Affordable homeowners insurance Utah: Smart Ways To Protect Your Home

Utah homeowners face real risks from hail, flash floods, and wildfires that standard policies often don’t cover fully. At Direct Insurance Services, we’ve helped hundreds of Utah families find affordable homeowners insurance that actually protects what matters most.

The good news? You don’t need to choose between low premiums and solid coverage. This guide shows you exactly how to get both.

Why Utah Homeowners Need Real Protection

Utah’s weather patterns hit different than most states, and your standard homeowners policy probably doesn’t cover what you actually need. Wildfires rank ninth nationally for homes at risk, according to the Insurance Information Institute, and Utah sits directly on the Intermountain Seismic Belt, meaning earthquake damage isn’t automatically covered. Flash floods strike regularly-the state experiences significant precipitation events that standard policies explicitly exclude. From 2020 to 2023, homeowners in Weber County saw premiums jump 86.4%, while Summit County nearly doubled, according to data from the National Bureau of Economic Research and CoreLogic. These increases reflect real claims from real disasters, not theoretical risks.

What Your Basic Policy Actually Leaves Out

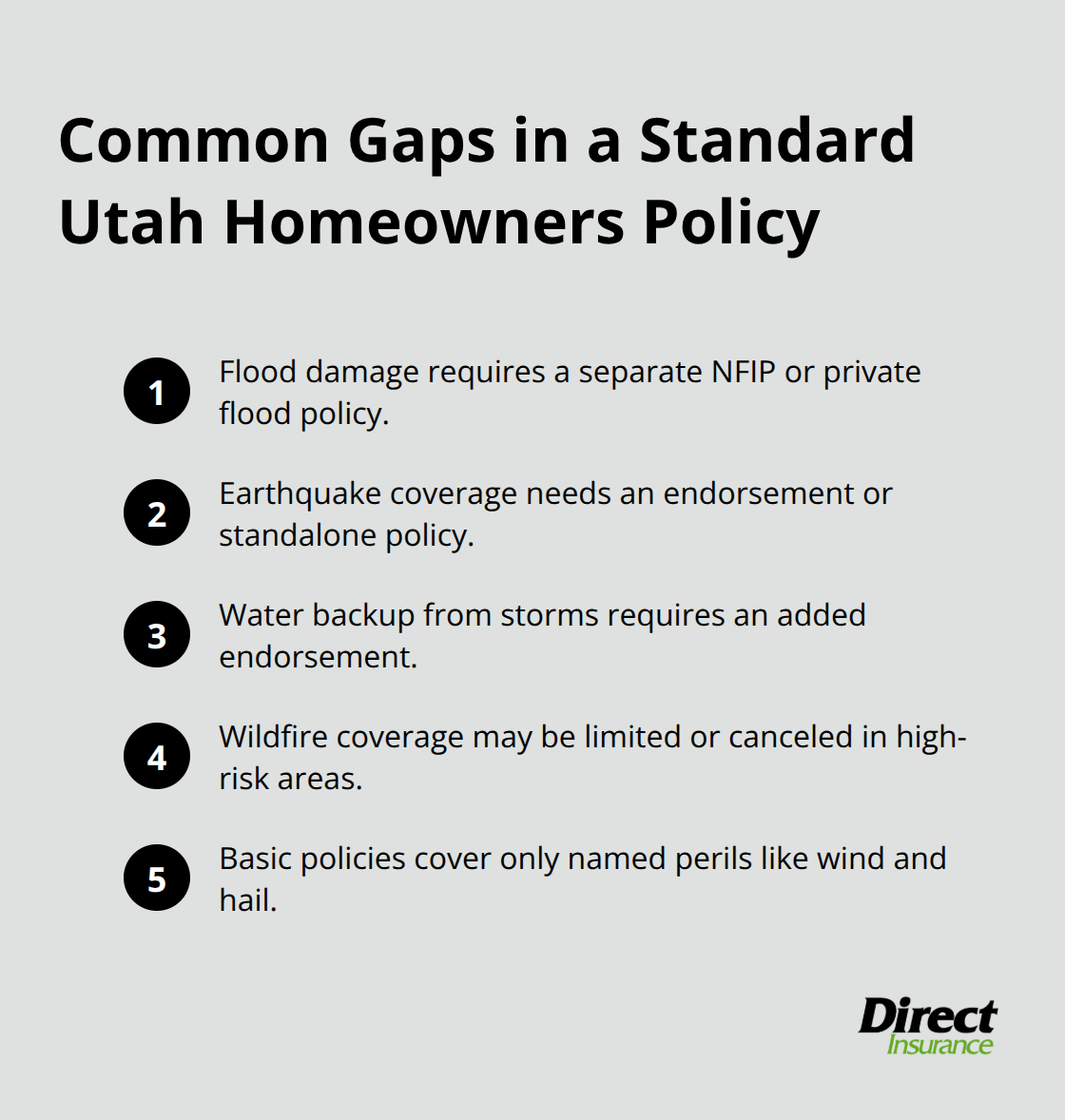

A standard Utah homeowners policy covers dwelling damage, personal property, liability, and loss of use-but only for named perils like wind and hail. Flood damage requires a separate National Flood Insurance Program policy or private flood coverage. Earthquake coverage needs its own endorsement or standalone policy.

Wildfire damage falls under standard policies technically, but many carriers tighten coverage or cancel policies in high-risk areas entirely. Water backup from storms (different from flood coverage) requires an additional endorsement. If your home sits in an older neighborhood or has outdated plumbing and electrical systems, insurers may deny claims or offer limited coverage. The gap between what you think you’re covered for and what you actually are covered for creates real exposure.

Why Premiums Keep Rising in Utah

Construction costs in Utah have skyrocketed, forcing insurers to raise rates to match replacement values. A 2,000-square-foot home now costs roughly $175 per square foot to rebuild, pushing dwelling coverage requirements higher. Inflation hasn’t stopped-the average Utah policy costs about $1,541 annually according to the National Association of Realtors, up significantly from previous years. Climate change makes severe weather more frequent, which drives up reinsurance costs that carriers pass directly to you. Salt Lake County homeowners saw premiums rise from $1,045 in 2020 to a projected $1,578 by 2026. This trend won’t reverse, which means waiting to secure proper coverage only costs more later.

Finding Coverage That Matches Your Real Risks

You need to assess your home’s actual replacement cost, not its market value. Most Utah homeowners underestimate what it truly costs to rebuild after a total loss. Add coverage for water backup if your property sits in a flood-prone area. Consider earthquake endorsements seriously-the Intermountain Seismic Belt poses genuine risk to Utah properties. Wildfire mitigation steps (clearing dead vegetation, upgrading roofing materials) can help you maintain coverage in high-risk zones and may qualify you for premium discounts. Shopping multiple insurers reveals significant rate differences; American Family averages about $1,476 annually for $500,000 dwelling coverage in Utah, while USAA runs roughly $1,533 and State Farm around $1,508. These variations mean your choice of carrier directly impacts your wallet.

The smarter move is locking in affordable rates now with coverage that actually matches your home’s true replacement cost and Utah’s specific risks. Once you understand what gaps exist in basic policies and why premiums reflect real exposure, you’re ready to find the right insurer at the right price.

How to Find the Best Rates on Utah Homeowners Insurance

Compare Multiple Carriers to Uncover Real Savings

Shopping multiple insurers isn’t optional if you want affordable coverage-it’s the only way to see what you’re actually paying for. American Family, USAA, State Farm, Allstate, and Farmers all operate in Utah, but their rates vary dramatically by ZIP code and home profile. A $500,000 dwelling policy costs roughly $1,476 annually with American Family, $1,533 with USAA, and $1,508 with State Farm according to U.S. News data. That $57 difference between American Family and State Farm multiplies across years. Requesting quotes from at least three carriers takes about 30 minutes and reveals which insurer values your specific property type. Don’t settle for one quote-premiums shift based on your roof age, home construction materials, and proximity to wildfire zones.

An independent agent who shops multiple carriers simultaneously saves you time and often uncovers rates you wouldn’t find calling companies individually. Most people discover they can save $200 to $400 annually just by switching to a carrier that fits their risk profile better.

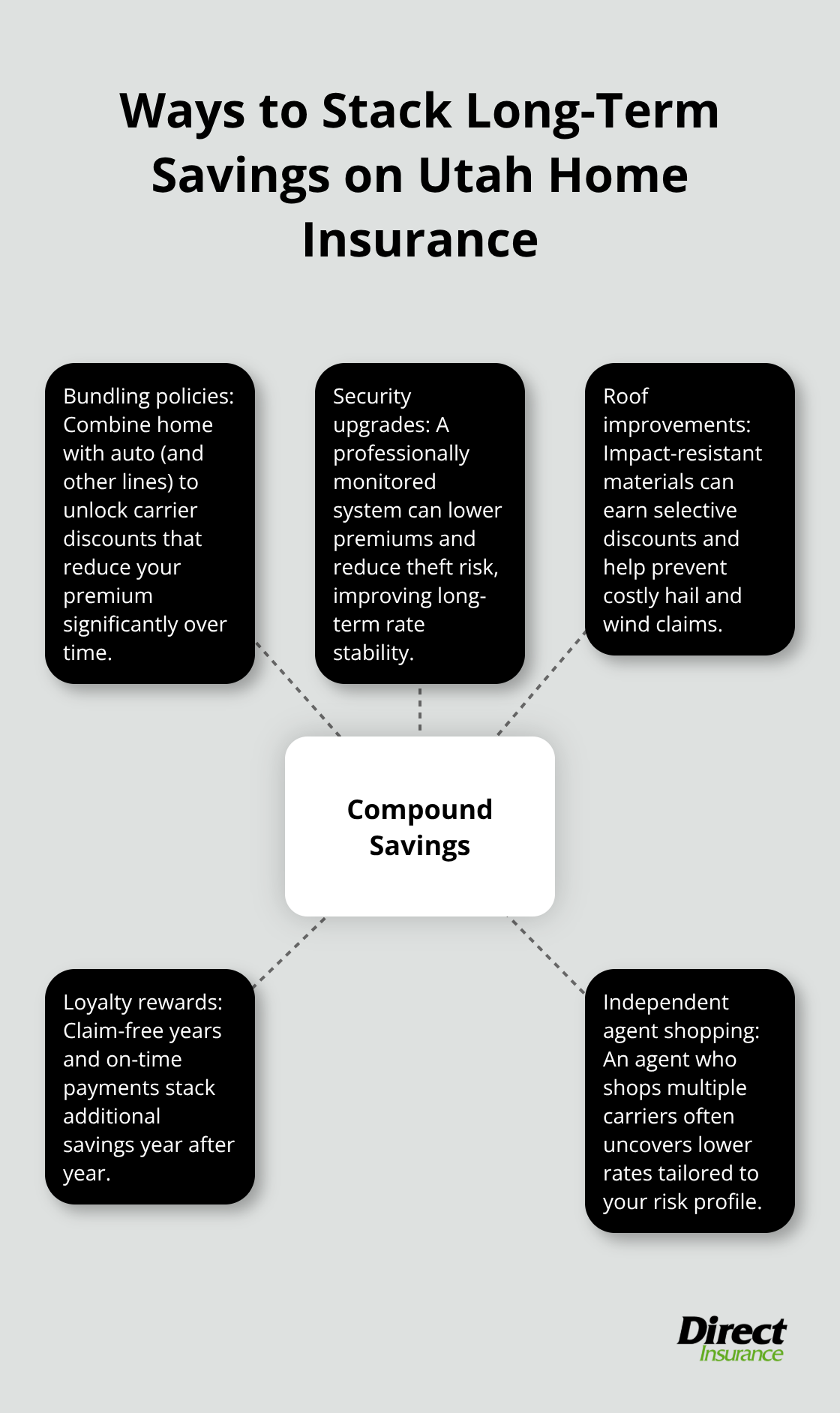

Stack Discounts Through Bundling and Safety Upgrades

Bundling homeowners insurance with auto coverage produces immediate savings that single-policy shopping can’t match. Carriers typically discount bundled policies by 10% to 25%, meaning you might pay $150 to $300 less per year on your home policy alone when combined with auto insurance. If you carry renters, life, or umbrella policies, stacking them with homeowners amplifies discounts further. Beyond rate reductions, bundling simplifies billing and creates one relationship instead of managing multiple insurers.

Safety upgrades directly reduce premiums on both policies. A monitored security system can lower costs according to insurers who recognize this risk and may offer better premium discounts for professionally monitored home security systems. Fire extinguishers, smoke detectors, and deadbolt locks qualify for modest discounts with most carriers. Roof upgrades matter more; upgrading to impact-resistant materials meeting wind mitigation standards can yield discounts up to 15% in some cases, though Utah insurers apply these selectively based on local weather patterns.

Maximize Long-Term Savings With Loyalty Rewards

Before upgrading your home, confirm your carrier offers discounts for specific improvements-some don’t reward roof work as heavily as others do. Loyalty rewards for claim-free years and on-time payment histories stack on top of these discounts, creating compound savings over time. The combination of bundling, security improvements, and claims-free status often cuts your total premium by 30% or more compared to a new policyholder paying full rates.

These rate reductions set the foundation for affordable protection, but your actual coverage quality depends on selecting the right policy limits and endorsements for Utah’s specific risks.

How to Cut Your Premium Without Cutting Coverage

Raise Your Deductible to Lower Monthly Costs

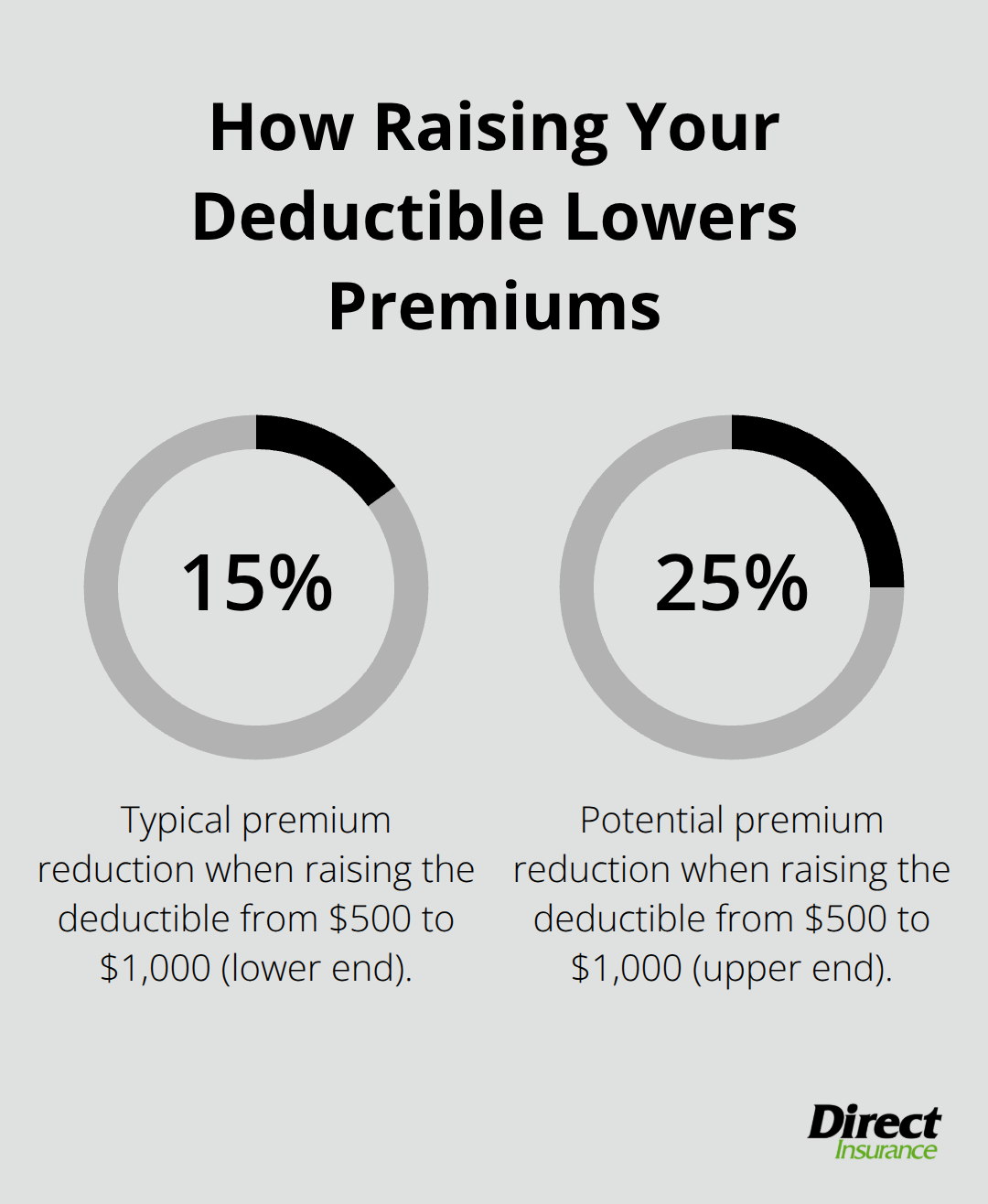

Your deductible is the most direct lever you control to reduce premiums. Raising your deductible from $500 to $1,000 typically cuts your annual premium by 15% to 25%, depending on your carrier and home profile. For a Utah homeowner paying $1,541 annually according to the National Association of Realtors, that jump means saving $230 to $385 per year.

The math works if you can actually afford to pay $1,000 out-of-pocket after a claim. If you’d struggle to cover that amount, a $750 deductible strikes a better balance-still meaningful savings without creating financial stress when you need coverage most. Salt Lake County residents seeing projected premiums climb to $1,578 by 2026 should calculate whether raising deductibles now shields them from future rate increases better than accepting higher monthly costs.

Install Security and Fire Detection Systems

Home security systems deliver measurable premium reductions that justify their upfront investment. A monitored system typically reduces your premium by 2% to 15%, with average savings around $100 annually according to Policygenius. Most systems cost $150 to start with ongoing monthly service fees around $15 to $30, meaning you recoup installation costs within two years through premium reductions alone. Fire detection systems, smoke alarms, and sprinkler systems qualify for similar discounts with most Utah carriers. Beyond premium savings, these systems lower your actual risk of theft and fire damage, which means fewer claims and better long-term rate stability.

Maintain Your Roof and Property

Roof maintenance and upgrades matter enormously in Utah’s hail-prone climate. Replacing an older roof with impact-resistant roofing materials can yield discounts and may qualify you for a homeowners insurance discount. The real payoff comes from preventing claims entirely-a home with a well-maintained roof, clear gutters, and trimmed trees avoids the water damage and debris impact claims that drive rate increases. Property maintenance costs money upfront but prevents the expensive claims that follow negligence.

Combine Discounts for Maximum Savings

Utah homeowners who bundle auto and home policies while maintaining security systems and claim-free records often see combined savings of 30% or more compared to new policyholders paying standard rates. Each discount stacks on top of the others, creating compound savings over time. Your carrier’s specific discount structure determines which improvements matter most for your situation, so confirm what qualifies before investing in upgrades.

Final Thoughts

Affordable homeowners insurance in Utah requires you to compare rates across multiple carriers, stack discounts through bundling and safety upgrades, and adjust deductibles to match your financial situation. American Family, USAA, and State Farm offer dramatically different premiums for identical coverage, bundling cuts your costs by 10% to 25%, and raising your deductible from $500 to $1,000 saves $230 to $385 annually. These aren’t theoretical savings-they represent real money back in your pocket every year.

ZIP code matters enormously in Utah since a property in Summit County faces different wildfire and earthquake exposure than one in Salt Lake County, and your premium should reflect that reality. A monitored security system, impact-resistant roof, or maintained property all qualify for discounts, but only if your carrier recognizes them. Shopping alone takes time and often misses carrier-specific discounts you’d qualify for with an independent agent who shops multiple top-rated companies simultaneously.

We at Direct Insurance Services understand Utah’s unique risks-wildfires, hail, earthquakes, and rising construction costs-because we live here and have spent over 50 years helping Utah families find coverage that actually protects their homes while keeping premiums manageable. Contact Direct Insurance Services today for personalized quotes that compare your options side by side, and most people discover they can save hundreds annually while actually improving their coverage. Your home is your largest asset, and protecting it affordably shouldn’t require guesswork.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation