maximizing discounts instead. Bundling your homeowners and auto insurance typically saves 10 to 25 percent on both policies. Smart home discounts for security systems and water leak detection devices also reduce premiums.

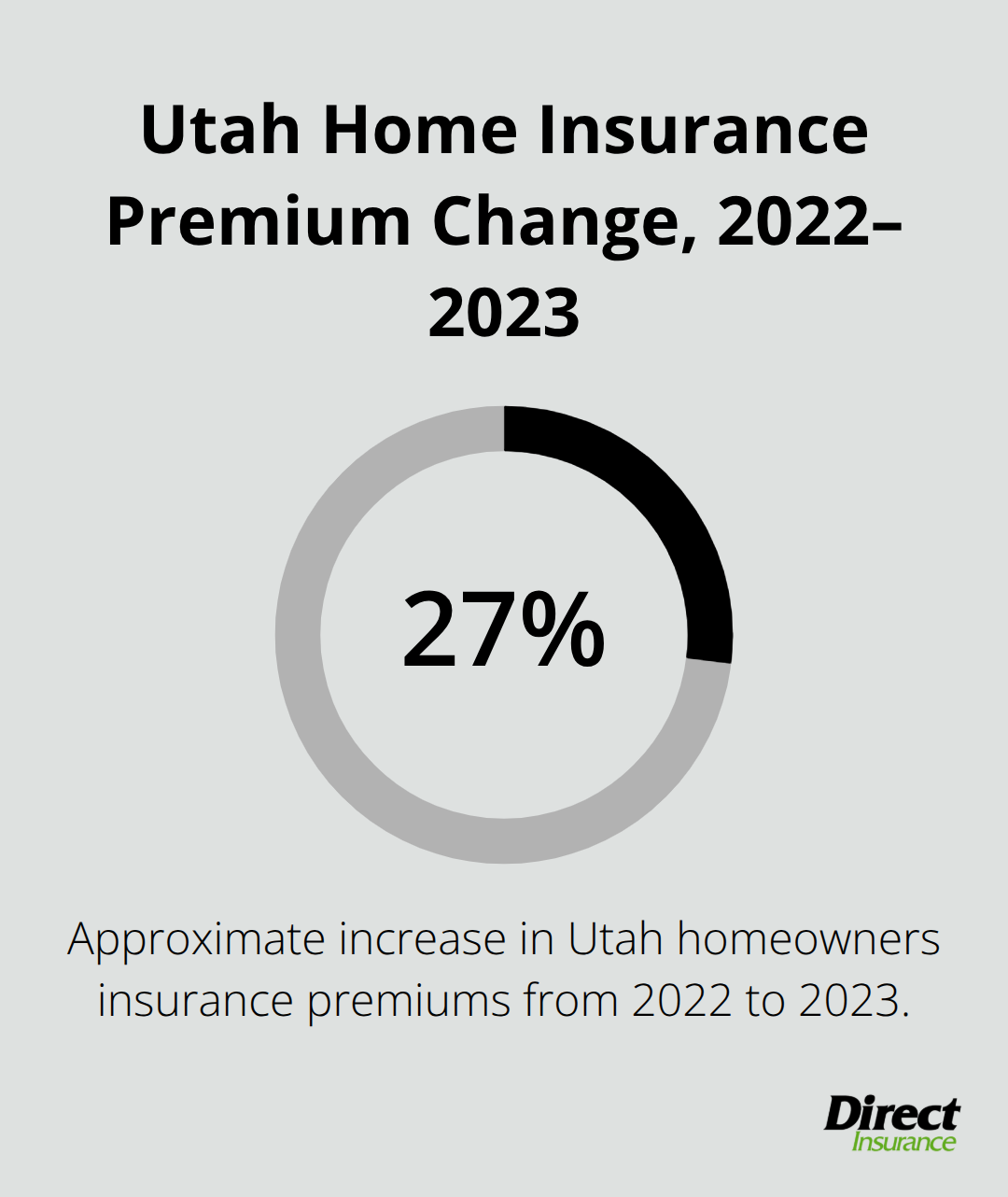

What Utah Homeowners Actually Pay

Utah’s average homeowners insurance cost sits at $1,541 annually or about $128 per month according to the National Association of Realtors. Premiums rose approximately 27 percent from 2022 to 2023, reflecting nationwide pressure on the insurance market. Comparing quotes from at least three different insurers remains essential because the same home in the same ZIP code receives vastly different quotes from different carriers. State Farm averages around $1,078 annually in Utah while American Family averages $1,249 and Nationwide $1,254 for identical coverage, demonstrating how carrier selection alone can save you hundreds of dollars yearly. Shopping multiple insurers takes two hours maximum and could cut your annual cost by 30 percent or more.

The rates you receive depend heavily on which carrier you approach and how thoroughly you compare options. Once you understand what drives your costs, the next step involves selecting a policy that actually protects your home and belongings at a price that fits your budget.

How to Choose the Right Homeowners Insurance Policy

Start with your home’s replacement value, not its current market price. The market value of your Utah home and what it costs to rebuild from scratch are completely different numbers. A home worth $400,000 might cost $550,000 to rebuild because construction materials and labor have increased dramatically. Insure.com data shows that premiums rise predictably with dwelling coverage limits: a $200,000 dwelling limit costs roughly $1,407 to $1,416 annually, while $300,000 costs about $1,792, $400,000 runs $2,149 to $2,161, and $600,000 reaches approximately $2,862 to $2,876 for the same profile and ZIP code. Get a professional rebuild estimate from a local contractor or use the National Association of Home Builders cost calculator to establish your actual replacement cost. Underinsuring by $100,000 might save you $300 annually but leaves you exposed to catastrophic financial loss if your home burns. Overinsuring wastes money on coverage you’ll never use.

Your personal property coverage limit should reflect what you actually own. Most people own far more than they estimate until they photograph their belongings room by room and price them. Electronics, furniture, clothing, jewelry, and tools add up quickly. If you own expensive items like art, jewelry, or collectibles, you need scheduled personal property endorsements because standard policies cap coverage on high-value items.

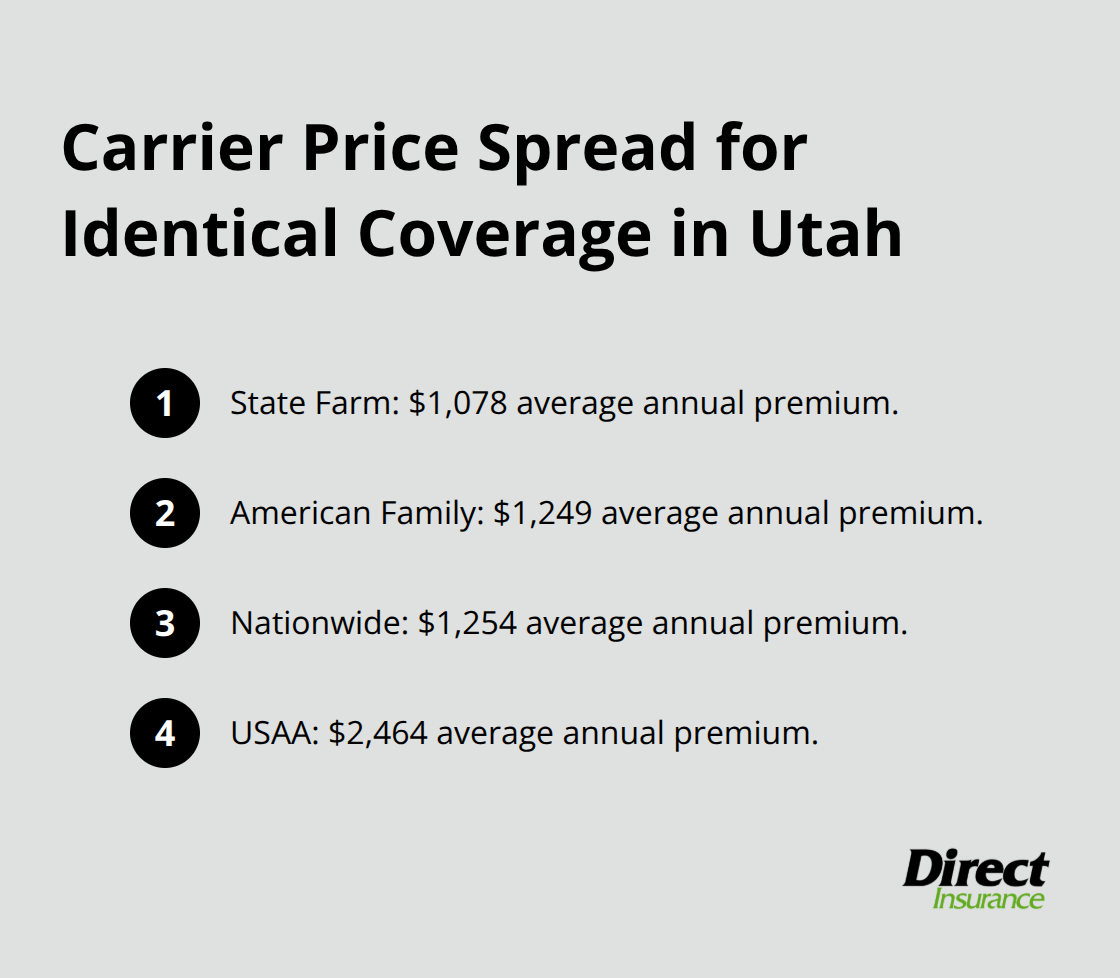

Compare Quotes from Multiple Carriers

Pull quotes from at least three different insurers before making any decision. The same home receiving quotes from State Farm, American Family, and Nationwide can show price differences exceeding $400 annually for identical coverage. Insure.com analyzed quotes from 82 national and regional insurers across 34,588 Utah ZIP codes and found State Farm averaging $1,078 annually while USAA ran $2,464 for the same profile, though USAA only serves military members and their families.

When comparing quotes, ensure every quote uses identical dwelling limits, deductibles, and endorsements. A quote missing earthquake coverage looks cheaper until you discover the competitor’s quote includes it. Request detailed breakdowns showing what each endorsement costs separately. Earthquake coverage in Utah can double your premium depending on your location and carrier, so understanding the specific cost matters.

Optimize Your Deductible and Discounts

Your deductible choice directly impacts your premium. Raising your deductible from $1,000 to $2,500 typically reduces your annual cost by 15 to 25 percent. This strategy works only if you have cash reserves to cover the higher deductible after a loss. If a $2,500 deductible would strain your finances, stick with $1,000.

Bundling your homeowners and auto policies typically saves 10 to 25 percent on both policies according to industry standard discounts. Smart home discounts for security systems and water leak detection devices also reduce premiums, sometimes by 5 to 10 percent depending on your carrier.

Leverage Utah’s Regional Pricing Variations

Utah’s ZIP code pricing varies dramatically enough that location-based shopping matters significantly. The difference between 84015 at approximately $1,498 annually and 84080 at roughly $2,133 represents a $635 gap for standard coverage according to Insure.com data. Some carriers price aggressively in specific regions while others avoid them entirely.

An independent insurance agency can access multiple carriers simultaneously and identify which ones offer competitive rates in your specific ZIP code without you submitting separate applications to each company. This saves hours of phone calls and repeated data entry. Ask your agent specifically about Utah-based carriers like Bear River Mutual and Quality 1st, which sometimes offer rates competitive with national carriers. Local carriers understand Utah’s specific risks from wildfire, hail, and snow load better than national companies.

Verify Coverage Details Before Signing

Once you’ve compared quotes and selected your coverage limits, review the policy document before signing. Verify that solar panels are covered if you have them, confirm whether your shed or garage has adequate coverage, and check if your basement finishing is included. These details vary by insurer and can mean the difference between a claim paid in full and a claim denied.

Final Thoughts

Utah homeowners insurance basics require three concrete actions: understanding what your policy covers, knowing what drives your rates, and comparing options before you buy. Dwelling coverage protects your home’s structure, personal property coverage reimburses your belongings, and liability protection shields you from lawsuits when someone gets injured on your property. Location, home age, claims history, and credit score determine your premium, and the same coverage costs vastly different amounts depending on which carrier you choose.

Start by gathering your home’s replacement cost estimate and listing your major belongings with approximate values. Request quotes from at least three different insurers using identical coverage limits and deductibles, then compare them line by line while paying special attention to what each endorsement costs separately. Identify which discounts apply to your situation-whether that means bundling auto and home insurance or installing a security system.

We at Direct Insurance Services help Utah homeowners navigate these decisions with quotes from multiple top-rated insurance companies. Our team understands Utah’s specific risks from wildfires, hail, earthquakes, and snow load, and we explain policy details in plain language to help you avoid coverage gaps. Contact Direct Insurance Services to get started with quotes today.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation