Landlords Liability Coverage: Understanding Your Policy

As a landlord, you face unique risks that standard homeowners insurance won’t cover. A single tenant injury or property damage claim can cost you thousands in legal fees and settlements.

Landlord’s liability coverage protects your rental business from these financial threats. At Direct Insurance Services, we help property owners understand their policies so they can make informed decisions about their protection.

What Landlord’s Liability Coverage Actually Protects

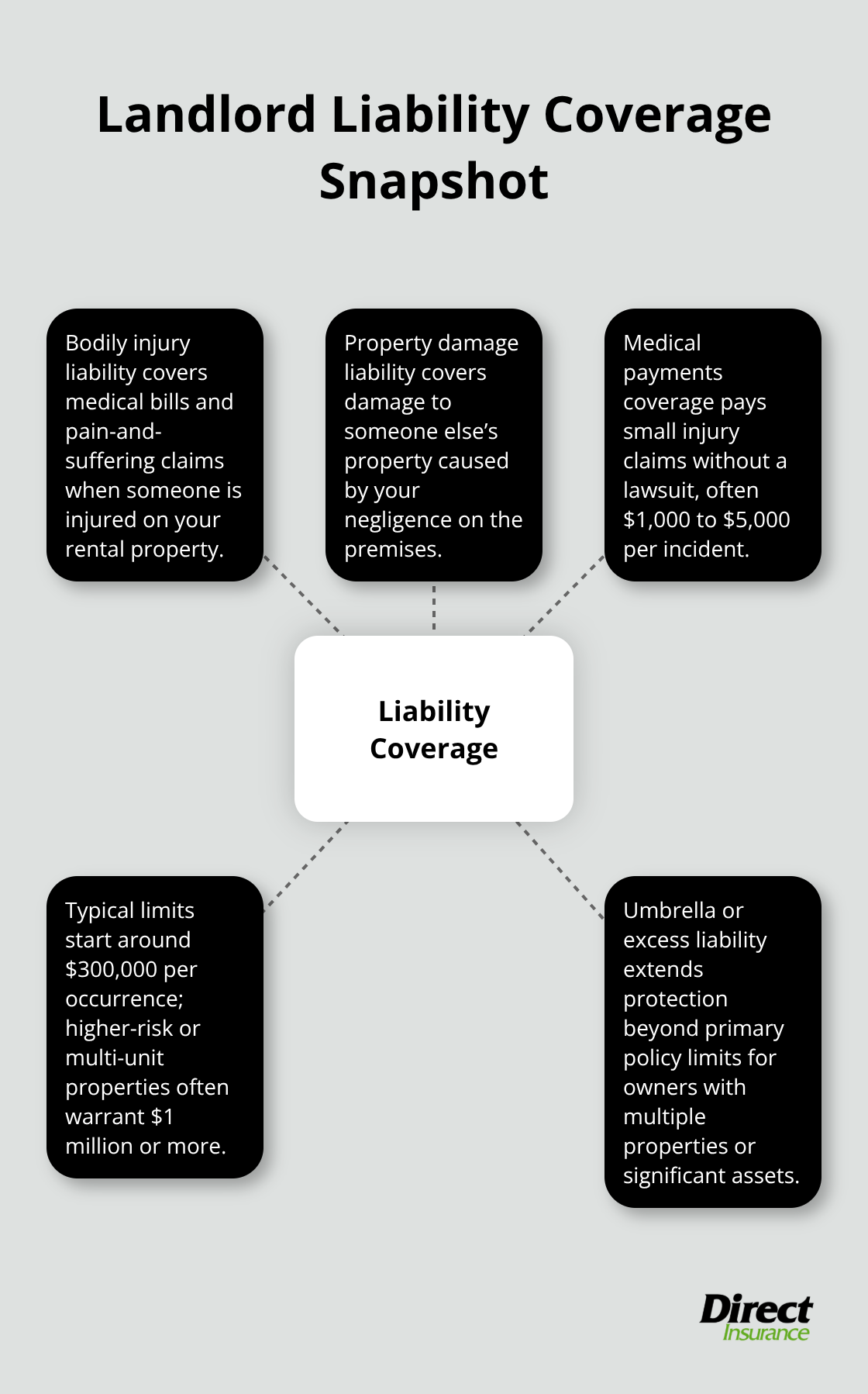

Landlord’s liability coverage protects you when someone gets injured on your rental property or their property gets damaged due to conditions you’re responsible for maintaining. This isn’t about damage to your building-that’s covered separately under dwelling coverage. Liability specifically covers third-party claims, meaning injuries or damage to tenants, guests, or visitors. According to the Insurance Information Institute, liability coverage also pays for legal defense costs if you’re sued, with hourly rates typically ranging from $150 to $350 per hour.

How Liability Coverage Splits Into Two Categories

The coverage typically splits into two categories: bodily injury liability covers medical bills and pain-and-suffering claims from injuries, while property damage liability covers damage someone else’s property suffers because of your negligence. Most landlord policies include medical payments coverage as well, which pays small injury claims without requiring a lawsuit-often $1,000 to $5,000 per incident. Standard liability limits start around $300,000 per occurrence, though properties with multiple units or higher values warrant $1 million or more.

If you own multiple rental properties or significant assets, umbrella or excess liability insurance extends protection beyond your primary policy limits and is worth serious consideration.

Common Claims That Liability Covers

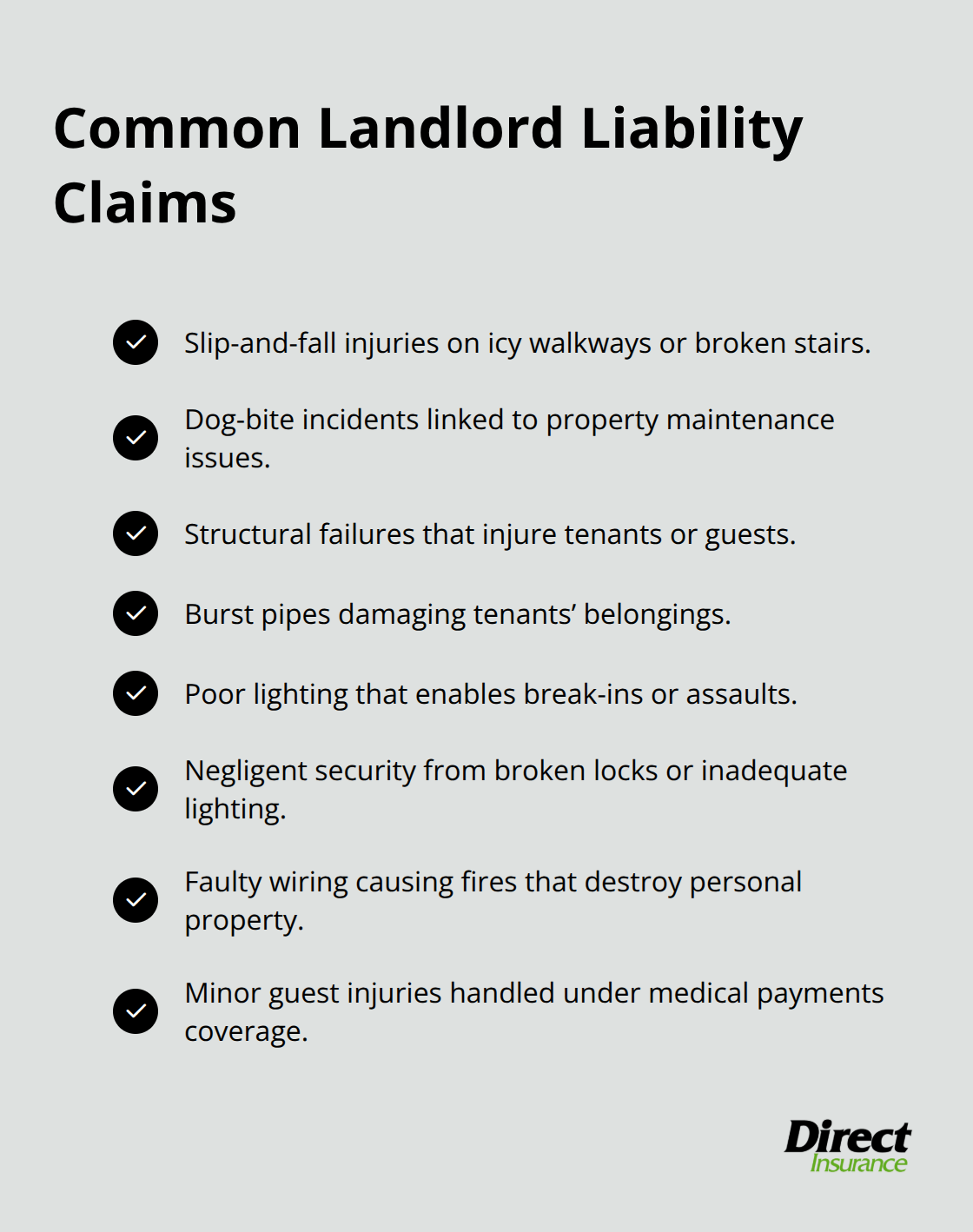

Slip-and-fall injuries are the most frequent landlord liability claims, according to the Insurance Information Institute. A tenant slips on ice you failed to clear, or a guest falls on a broken stair you knew about but didn’t repair-both trigger liability coverage. Dog-bite injuries also appear regularly; if your property maintenance failed to prevent a tenant’s guest from being attacked, you could face a claim. Structural failures like ceiling collapse, burst pipes that flood a tenant’s belongings, or poor lighting that enables a break-in also fall under liability. Negligent security creates significant exposure-if you ignored broken locks or failed to maintain adequate exterior lighting and someone is assaulted, liability coverage responds. Property damage claims arise when your negligence damages a tenant’s personal property; for example, if your faulty wiring causes a fire that destroys their furniture and electronics.

Medical payments coverage handles smaller incidents without litigation, such as a guest’s minor injury that needs emergency room treatment.

What Standard Landlord Policies Exclude

Standard landlord policies explicitly exclude professional services, intentional acts, and wear-and-tear damage. If you intentionally harm someone or deliberately create a hazard, coverage vanishes. Mold from water damage often carries exclusions or severe sublimits unless you add specific endorsements. Pre-1978 properties require EPA lead-based paint disclosures, but lead exposure claims may face coverage disputes or exclusions if you didn’t follow disclosure rules. Asbestos exposure creates liability you must manage through proper disclosure and professional remediation, though coverage for asbestos-related claims is typically excluded. Short-term rental activity like Airbnb or Vrbo frequently falls outside standard landlord policies-insurers view frequent guest turnover as commercial activity requiring separate commercial liability coverage. Maintenance-related issues can be tricky; if you ignored repeated requests to fix a hazard, an insurer might deny the claim arguing negligence was your responsibility to prevent. Vacancy periods increase risk substantially, and many standard policies exclude or heavily limit liability coverage when a property sits empty for extended periods.

Understanding Your Policy’s Fine Print

You need to review your policy exclusions carefully with your agent, because gaps here can leave you exposed to exactly the claims most likely to occur. The specific exclusions in your contract depend on the form your insurer uses (DP-1, DP-2, or DP-3) and any endorsements you’ve added. Each property type-single-family homes, multi-unit buildings, condos, or short-term rentals-carries different exclusion patterns and coverage needs. Your agent can walk you through which exclusions apply to your situation and recommend endorsements that fill critical gaps. Understanding what your policy actually excludes is the first step toward identifying whether you need additional coverage layers like umbrella policies or specialized short-term rental protection.

Why Liability Coverage Protects Your Assets

The Legal and Financial Reality of Uninsured Liability

Landlord liability coverage isn’t optional if you want to keep your assets safe from legal judgment. Most states don’t legally mandate liability insurance on rental properties, but mortgage lenders often require it as a loan condition, and tenants increasingly expect landlords to carry adequate protection. Without liability coverage, a single lawsuit drains your bank account faster than you’d anticipate. Attorney fees in landlord-tenant disputes range from $225 to $300 on average across the US, and a contested case accumulates additional costs before trial even begins. Medical bills from a serious injury claim often exceed $50,000, and jury awards for pain and suffering reach six figures depending on injury severity and jurisdiction.

How One Claim Destroys Financial Security

The financial reality is stark: one major claim destroys a landlord’s portfolio. If someone suffers a permanent injury on your rental property due to a hazard you failed to fix, compensatory damages alone might reach $100,000 to $250,000 depending on severity and state law. Punitive damages can double or triple that amount if negligence was egregious. Without liability coverage, you pay from your personal funds, potentially forcing asset liquidation or bankruptcy. Properties with multiple units carry higher exposure because more people transit the premises regularly, increasing slip-and-fall and injury incidents. Environmental hazards like lead paint exposure in pre-1978 buildings or mold from water damage create substantial liability if you failed to disclose or remediate properly.

Short-Term Rentals and Elevated Risk

Short-term rental properties face dramatically higher claims frequency. Airbnb and Vrbo properties see guest injuries at rates that standard landlord policies often exclude entirely, meaning you absorb 100 percent of costs. A guest injury claim on a short-term rental can exceed $50,000 in medical expenses alone, plus legal defense costs that mount quickly. The guest turnover model creates continuous exposure-each new occupant introduces fresh liability risk that long-term tenant relationships don’t generate. Properties rented through platforms like Airbnb require specialized coverage because standard policies explicitly exclude frequent guest activity.

The Math of Protection Versus Risk

Liability insurance costs $300 to $600 annually for typical single-family rentals, while one lawsuit costs $10,000 to $100,000 or more. Carrying adequate coverage transforms a catastrophic financial risk into a manageable insurance expense. A $1 million liability limit protects your rental business and personal assets from the claims most likely to occur. The cost-benefit calculation is straightforward: you spend less than $1,000 per year to avoid potential losses that exceed $250,000. Multi-unit properties and short-term rentals warrant higher limits and umbrella coverage because exposure scales with occupancy and guest frequency.

Choosing Coverage Limits That Match Your Exposure

Your liability limits should reflect your property’s specific risk profile, not just industry minimums. A single-family home in a low-crime area with minimal foot traffic might operate safely at $300,000 per occurrence, while a three-unit building in an urban location warrants $1 million or more. Properties with pools, stairs, or other hazardous features require higher limits because injury claims from these features tend to be more severe. If you own multiple rental properties or significant personal assets, umbrella coverage extending $1 million to $2 million beyond your primary policy limits provides critical protection. Your next step involves assessing your specific property characteristics and risk factors to determine whether standard liability limits adequately protect your financial position.

How to Choose the Right Coverage Limits for Your Rental Property

Assess Your Property’s Specific Risk Profile

Selecting the right liability limits requires honest assessment of your property’s specific characteristics, not just copying industry minimums. A single-family home in a quiet neighborhood carries different risk than a four-unit building in a high-traffic urban area, yet many landlords apply the same $300,000 limit across properties with vastly different exposure levels. Start by documenting your property’s physical features: the number of units, building age, presence of stairs or pools, exterior lighting quality, and local crime rates. Properties built before 1978 introduce lead paint liability that newer homes avoid entirely. Multi-unit buildings generate more foot traffic and tenant turnover, which increases slip-and-fall and injury incidents substantially. If your property sits in an area with higher crime rates, negligent security claims become more probable, which means your liability limits should exceed baseline recommendations.

Understand How Property Type Affects Coverage Needs

Short-term rental properties warrant significantly higher limits than long-term rentals because guest turnover creates continuous exposure. A $1 million limit represents the minimum for frequent short-term activity, not the standard. The Insurance Information Institute recommends starting at $300,000 per occurrence for single-family homes but emphasizes that properties with multiple units or significant asset value should carry $1 million or higher. Once you’ve documented these risk factors, compare your current limits against your actual exposure. Most landlords discover their existing coverage falls short after honestly evaluating their property’s characteristics.

Balance Deductibles Against Your Financial Capacity

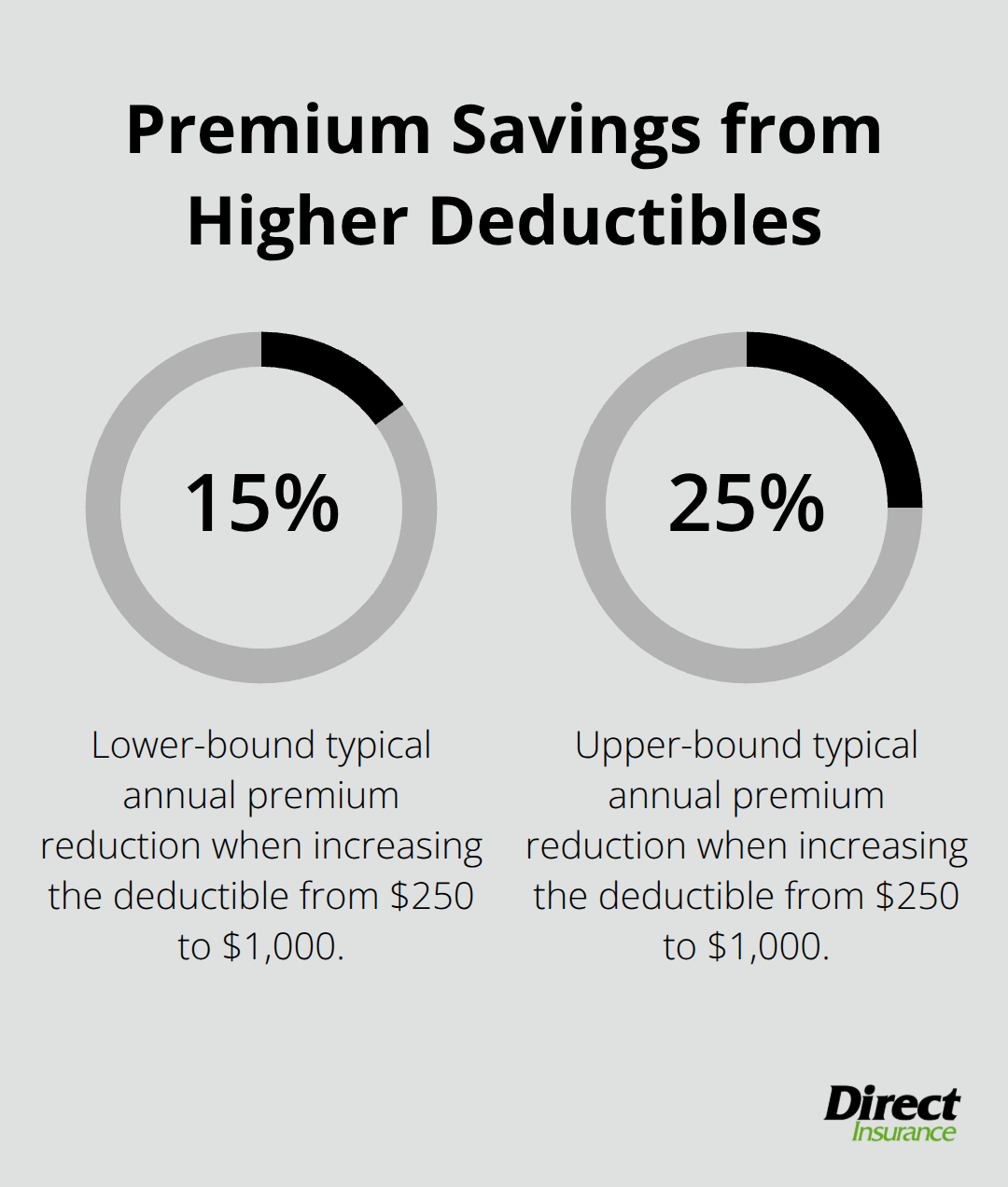

Deductibles directly impact both your premium costs and out-of-pocket expenses when claims occur, making this decision far more important than many landlords realize. Raising your deductible from $250 to $1,000 typically reduces your annual premium by 15 to 25 percent, savings that sound attractive until you face a legitimate claim that requires thousands in legal defense before your coverage activates. The correct deductible balances premium savings against your actual ability to absorb out-of-pocket costs without financial strain.

If you own multiple rental properties, a higher deductible across your portfolio makes sense because you can distribute costs; if you own one property, a lower deductible protects you from catastrophic expense.

Calculate What You Can Actually Afford Out-of-Pocket

Legal defense costs often reach $5,000 to $15,000 before a claim settles, meaning your deductible should never exceed what you can comfortably pay from available cash reserves. Consider that amount carefully-your deductible should reflect what you can actually afford without jeopardizing your financial stability. If you cannot comfortably cover $1,000 from savings when a claim arrives, a $500 deductible makes more sense despite slightly higher premiums. The savings from a higher deductible evaporate instantly when you face a $10,000 legal defense bill that your deductible forces you to absorb personally.

Work with an Agent to Customize Your Coverage

An insurance agent who understands your specific situation transforms this from a guessing game into a strategic decision. Your agent reviews your property documentation, rental history, and assets to recommend limits and deductibles that genuinely protect your financial position rather than simply reducing your premium. An agent walks you through which exclusions apply to your situation and recommends endorsements that fill critical gaps. Avoid the temptation to maximize deductibles purely for lower premiums; the real protection comes from coverage that matches your actual exposure and financial capacity.

Final Thoughts

Landlord liability coverage protects your financial security from the claims most likely to damage your rental business. A single lawsuit costs tens of thousands in legal fees and settlements, while adequate coverage costs a few hundred dollars annually. Your liability limits must match your actual exposure, not industry minimums that may leave you exposed to catastrophic loss.

Single-family homes typically operate safely at $300,000 per occurrence, while multi-unit buildings and short-term rentals warrant $1 million or higher. Building age, property location, and hazardous features like pools or stairs all influence how much protection you genuinely need. Standard landlord policies exclude professional services, intentional acts, mold, lead exposure, and short-term rental activity unless you add specific endorsements, so understanding these gaps prevents shock when you file a claim.

Schedule time with an insurance professional who understands your situation and can recommend limits and endorsements that genuinely protect your financial position. We at Direct Insurance Services shop multiple top-rated insurers to match your specific needs and budget, and our team in Salt Lake City specializes in helping landlords find the right coverage for their rental properties. Policy reviews should happen annually or whenever your property changes, because renovations, tenant turnover, or acquisitions alter your risk profile and may require coverage adjustments.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation