Personal Umbrella Utah Tips: Strengthen Your Safety Net With Extra Coverage

One lawsuit can wipe out years of financial progress. At Direct Insurance Services, we’ve seen Utah families lose homes and savings because their standard homeowners or auto insurance wasn’t enough.

Personal umbrella Utah tips start with understanding that your existing policies have limits-often $300,000 or less. When someone sues you for more than that, you’re personally responsible for the difference.

That’s where umbrella coverage steps in, protecting your assets with an extra layer of liability insurance that kicks in when your other policies max out.

What Umbrella Coverage Actually Protects in Utah

A personal umbrella policy is straightforward liability insurance that activates after your homeowners or auto policy limits are exhausted. In Utah, standard homeowners policies typically cap liability at $300,000, while auto policies often max out around $500,000. Once a claim exceeds these limits, you become personally liable for the remainder. An umbrella policy bridges that gap by adding $1 million to $5 million in extra coverage, with most Utah residents starting at $1 million. The policy pays legal defense costs, medical expenses, and settlements that your underlying policies won’t cover. Unlike your primary policies, umbrella coverage costs remarkably little-typically $175 to $300 annually for $1 million of protection in Utah, with each additional million costing roughly $75 per year according to ACE Private Risk Services data.

How the Coverage Actually Works When You Need It

The mechanics are simple but powerful. Your homeowners and auto policies pay first up to their stated limits. Once exhausted, your umbrella policy activates. Consider a concrete example: a serious dog bite at your home results in $650,000 in medical bills and legal fees.

Your homeowners liability limit of $500,000 covers the initial claim, but you remain personally responsible for the remaining $150,000 without umbrella protection. With an umbrella policy in place, that extra layer absorbs the $150,000 difference, protecting your savings and assets. The Insurance Information Institute reports that only 0.77% of people with liability insurance filed bodily injury claims in 2023, but those claims that do occur frequently exceed standard policy limits, making umbrella coverage essential for serious financial protection.

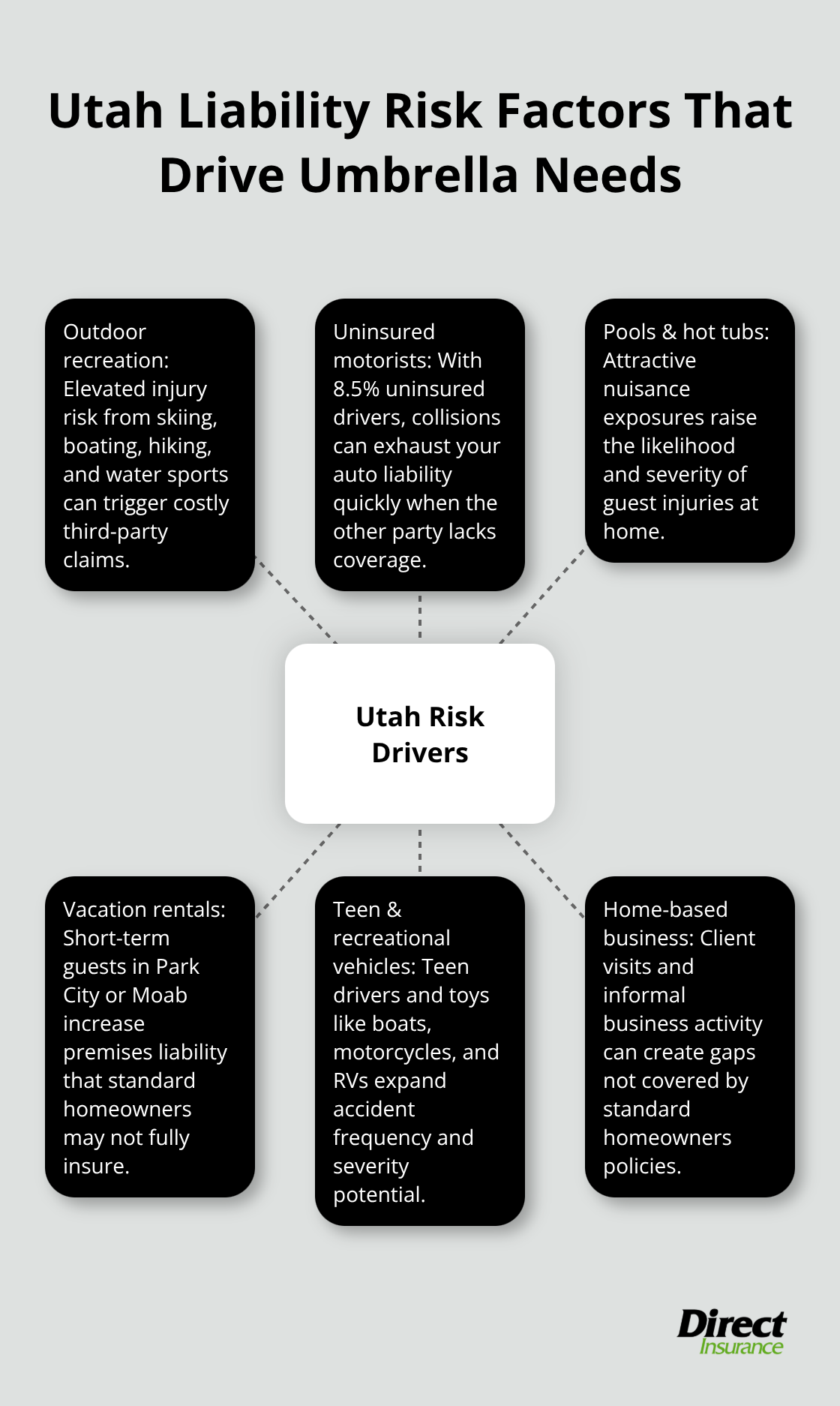

Utah’s Specific Risk Environment

Utah residents encounter liability exposures that make umbrella coverage particularly valuable. The state’s outdoor recreation culture-skiing, water sports, hiking, and boating-creates elevated injury risks on your property and through your activities. Utah’s uninsured driver rate sits around 8.5%, meaning collisions with uninsured motorists can quickly deplete your auto liability limits. Pool and hot tub ownership, common in Utah suburbs, dramatically increases attractive nuisance liability exposure.

Vacation rental owners in Park City, Moab, and similar areas face heightened guest-injury risk that standard homeowners policies don’t adequately cover. Additionally, nearly 40% of Americans lack sufficient liability coverage to protect their assets, according to the Insurance Information Institute, and Utah residents are no exception.

Business Activities and Home-Based Work

If you operate a home-based business or meet clients at your residence, standard homeowners coverage often excludes business-related liability claims entirely. This gap leaves you exposed to significant financial risk. An umbrella policy fills this protection hole by covering liability that your primary homeowners policy rejects. These factors combine to create a liability environment where umbrella protection becomes a practical necessity for preserving the financial security you’ve built. Understanding how much coverage you actually need requires a closer look at your specific assets and lifestyle-a calculation that determines whether $1 million or $5 million in umbrella limits makes sense for your situation.

How Much Umbrella Coverage to Buy

Start with your net worth, not your income. Your umbrella limit should roughly match or exceed your total assets-savings, investments, real estate, retirement accounts, everything. If you own a $500,000 home, have $200,000 in retirement savings, and maintain $100,000 in liquid investments, you’re protecting $800,000 in assets. A $1 million umbrella policy makes sense here. If your net worth climbs to $2 million or higher, you should seriously consider $2 million to $3 million in umbrella coverage. This isn’t about being overly cautious; it’s about matching your protection to what you actually stand to lose. A lawsuit judgment doesn’t just take future income-courts can seize assets you’ve already built. According to ACE Private Risk Services data, the average cost for $1 million of umbrella coverage in Utah runs $175 to $300 annually, making it remarkably affordable relative to your actual exposure. Each additional $1 million typically costs around $75 per year, so jumping from $1 million to $2 million in coverage adds roughly $75 to your annual premium.

Calculate Your Actual Asset Protection Need

That minimal investment protects against the financial devastation a major lawsuit could inflict. Start by listing every asset you own: your home value, vehicles, savings accounts, investment portfolios, retirement funds, and any other property. Add these figures together to reach your total net worth. This number becomes your baseline for umbrella coverage decisions. A quiet lifestyle with minimal entertaining, no pool, and modest recreational activity might justify $1 million in coverage. Most Utah homeowners should start at $1 million minimum and move to $2 million if your net worth exceeds $1 million or your lifestyle includes multiple risk factors.

How Your Lifestyle Multiplies Your Liability Exposure

If you host frequent gatherings, own a swimming pool or hot tub, operate a home-based business, rent out a vacation property, or participate in water sports and skiing, your liability exposure multiplies dramatically. Pool ownership alone can add $50 to $150 annually to umbrella premiums because attractive nuisance liability is real and costly. Vacation rental owners in Park City or Moab face guest-injury exposure that standard homeowners policies explicitly exclude, making umbrella coverage essential rather than optional. Teen drivers on your auto policy increase accident risk substantially, which influences both your underlying auto limits and your umbrella needs. If you own recreational vehicles-boats, motorcycles, RVs-your liability footprint expands significantly. Utah’s uninsured motorist rate of 8.5% means your collision exposure is higher than national averages, creating a stronger case for robust umbrella limits. Home-based professionals who meet clients at their residence face business liability gaps that umbrella policies bridge, though you should confirm your specific business activities are covered under the policy terms.

Match Your Coverage to Worst-Case Scenarios

If you own rental property, frequently host events, maintain a pool, or operate any business activity from home, $2 million becomes the practical floor. Higher net worth individuals-those with $3 million or more in assets-benefit from $3 million to $5 million in umbrella coverage. The Insurance Information Institute found that nearly 40% of Americans lack sufficient liability coverage, and many Utah residents fall into this underinsured category. Your current auto and homeowners liability limits matter too; most carriers require minimum underlying coverage of $300,000 for homeowners and $250,000 to $500,000 for auto before issuing umbrella protection. If your existing limits are lower, raising them first makes financial sense, then layering umbrella coverage on top. Medical expenses for catastrophic injuries routinely exceed $500,000, and legal defense costs alone can reach $150,000 or more. Your umbrella limit should reflect the worst-case scenario specific to your situation, not a generic one-size-fits-all number. Once you’ve determined your coverage target, the next step involves understanding which carriers offer the best rates and terms for your particular risk profile-a comparison that requires shopping multiple insurers to find genuine value.

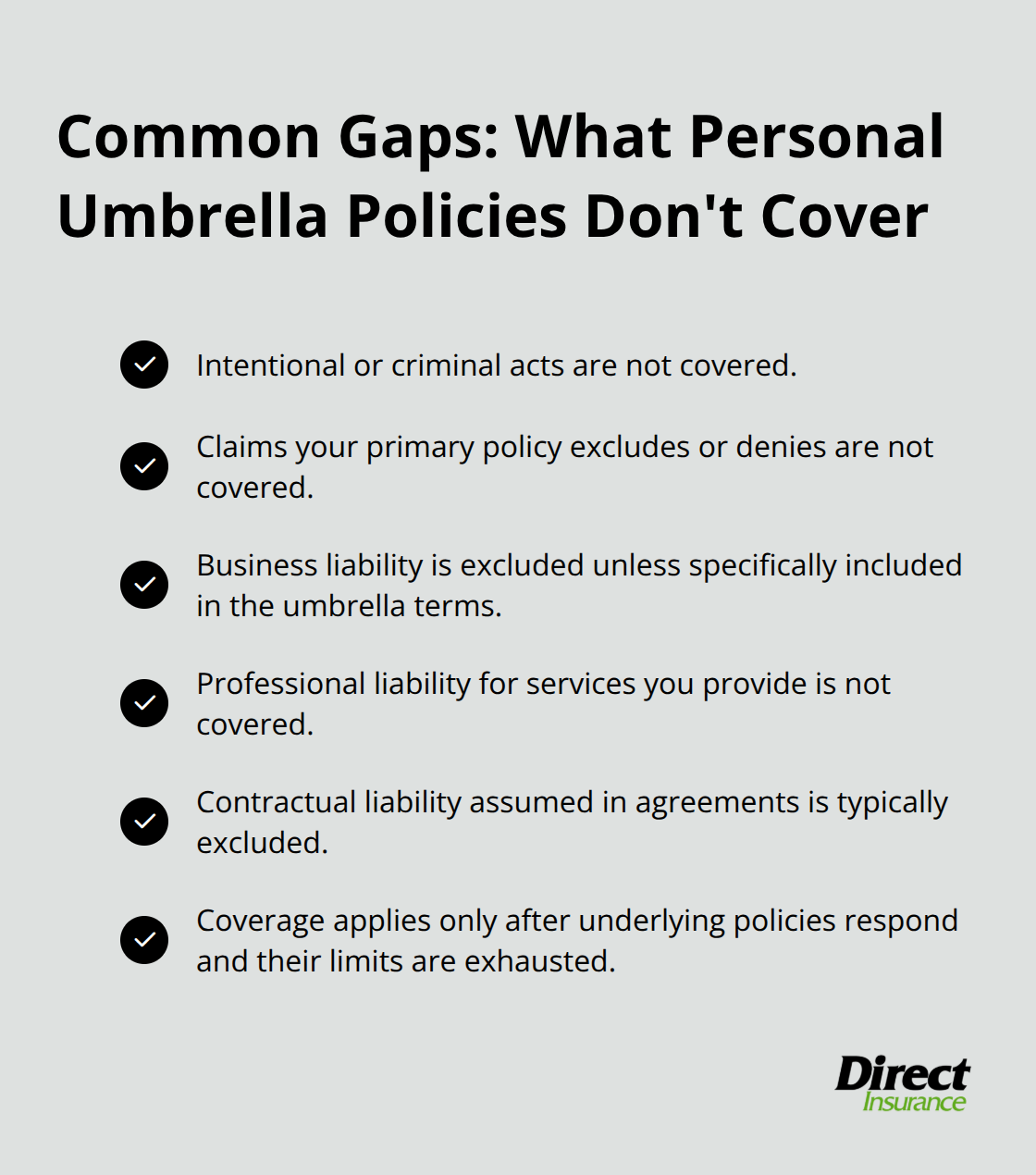

What Umbrella Insurance Actually Covers and Doesn’t

Coverage Boundaries That Matter

Most Utah residents believe umbrella policies function like a financial cure-all, covering any liability gap left by their primary insurance. This misconception costs people real money. Umbrella policies have specific boundaries, and understanding them prevents expensive surprises when you need protection most.

Your umbrella policy will not cover intentional acts, criminal behavior, or liability your underlying homeowners and auto policies explicitly exclude. If your homeowners policy denies a claim because you failed to maintain your property or violated policy conditions, your umbrella won’t rescue you. Business liability claims often fall outside umbrella coverage unless your policy specifically includes business pursuits, which most standard policies do not.

Professional liability-lawsuits from clients who hired you for services-remains unprotected under personal umbrella policies designed for household and recreational exposure. Contractual liability you assumed in a written agreement typically isn’t covered either. The umbrella activates only after your underlying policies exhaust their limits, meaning those primary policies must actually cover the incident first.

Why Your Primary Policies Matter First

If your homeowners policy denies a dog bite claim because you failed to disclose the animal, your umbrella won’t step in to save you. This is why reviewing your current homeowners and auto policy exclusions matters before purchasing umbrella coverage. You need to understand what your primary policies actually protect before adding a secondary layer on top.

The Real Cost of Umbrella Protection

Many Utah residents assume umbrella insurance costs thousands annually because they’ve never priced it, so they skip it entirely. Reality contradicts this assumption sharply. A $1 million umbrella policy in Utah costs between $175 and $300 per year for most homeowners, adding just $200-400 annually for $1-5 million in additional liability coverage above your existing insurance limits. Each additional million dollars of coverage adds roughly $75 annually, so expanding from $1 million to $2 million costs approximately $250 to $375 total.

This makes umbrella coverage cheaper than most people spend monthly on streaming services. Your actual premium depends on specific factors including driving history, claims history, credit score, and whether you own pools or rental properties. A DUI or multiple accidents can raise rates 25 to 40 percent, but even with these increases, umbrella coverage remains remarkably inexpensive relative to the financial devastation a major lawsuit creates.

Pool ownership might add $50 to $150 annually, but that’s still less than $30 per month for protection against catastrophic liability. Bundling your umbrella policy with your existing auto and homeowners coverage typically reduces total premiums by 5 to 15 percent compared to purchasing policies separately.

Wealth Isn’t Required for Protection

You absolutely don’t need a six-figure net worth to benefit from umbrella protection. Anyone with meaningful assets-a paid-off car, retirement savings, home equity, or investment accounts-has something worth protecting. A household with $300,000 in home equity, $100,000 in retirement savings, and $50,000 in liquid investments has $450,000 in assets that a lawsuit judgment could claim.

Without umbrella coverage, that family faces genuine financial devastation from a single serious incident. Utah residents at all income and wealth levels encounter the same liability risks: dog bites, slip-and-fall accidents, vehicle collisions, and recreational injuries. These incidents don’t discriminate based on net worth.

A single catastrophic claim can exceed $1 million in medical expenses and legal fees regardless of whether you’re wealthy or middle-class. Umbrella insurance exists precisely to protect ordinary families who’ve built modest wealth and can’t afford to lose it.

Final Thoughts

Medical costs for serious injuries now routinely exceed $500,000, and legal defense expenses alone can reach $150,000 or more. When a lawsuit judgment arrives, courts seize assets you’ve already built without regard for your income or intentions. Utah’s uninsured motorist rate of 8.5% means your collision exposure exceeds national averages, while outdoor recreation culture and pool ownership multiply liability risks that standard policies won’t cover.

The financial protection umbrella coverage provides costs remarkably little relative to what you stand to lose. At $175 to $300 annually for $1 million in coverage, you spend less than most people allocate to monthly subscriptions. Each additional million costs roughly $75 per year, making comprehensive personal umbrella Utah tips genuinely affordable for families at any income level.

We at Direct Insurance Services shop multiple top-rated carriers to find coverage that matches your actual risk profile and budget. Protect what you’ve built before a lawsuit forces you to start over.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation