How to Get the Best Home Insurance Rates

Home insurance premiums vary dramatically across the country, with some homeowners paying three times more than others for similar coverage. The difference often comes down to knowing which factors insurers prioritize and how to leverage them.

We at Direct Insurance Services have helped thousands of homeowners secure the best home insurance rates by focusing on proven strategies that actually work. Smart shopping and strategic policy adjustments can save you hundreds of dollars annually.

What Drives Your Home Insurance Costs

Location and Natural Disaster Risk

Your location determines up to 70% of your home insurance premium and stands as the single most powerful factor in rate calculations. Homes in hurricane-prone Florida average $4,231 annually according to Insurance Information Institute data, while Wyoming homeowners pay just $1,285 for similar coverage.

Wildfire zones in California and Colorado face premium increases of 20-40% above state averages. Proximity to fire departments and hydrants can reduce rates by 5-10%, while homes within 1,000 feet of coastlines or flood zones see automatic surcharges that insurers apply without negotiation.

Construction Materials and Home Age

Construction materials and home age create significant rate variations that homeowners encounter. Brick homes receive 5-15% discounts compared to wood frame construction, while homes built before 1980 face premium penalties of 10-25% due to outdated electrical and plumbing systems.

Steel and concrete construction in tornado-prone areas can slash premiums by up to 35%. These materials resist wind damage better than traditional wood frame construction (which explains why insurers reward homeowners who invest in stronger building materials).

Coverage Limits and Deductible Selection

Your coverage limit directly impacts costs in predictable ways. Insurers charge roughly $200-300 more annually when you insure a home for $400,000 versus $300,000. This linear relationship makes coverage decisions straightforward for most homeowners.

Deductible selection offers immediate savings that you control completely. Homeowners who raise their deductible from $1,000 to $2,500 typically reduce premiums by 12-18%, while those who jump to $5,000 can cut costs by 25-30%. Most homeowners choose $1,000 deductibles, but financial experts recommend higher amounts if you maintain adequate emergency savings (typically 3-6 months of expenses).

These cost factors work together to create your final premium, but smart homeowners can influence several of them through strategic choices and home improvements. Consider bundling auto and home insurance to unlock additional savings of 5-25% on your total premiums.

How Can You Slash Your Home Insurance Costs

Multi-Policy Bundling Delivers Guaranteed Savings

Bundling your home and auto insurance with the same carrier generates automatic discounts of 5-25% on your total premiums. State Farm customers can save up to $1,356 when bundling auto and home insurance, while Allstate customers save approximately $692 per year through their multi-policy discount program.

The math works because insurers prefer customers who consolidate their business. They reduce marketing costs and increase customer retention when you hold multiple policies. Progressive offers up to 12% off home insurance when combined with auto coverage, and USAA provides military families with discounts that reach 23% in some states.

Security Upgrades Cut Premiums Immediately

Monitored security systems reduce home insurance premiums by 5-20% depending on your insurer and system type. ADT and SimpliSafe installations qualify for discounts with most major carriers, while smart home devices like Ring doorbells and Nest smoke detectors can lower rates by an additional 2-5%.

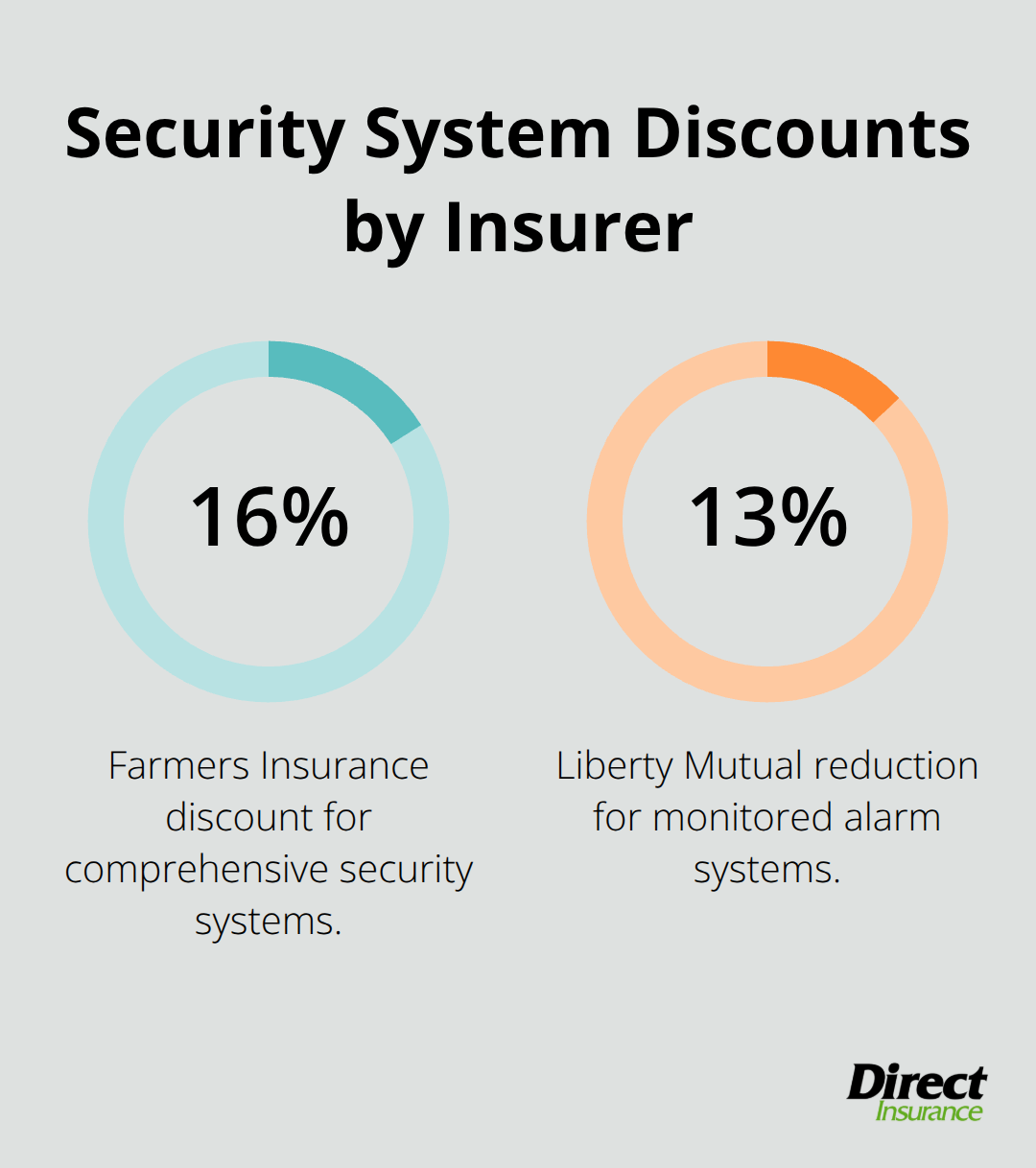

Deadbolt locks, security cameras, and fire extinguishers generate smaller but meaningful discounts of 2-10%. These upgrades pay for themselves within 2-3 years through premium savings alone. Farmers Insurance offers 16% discounts for comprehensive security systems, while Liberty Mutual provides 13% reductions for monitored alarm systems.

Rate Shopping Reveals Hidden Savings

Home insurance rates vary by 40-60% between carriers for identical coverage, which makes comparison shopping the most powerful tool for cost reduction. GEICO quotes averaged $1,247 annually for $300,000 coverage according to NerdWallet analysis, while Travelers averaged $2,102 for the same protection.

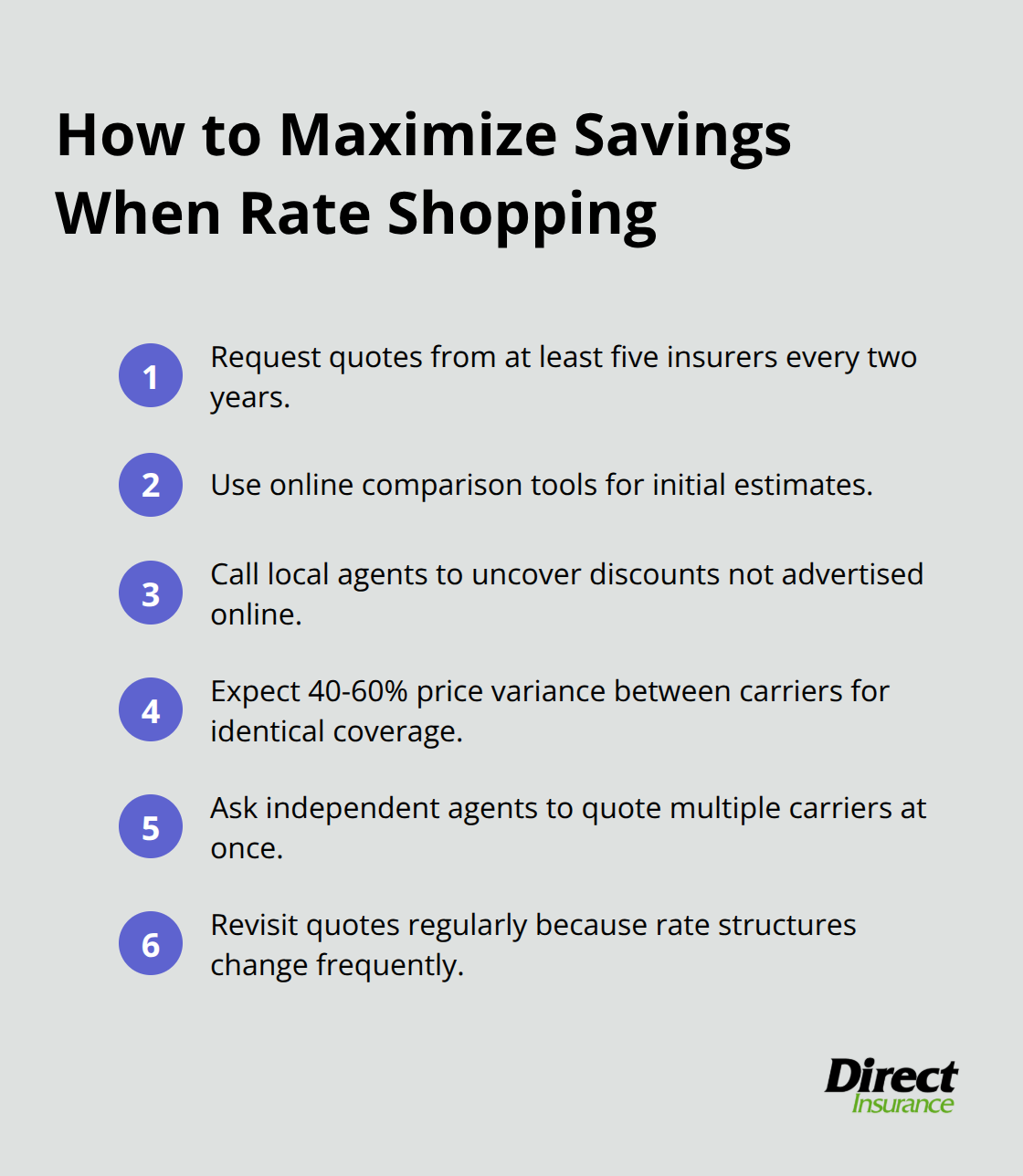

Request quotes from at least five insurers every two years because rate structures change frequently. Online comparison tools provide initial estimates, but direct contact with local agents often reveals additional discounts not advertised online (independent agents can quote multiple carriers simultaneously and save you time while they maximize your savings potential).

However, even the smartest shoppers make costly mistakes that can wipe out these savings completely. The next section reveals the three most expensive errors homeowners make when they purchase insurance.

What Insurance Mistakes Cost You Money

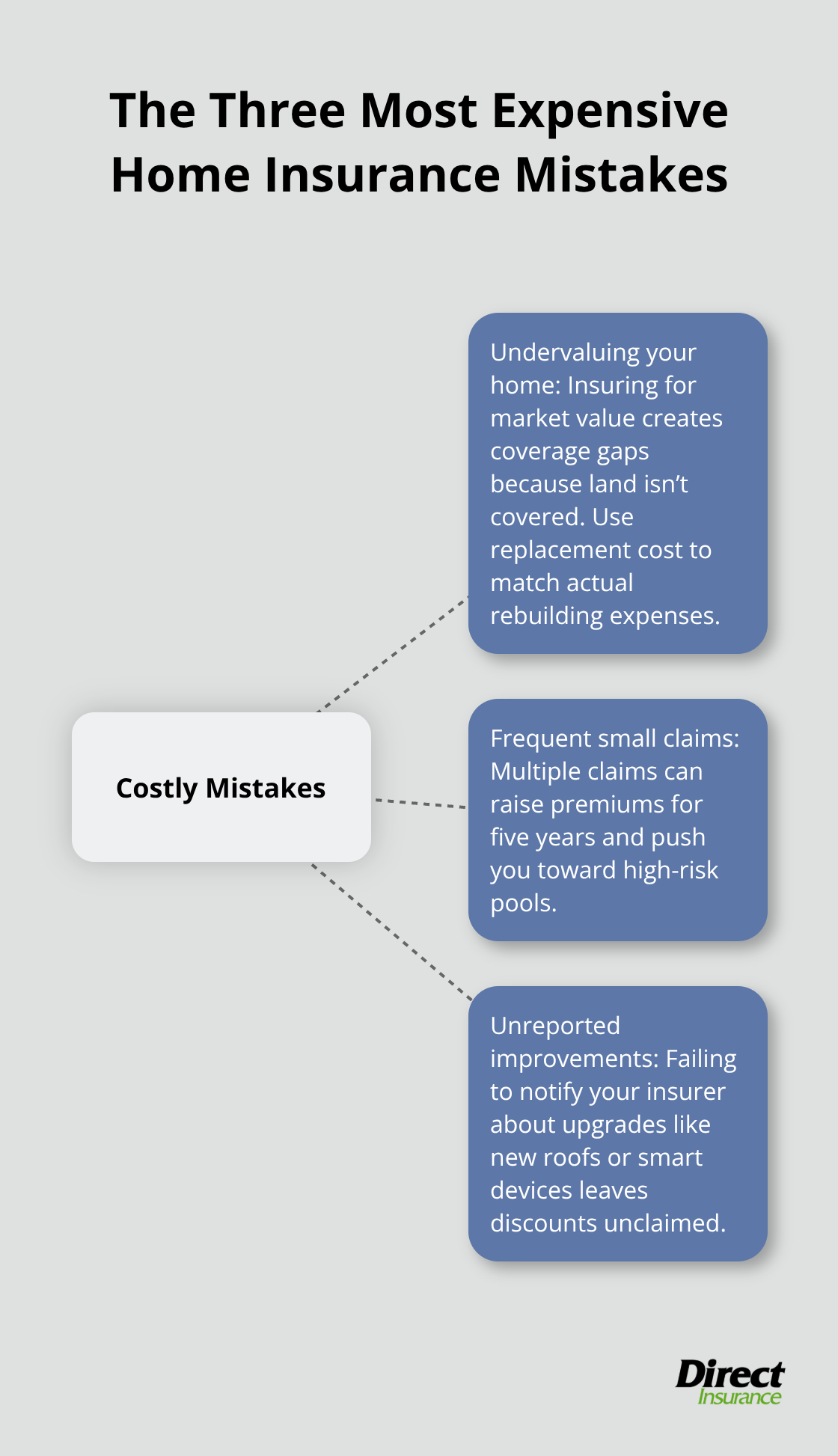

Undervaluing Your Home Creates Coverage Gaps

Most homeowners insure their property for market value instead of replacement cost, which creates dangerous coverage shortfalls that surface during claims. Market value includes land costs that insurers never cover, while replacement cost reflects actual rebuilding expenses. A $400,000 home might require $320,000 to rebuild, but homeowners often insure for the full purchase price and pay higher premiums for unnecessary coverage.

Construction costs have surged significantly in recent years, yet many homeowners never adjust their coverage limits. This gap means your coverage from previous years now provides less purchasing power. Insurance companies require 80% replacement cost coverage to avoid coinsurance penalties (where they reduce claim payments proportionally to your underinsurance).

Frequent Small Claims Destroy Your Rates

Multiple small claims trigger rate increases that last five years and cost far more than the original damage. A single claim raises premiums significantly on average, while two claims within three years can substantially increase your rates. Homeowners who file small roof claims often pay thousands extra in premiums over the next five years.

Insurance companies track your claims through CLUE reports that follow you between carriers. Multiple claims in five years make you nearly uninsurable with standard carriers (which forces you into high-risk pools with premiums well above market rates). Smart homeowners handle smaller repairs out of pocket and reserve insurance for catastrophic losses that exceed their financial capacity.

Home Improvements Go Unreported

Home improvements like new roofs, updated electrical systems, or security upgrades can reduce premiums, but insurers never automatically adjust your rates. You must contact your agent and provide documentation to claim these discounts. A roof replacement typically generates annual savings, yet most homeowners never notify their insurance company.

Smart home technology installations qualify for additional discounts that stack with security system reductions. Nest thermostats, water leak detectors, and smart smoke alarms can combine for premium reductions when you properly document them with your insurer.

Final Thoughts

The best home insurance rates require a systematic approach that combines smart comparison shopping with strategic policy management. Request quotes from at least five insurers every two years, as rates vary by 40-60% between carriers for identical coverage. Bundle your home and auto policies to unlock automatic savings of 5-25%, and invest in security upgrades that generate immediate premium reductions.

Avoid the costly mistakes that drain your savings over time. Never file small claims that cost less than your annual premium increase, and always insure for replacement cost rather than market value. Update your policy after home improvements to capture available discounts that insurers never apply automatically (most homeowners miss thousands in potential savings this way).

We at Direct Insurance Services help homeowners navigate these complexities and shop multiple top-rated carriers to find optimal coverage at competitive rates. Smart insurance choices deliver compound benefits over time, as the hundreds you save annually add up to thousands over your homeownership. Contact Direct Insurance Services today to start maximizing your home insurance value.