How to Bundle Homeowner and Auto Insurance for Savings

Most homeowners pay more than they need to for insurance. Bundling your homeowner and auto insurance can cut your premiums significantly-often by 15% to 25% depending on your insurer.

At Direct Insurance Services, we’ve seen firsthand how many people leave money on the table by keeping their policies separate. This guide walks you through exactly how bundling works, what savings you can realistically expect, and how to find the best rates for your situation.

How Bundling Actually Works

What Bundling Means

Bundling means holding two or more insurance policies with the same company, and in return, that insurer gives you a discount on your total premiums. The mechanics are straightforward: insurers use bundling discounts to attract and retain customers. When you bring both your auto and homeowner policies under one roof, the insurance company reduces your rates because they manage less risk across multiple lines and you’re less likely to shop around.

The Real Discount Numbers

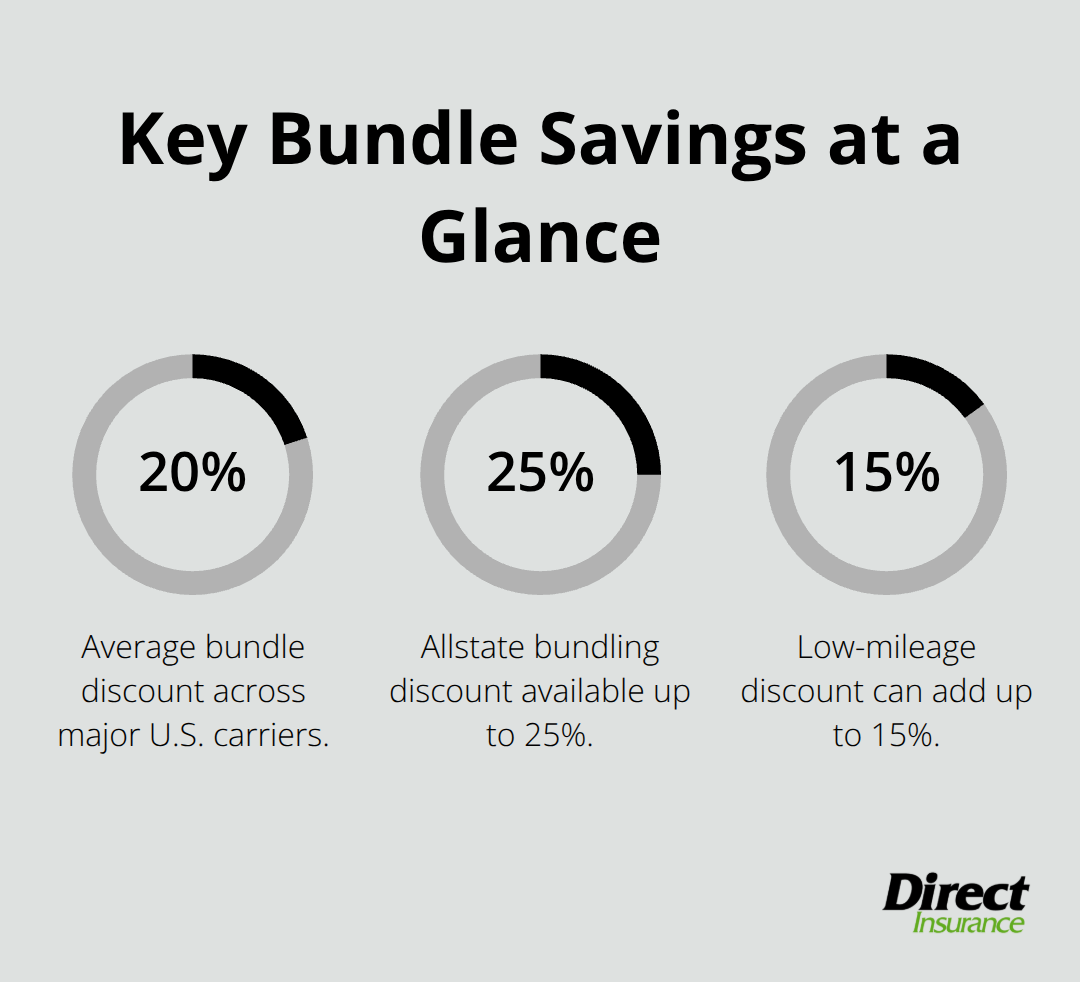

According to Bankrate’s 2025 analysis using Quadrant Information Services data, multi-policy discounts hover around 20% across major carriers. State Farm can save you up to $1,273 per year on a bundled auto and home policy, while Allstate offers bundling discounts up to 25%, Farmers averages about 20%, and Nationwide can save you up to 20% by bundling auto and home. The discount applies to both policies, not just one, so your auto premium drops and your homeowner premium drops simultaneously.

Most insurers keep your auto and homeowner policies as separate policies with different policy numbers, but you manage them in one place online or through a single agent. This separation means you maintain distinct coverage for each line while still receiving the bundled rate reduction.

How You Qualify for Bundle Discounts

Qualifying for bundle discounts requires nothing special on your end. You simply need to purchase both auto and homeowner coverage from the same insurer, and the discount applies automatically in most cases. Some insurers make you request quotes for both policies together to see the bundled rate, while others require a phone conversation with an agent rather than an online quote.

This variation is why comparing quotes across multiple insurers matters enormously-the bundled rate from one company might be significantly higher than another, even with the same discount percentage. When you shop, request quotes for auto and home from the same insurer and align coverage types and deductibles so you’re comparing apples to apples.

Stacking Additional Discounts

Check whether the insurer offers additional discounts alongside bundling, such as safe driver discounts, loyalty bonuses, or low-mileage discounts (these stack on top of your bundle savings and can add another 5% to 15% to your total savings). The combination of a 20% bundle discount plus a 10% safe driver discount, for example, creates meaningful additional protection for your wallet.

Understanding how these discounts layer together sets you up to make an informed choice. The next step involves knowing exactly what savings you can realistically expect and how to compare those numbers across different insurers.

What Savings Should You Actually Expect

The Real Numbers Behind Bundle Discounts

The 20% average bundling discount across major carriers that Bankrate’s 2025 analysis found serves as a useful benchmark, but your actual savings depend entirely on which insurer you choose and how their pricing works. State Farm can save you up to $1,273 per year on bundled auto and home coverage, while Allstate offers discounts up to 25%, Farmers averages around 20%, and Nationwide can save up to 20% when you bundle. The critical insight here is that these percentages don’t tell the whole story. A 25% discount from an insurer with higher base premiums might deliver less total savings than a 15% discount from a carrier with lower starting rates.

This is why comparing bundled quotes apples-to-apples across at least three insurers matters more than chasing the highest discount percentage. When you request quotes, align the deductibles, liability limits, and coverage types exactly across each company so you’re actually comparing the same protection level.

How Base Premiums Affect Your Bottom Line

Two insurers might both advertise 20% bundle discounts, yet one delivers significantly more savings than the other. An insurer with a $1,200 annual auto premium and a $900 annual homeowner premium (before discounts) gives you roughly $420 in total savings at 20% off. Another insurer with a $1,400 auto premium and a $1,100 homeowner premium at the same 20% discount yields $500 in savings. The percentage stays identical, but your wallet feels the difference.

This reality means you cannot rely on discount percentages alone. You must pull actual quotes from multiple carriers and compare the final bundled premium amounts, not just the discount rates they advertise.

Stacking Additional Discounts for Maximum Savings

Your real savings appear when you layer bundling with other available discounts. Safe driver discounts typically add another 5% to 10%, low-mileage discounts can contribute 5% to 15% depending on your driving habits, and loyalty discounts reward you for staying with an insurer over time. If you combine a 20% bundle discount with a 10% safe driver discount, you reach roughly 28% in total savings rather than 20%.

Many people stop after obtaining a bundled quote without asking about these additional discounts, which means they leave money on the table. When you contact an insurer for quotes, explicitly ask what other discounts apply to your specific situation. Some insurers offer discounts for installing home security systems, completing defensive driving courses, or insuring multiple vehicles, so understanding your full discount picture proves essential before you make a decision.

Finding Your Best Bundle Rate

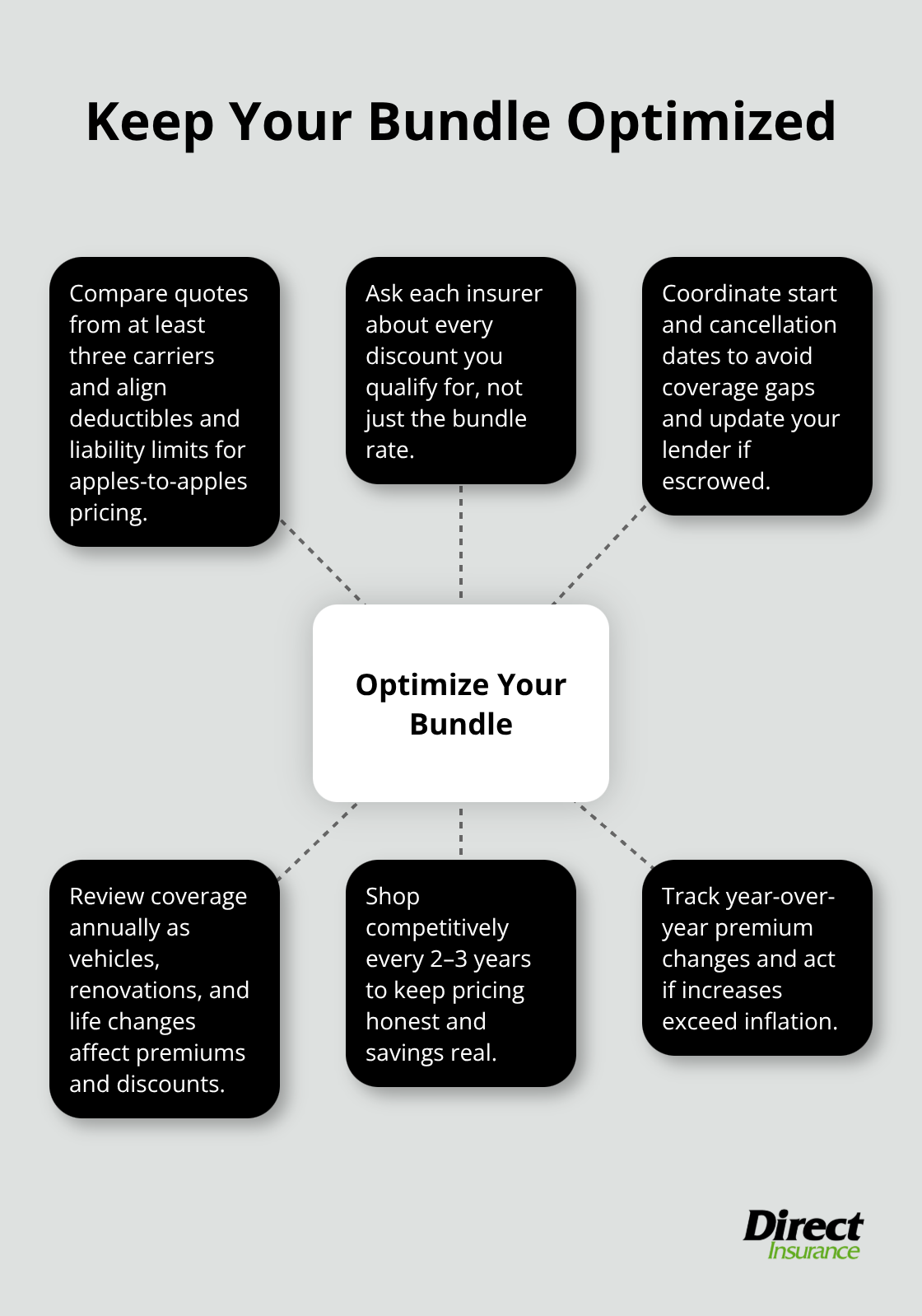

The path forward requires you to request quotes from at least three major carriers and compare the final bundled premiums side by side. Align your coverage limits and deductibles across all quotes so the comparison reflects true apples-to-apples pricing. Ask each insurer about every discount you might qualify for, not just the bundle discount. This approach takes more effort than accepting the first quote you receive, but the difference in your annual premiums often justifies the time investment.

Getting Your Bundle Started and Keeping It Optimized

Request Quotes from Multiple Top Carriers

Start your bundling process by contacting at least three major carriers and requesting quotes for both auto and homeowner coverage together. Specify identical deductibles and liability limits across all quotes so you compare actual equivalent protection. Many people rely solely on online quotes, which often don’t reflect the true bundled rate an agent can negotiate over the phone. According to Bankrate’s 2025 analysis, top carriers for bundling home and auto insurance deserve your attention before you decide.

When you receive quotes, extract the final annual premium amounts after all discounts apply, not just the discount percentages. The insurer with the lowest total bundled premium wins, regardless of how impressive their advertised discount rate sounds.

Execute Your Transition Carefully

Once you’ve chosen your insurer, coordinate the timing with precision. Start both policies with your new company, then cancel your old policies only after the new coverage becomes active. If your home has a mortgage with an escrow account, contact your lender to update the homeowner’s insurance information so they don’t flag a lapse in coverage. This transition typically takes one to two weeks, and rushing it creates unnecessary gaps in your protection.

Monitor Your Coverage Annually

After bundling, review your coverage every year because life changes shift your insurance needs. If you add a second vehicle, that changes your auto premium and potentially unlocks a multi-car discount that stacks on top of your bundle savings. If you renovate your home, your homeowner’s premium may increase, but that renovation might also qualify you for a security system discount that offsets the rise.

Track your premium increases year over year, and if your rate climbs more than inflation justifies, shop around immediately. Bundling creates loyalty, which sometimes makes insurers complacent about your pricing. New customers often receive better rates than existing customers at the same company, so don’t assume staying put saves money.

Shop Competitively Every Few Years

Every two to three years, request fresh quotes from competitors to verify your bundle still delivers real savings compared to what new bundlers receive. Some insurers penalize you for canceling one policy in a bundle by removing the multi-policy discount entirely, so before you drop coverage, ask your agent whether canceling would trigger a rate increase on the remaining policy. This knowledge prevents expensive surprises and helps you make smarter decisions about coverage changes.

Final Thoughts

Bundling your homeowner and auto insurance delivers real financial benefits that most homeowners overlook. A 20% average discount across major carriers translates to hundreds of dollars annually, and when you layer in additional discounts for safe driving or home security, your savings climb even higher. State Farm customers save up to $1,273 per year with bundled coverage, while Allstate offers discounts reaching 25%-these represent actual money staying in your account instead of going to your insurer.

The path to maximizing your savings requires you to compare quotes from multiple carriers rather than accepting the first offer you receive. Request bundled quotes from at least three insurers with identical deductibles and coverage limits, then extract the final annual premium amounts to identify your true winner. Many people overlook additional discounts stacked on top of bundling (safe driver discounts, loyalty bonuses, low-mileage rates, and security system discounts), which means they leave 5% to 15% in savings on the table.

Contact Direct Insurance Services to start your homeowner and auto insurance bundle search today. Our independent agency based in Salt Lake City shops multiple top-rated insurers to find you the best bundled rates for your situation. Within weeks, you’ll have your coverage in place, delivering savings that compound year after year.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation