Best Auto and Home Insurance Bundle Deals

Bundling your auto and home insurance policies is one of the smartest financial moves you can make. Most insurers offer discounts between 15% and 25% when you combine these two policies, which adds up to real savings on your annual premiums.

At Direct Insurance Services, we help customers find the best auto and home insurance bundle deals tailored to their specific needs. This guide walks you through how bundles work, what to compare across insurers, and how to maximize your savings.

How Bundle Discounts Actually Work

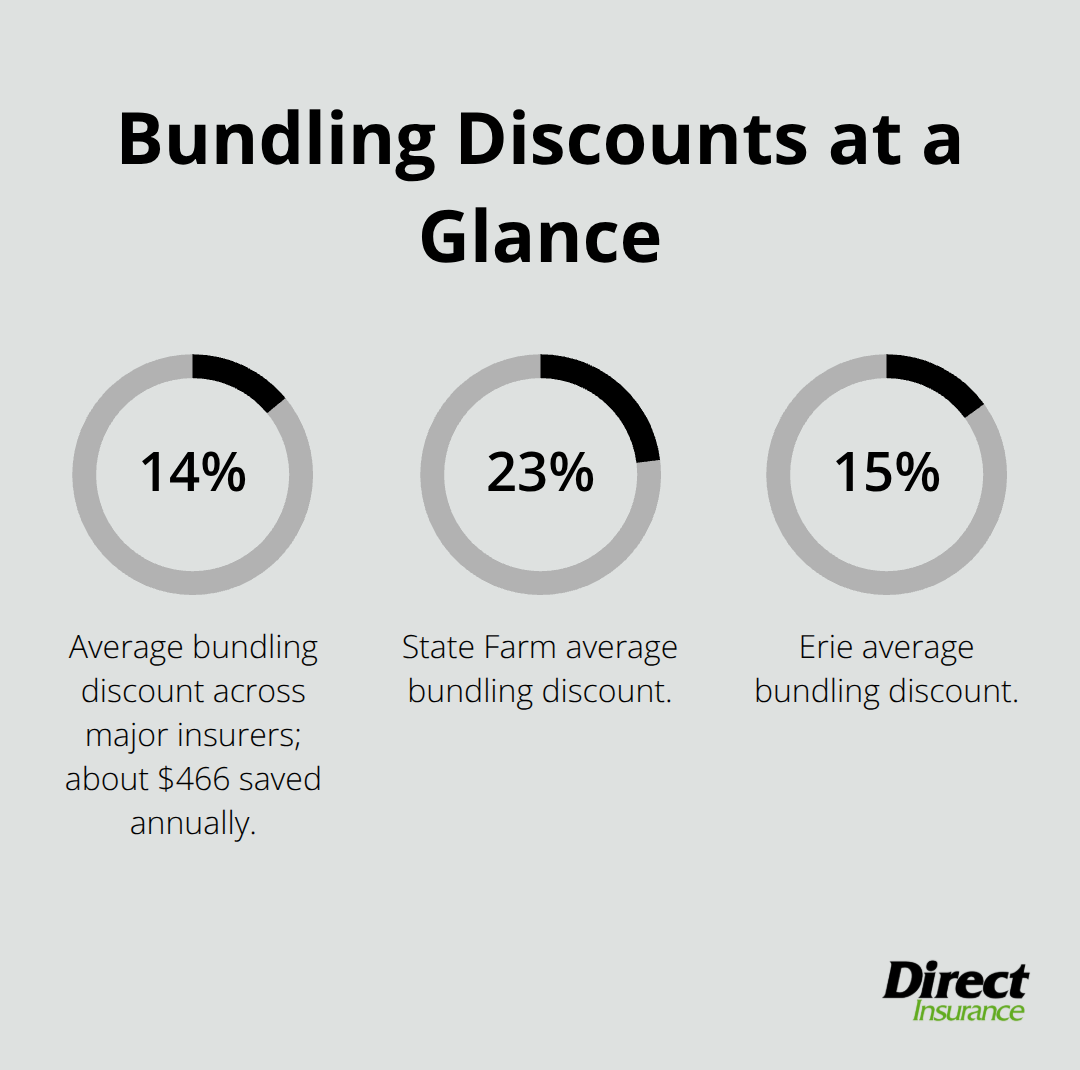

When you combine auto and home insurance with the same carrier, you don’t get a single merged policy. Instead, you keep two separate policies with two separate policy numbers, but the insurer applies a discount to your combined premium. Forbes Advisor analyzed 672 auto and home rates and found that the average bundling discount across major insurers sits at 14%, which translates to roughly $466 in annual savings. State Farm leads with a 23% average bundling discount, while Erie follows at 15%. The discount applies to the total of both policies rather than to individual lines, so a carrier might reduce your combined auto and home cost by 14% instead of discounting each policy separately.

Managing Your Deductibles

This structure matters because you remain responsible for managing two deductibles unless your insurer offers a single deductible option for events affecting both your home and vehicle. Some carriers like Erie include this feature, which can significantly reduce out-of-pocket costs if a single incident damages both properties. When you evaluate bundle options, ask whether the insurer provides a single deductible benefit-this detail can save you thousands if you ever file a claim.

The Hidden Financial Advantages

The real financial advantage extends beyond the headline discount percentage. Insurers reduce their administrative costs when they handle one customer relationship instead of two, and they pass some of those savings to you. You also benefit from simplified billing, often receiving one statement instead of two, and managing both policies through a single online account or app. Forbes Advisor found that the cheapest bundled quotes came from Auto-Owners at approximately $1,878 annually, followed by American Family at $2,178. These prices already reflect bundling discounts, so the savings are baked in.

Stacking Additional Discounts

Many bundlers stack additional discounts on top of the multi-policy discount, such as safe-driver discounts, loyalty discounts, or low-mileage discounts, which multiplies your total savings potential beyond the standard 14% to 25% range. You also eliminate the risk of coverage gaps when switching insurers, since you can coordinate policy effective dates to move both policies simultaneously. Understanding how these layers of savings work helps you identify which carriers offer the most value for your situation-and that’s exactly what we’ll explore when comparing specific bundle deals from different insurers.

Which Bundle Deal Actually Saves You the Most

Comparing bundle deals across insurers requires more than glancing at discount percentages. State Farm advertises a 23% bundling discount, but Erie customers report 15% savings, and the actual dollar amounts differ dramatically depending on your location and risk profile. Forbes Advisor’s analysis of 672 auto and home rates revealed that Auto-Owners delivers the cheapest bundled quotes at approximately $1,878 annually, while State Farm customers pay around $2,587 for comparable coverage. The gap isn’t small, and it proves that the highest discount percentage doesn’t always mean the lowest final bill.

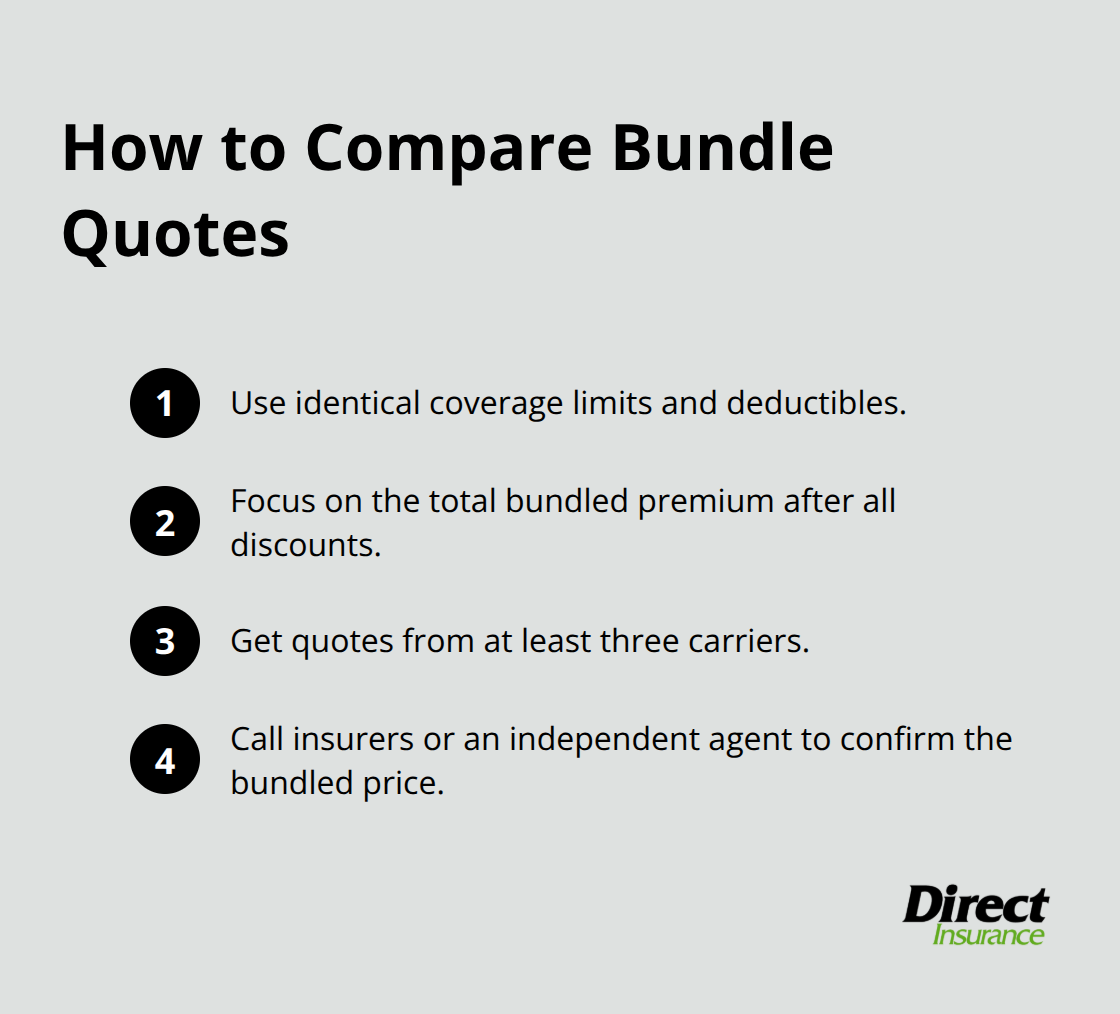

Request Quotes Using Identical Coverage

When you request quotes, ignore the marketing language and focus on the total bundled premium after all discounts apply. Request quotes from at least three carriers using identical coverage limits and deductibles so you’re comparing apples to apples. Many online quote tools don’t show bundling discounts automatically, so call insurers directly or work with an independent agent to confirm the bundled price.

Ask each insurer specifically how they calculate the multi-policy discount and whether additional discounts stack on top of the bundle offer. Progressive customers bundling auto and home report savings exceeding 25% in some cases, but this varies significantly by state and personal factors like driving history and home age.

Uncover Hidden Terms That Affect Your Savings

Bundling agreements contain terms that dramatically affect your actual savings. Some insurers require you to maintain minimum coverage levels on both policies to qualify for the bundled discount, meaning you can’t lower your home liability limit to reduce costs without losing the discount entirely. Others apply the bundle discount only if you pay annually rather than monthly, which forces you to pay a larger lump sum upfront. Check whether the insurer charges a fee for policy changes or cancellations, since bundled customers often face higher exit costs.

Ask About Single Deductible Features

Ask about the single deductible feature explicitly, because only some carriers offer it, and this benefit can save thousands during a claim. State Farm’s analysis shows bundled customers save an average of $787 annually through their 23% discount, but this figure assumes you maintain their recommended coverage levels. Review the fine print on how discounts apply if you add a second vehicle or a rental property later, since some insurers reduce or eliminate bundle discounts when you add new policies. Request a full disclosure of any rate increases scheduled for renewal, because some carriers offer aggressive introductory bundled rates that jump substantially after year one.

Navigate the Details With Professional Help

Shopping multiple carriers and translating the real costs into straightforward comparisons takes time and attention to detail. An independent agent can help you compare these hidden terms across several insurers at once, saving you hours of phone calls and fine-print reviews. Once you’ve identified which bundle offers the lowest true cost and the most favorable terms, the next step involves maximizing those savings even further through strategic adjustments to your coverage and additional discounts that most customers overlook.

How to Cut Your Bundle Cost Without Cutting Coverage

The bundling discount you receive is just your starting point, not your final savings. Most customers stop after locking in the initial multi-policy discount and miss significant additional savings that compound over time. Customers frequently discover they’ve been overpaying for months or years because they never adjusted their coverage or stacked additional discounts on top of their bundle. The most aggressive way to maximize bundle savings involves three specific actions: ruthlessly evaluate whether your coverage limits match your actual needs rather than what the insurer suggests, aggressively layer every available discount your carrier offers, and treat your annual renewal as a mandatory renegotiation rather than a passive acceptance of rate increases.

Align Your Coverage Limits to Your Real Situation

Insurance companies build quote tools that default to higher coverage limits than most customers actually need, which inflates your premium unnecessarily. Your home’s replacement cost determines your dwelling coverage limit, and you can multiply your home’s square footage by average building costs per square foot in your area to obtain this figure. If your home would cost $350,000 to rebuild completely, insuring it for $500,000 wastes hundreds annually in premium. Similarly, your auto liability limits should reflect your actual assets at risk; if you own a home and have meaningful savings, carrying only the state minimum liability coverage exposes you to catastrophic financial loss in a lawsuit. Most states require minimum auto liability around $25,000 to $50,000 per person, but financial advisors recommend limits of at least $100,000 to $300,000 if you have substantial assets. Request a detailed breakdown from your insurer showing your current coverage limits and what you’re actually paying for each component, then compare this to your replacement cost estimates and net worth. Reducing unnecessary coverage while maintaining adequate protection typically saves 10% to 20% on your bundled premium.

Stack Every Discount Available Beyond Your Bundle

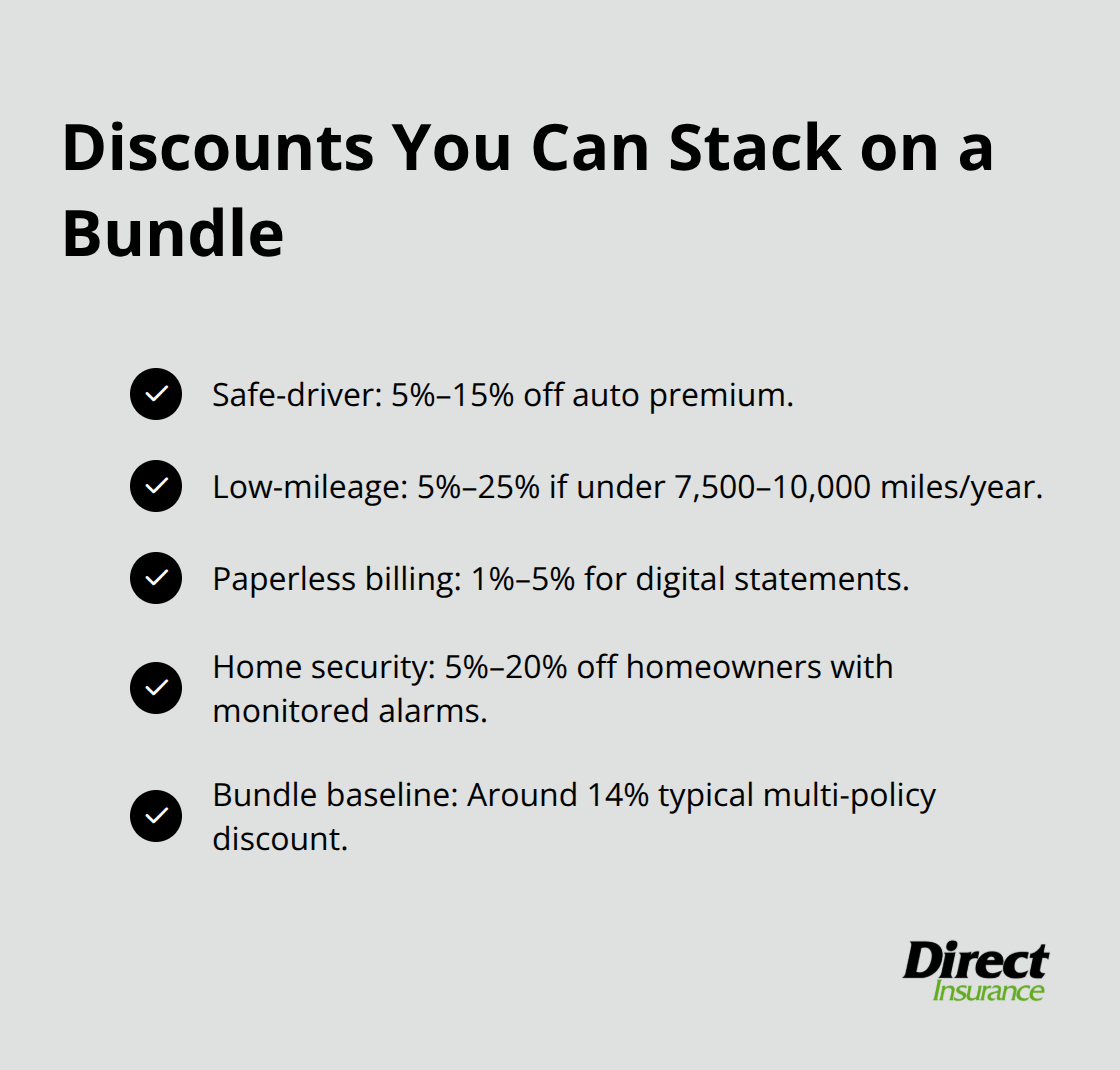

Your multi-policy discount is just one layer. Safe-driver discounts typically reduce your auto premium by 5% to 15% if you maintain a clean driving record for three to five years. Low-mileage discounts apply if you drive fewer than 7,500 to 10,000 miles annually and can save 5% to 25% depending on your carrier. Paperless billing discounts range from 1% to 5% and require nothing beyond switching to digital statements. Home security system discounts save 5% to 20% on your homeowners premium if you install monitored alarms, and some carriers offer discounts for having deadbolts, smoke detectors, or fire extinguishers.

Ask your insurer for a complete list of available discounts and confirm which ones apply to your bundled policies specifically, since bundle discounts sometimes restrict stacking. A customer who qualifies for safe-driver, paperless, and home security discounts alongside their 14% bundle discount can reduce their total premium by 30% to 40% compared to the base rate.

Treat Your Renewal as a Renegotiation Opportunity

Rate increases at renewal happen automatically unless you actively challenge them. Your insurer will send you a renewal notice showing your new premium, often 5% to 15% higher than your current rate, and most customers simply pay it. Instead, request a renewal quote from your current carrier and simultaneously obtain fresh quotes from two competing carriers using identical coverage. You’ll frequently discover that your current carrier’s renewal rate exceeds what competitors charge for the same protection. If you’ve maintained a clean record and haven’t filed claims, you have legitimate negotiating power to request a rate reduction or threaten to switch. Many insurers will match or beat competitor quotes to retain bundled customers because losing both auto and home policies costs them significantly more than offering a modest rate reduction. File a formal complaint with your state insurance commissioner if your carrier refuses to adjust rates and you can document better pricing elsewhere, which sometimes prompts carriers to reconsider. This annual renegotiation takes two hours but consistently saves customers $200 to $500 annually in cumulative savings over a five-year period.

Final Thoughts

Finding the best auto and home insurance bundle requires comparing actual dollar amounts across multiple carriers rather than chasing the highest discount percentages. State Farm advertises 23% savings while Auto-Owners delivers the lowest annual premiums at roughly $1,878, proving that marketing claims don’t always translate to your wallet. You now understand how bundle discounts work, what hidden terms to watch for, and exactly how to stack additional savings on top of your multi-policy discount through coverage adjustments and strategic discount layering.

The path forward involves three concrete actions: request bundled quotes from at least three carriers using identical coverage limits and deductibles so you compare apples to apples, ruthlessly evaluate whether your current coverage limits match your actual replacement costs and assets at risk rather than accepting the insurer’s defaults, and treat your annual renewal as a renegotiation opportunity instead of passively accepting rate increases because your negotiating power peaks when you have competing quotes in hand. We at Direct Insurance Services understand that navigating bundle options across multiple carriers takes time and expertise. Our team can help you compare bundle deals from different insurers, identify hidden terms that affect your savings, and build a customized coverage plan that fits your budget.

Rather than spending hours on phone calls and fine-print reviews, contact us to handle the heavy lifting so you move forward with confidence knowing you’ve found genuine value. Visit us at saltlakeinsurance.com to discuss your auto and home insurance needs with someone who understands your local situation and can deliver personalized service built on relationships, not transactions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation