Best Home Insurance Prices for Your Budget

Finding the best home insurance prices doesn’t have to drain your budget. Smart homeowners save hundreds annually by understanding what drives premium costs.

We at Direct Insurance Services see clients reduce their rates by 20-30% using proven strategies. The right approach combines comparing quotes with optimizing your coverage profile.

What Actually Drives Your Home Insurance Costs

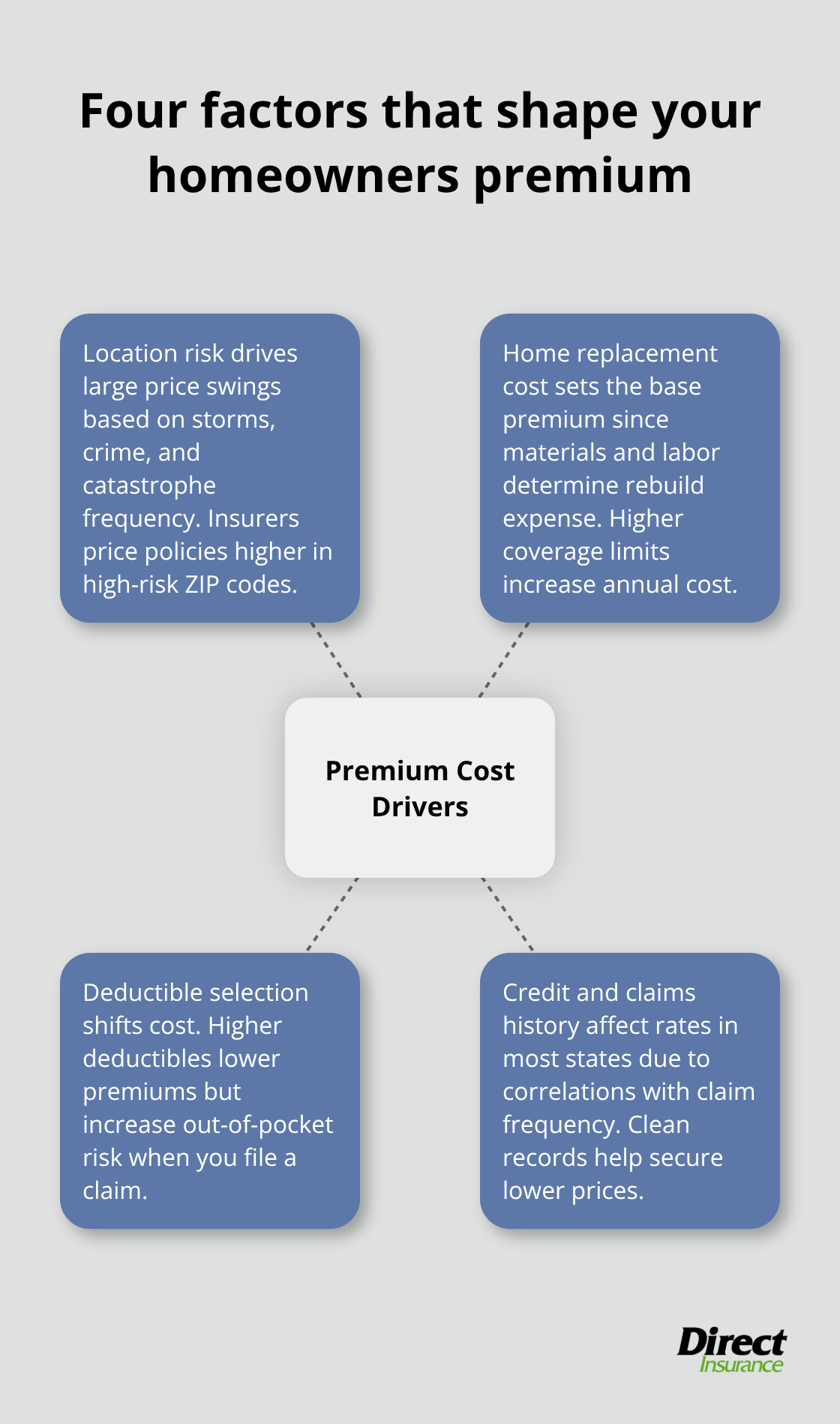

Location Determines Your Premium Reality

Your location alone can make or break your premium budget. Oklahoma homeowners pay an average of $4,623 annually while Alaska residents pay just $942 for identical coverage, according to Quadrant Information Services data. This massive 400% difference stems from weather patterns, crime rates, and natural disaster frequency.

States like Texas and Nebraska follow Oklahoma with premiums that exceed $4,500 due to severe weather exposure. Hurricane zones, earthquake regions, and wildfire areas automatically trigger higher rates regardless of your home’s condition. Insurance companies analyze regional risk data and adjust premiums accordingly.

Home Value Creates Your Premium Foundation

Your home’s replacement cost directly controls your base premium. A $200,000 coverage limit averages $1,555 annually, while $500,000 coverage jumps to $3,210 per year. Insurance companies calculate replacement costs with current construction materials and local labor rates (not your purchase price).

Newer homes consistently receive lower premiums because updated electrical systems, plumbing, and roofing reduce claim risks. Homes built before 1980 face premium penalties that average 15-25% higher due to outdated codes and infrastructure that ages over time.

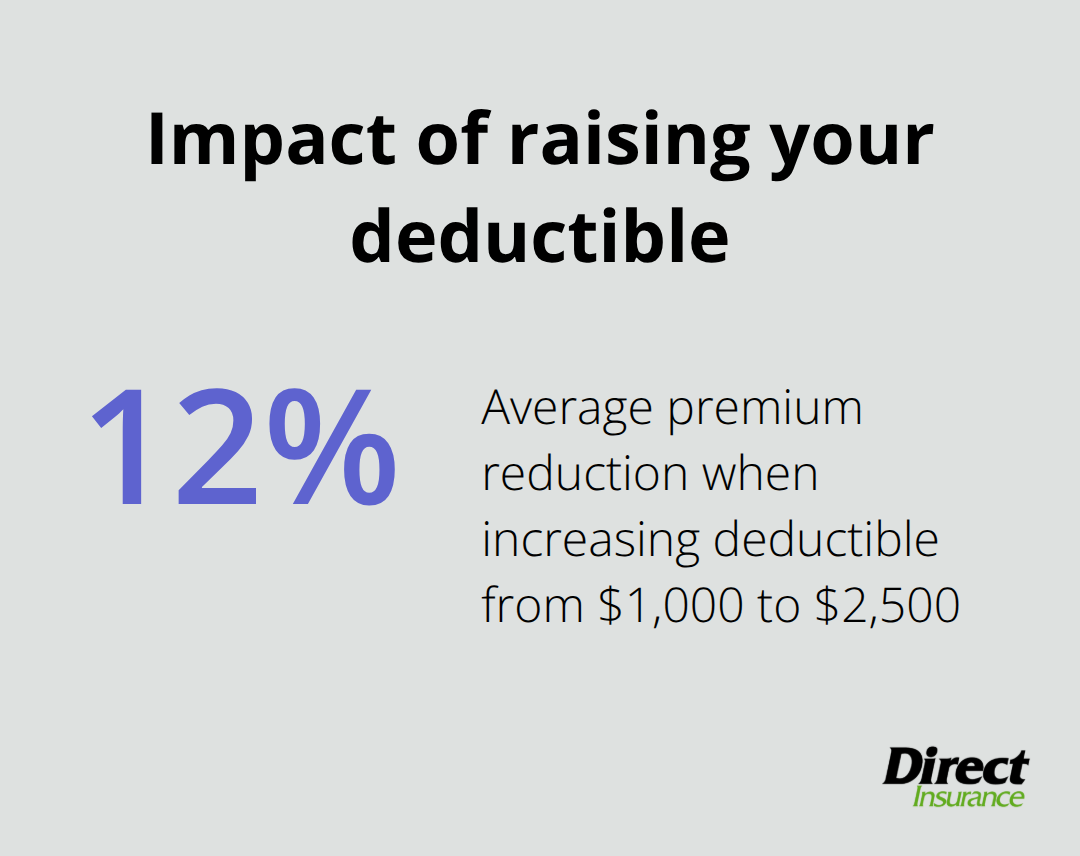

Deductible Choices Control Your Monthly Payment

You can reduce premiums by approximately 12% when you raise your deductible from $1,000 to $2,500 according to industry analysis. This strategy works best when you maintain emergency savings equal to your deductible amount.

Credit Score Creates Dramatic Premium Swings

Credit scores create dramatic premium variations with poor credit homeowners who pay $3,620 annually versus $2,210 for excellent credit holders. Claims history impacts future premiums with homeowners insurance claims staying on your CLUE report for five to seven years.

These cost factors work together to create your final premium, but smart homeowners can take specific actions to reduce these expenses through strategic policy management.

How Can You Cut Your Home Insurance Costs

Multi-Policy Bundling Delivers Immediate Savings

Bundle home and auto insurance to generate savings of 10-25% on your total premiums according to industry data. USAA leads with the most aggressive discounts, while State Farm and Allstate also provide substantial multi-policy reductions. The savings compound when you add additional policies like umbrella coverage or motorcycle insurance to your bundle.

Insurance companies reward customers who bundle because it reduces their acquisition costs and increases retention rates. Most carriers require you to maintain both policies with them to keep the discount, so compare the bundled rate against separate policies from different companies. Some homeowners save more by choosing the cheapest individual policies from different carriers rather than one company’s bundle.

Security Upgrades Reduce Risk and Premiums

Install monitored security systems, smart smoke detectors, and deadbolt locks to reduce your premiums by 5-20% depending on your carrier. Travelers offers specific discounts for certified smart home devices, while Farmers provides extensive security-related reductions. Video doorbells, motion sensors, and professionally monitored alarm systems generate the highest discounts because they prevent both theft and enable early fire detection.

Water leak detection systems and automatic shut-off valves can qualify for additional discounts since wind and hail account for the largest share of homeowners insurance claims, with 2.8 percent of insured homes experiencing such losses, followed by water damage and freezing at 1.5 percent. Newer homes with updated electrical panels, HVAC systems, and roofing materials automatically receive lower rates due to reduced fire and structural risks.

Credit Management Creates Long-Term Premium Control

Maintain excellent credit to save an average of $1,410 annually compared to poor credit scores based on Quadrant Information Services analysis. Insurance companies use credit-based insurance scores in most states because statistical data shows strong correlation between credit management and claim frequency. Pay bills on time, maintain low credit utilization, and avoid new debt inquiries to directly impact your insurance rates.

Homeowners with clean claims histories pay baseline premiums while previous claims increase rates by $125-145 annually for five to seven years. File multiple claims or high-dollar claims and you risk non-renewal, which makes prevention and maintenance investments more valuable than insurance payouts for minor damages.

These cost-reduction strategies work best when you combine them with smart quote comparison techniques that reveal the true value differences between insurance providers. General liability insurance protects against bodily injury and property damage claims that could otherwise devastate your finances.

How Do You Compare Insurance Quotes Without Getting Fooled

Request at least three quotes from different insurance companies to compare options effectively. The National Association of Insurance Commissioners produces comprehensive homeowners insurance reports with market data and cost analysis. This comparison requires strategic evaluation beyond simple premium numbers. Travelers offers the cheapest widely available coverage at $2,055 annually, while American Family averages $2,745 for identical protection levels. These premium differences reflect different risk assessments, discount structures, and claims processes that directly impact your long-term costs.

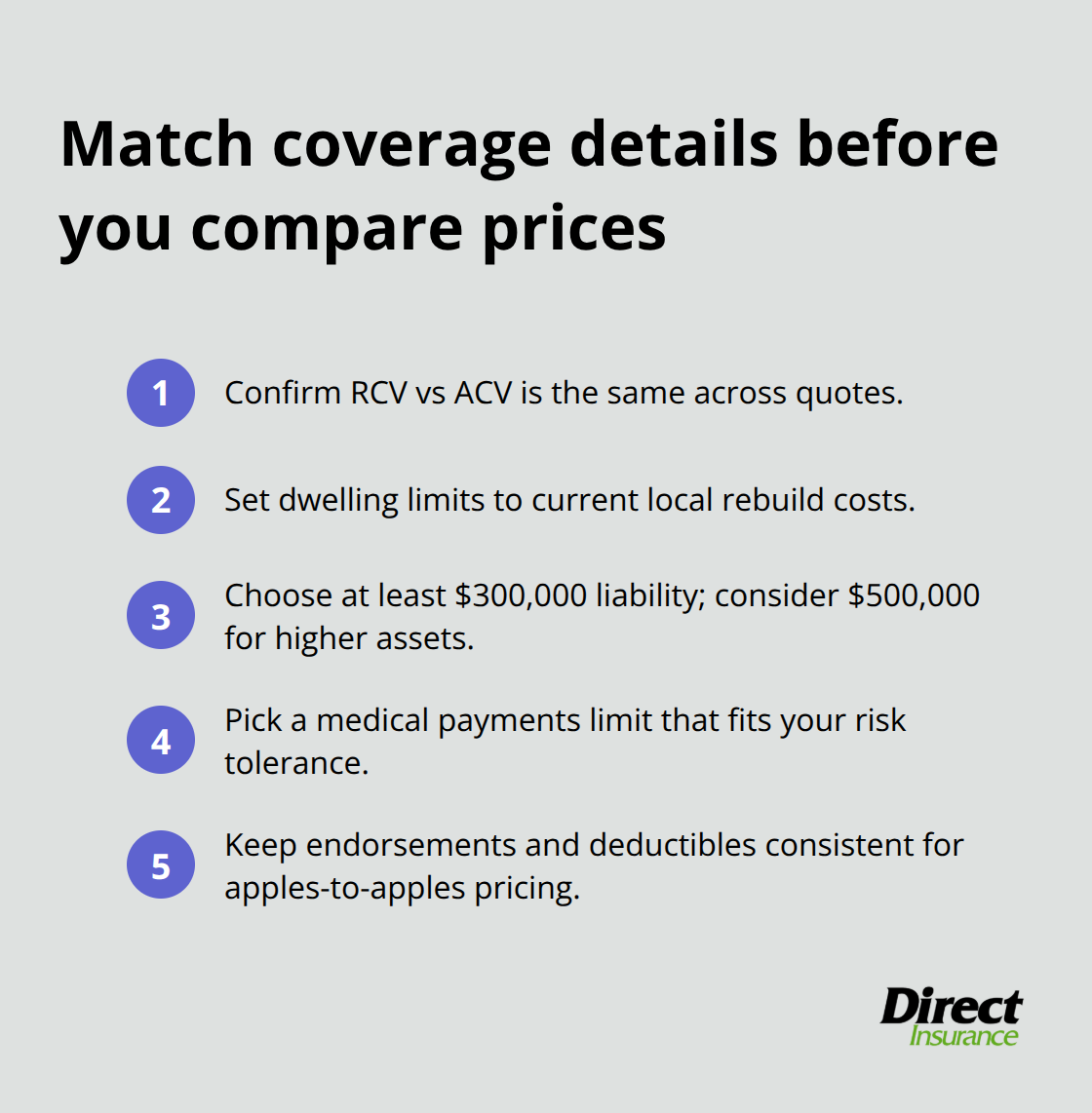

Match Coverage Details Before You Compare Prices

Insurance companies create misleading price comparisons through coverage variations. Replacement Cost Value coverage costs more than Actual Cash Value but prevents devastating underinsurance when you file claims. Dwelling coverage limits must reflect current construction costs, not your home’s purchase price or tax assessment value.

Personal liability coverage should start at $300,000 minimum with $500,000 recommended for homeowners with assets that exceed their home value. Medical payments coverage varies from $1,000 to $10,000 with higher limits that cost minimal additional premium but provide substantial protection against guest injury lawsuits.

Research Claims Processing Speed and Customer Satisfaction

Amica receives the highest customer satisfaction ratings while it maintains the cheapest average premiums at $97 monthly according to U.S. News analysis. State Farm processes the most claims annually but customer service quality varies significantly by local office and agent experience. USAA provides exceptional service exclusively for military families with average premiums of $130 monthly. Claims processing speed matters more than premium savings when you face emergency repairs or temporary housing needs (especially after major disasters). Research J.D. Power ratings, state insurance department complaints, and online reviews to identify companies that delay payments or deny legitimate claims through excessive documentation requirements.

Evaluate Agent Support and Local Expertise

Independent agents like those at Direct Insurance Services shop multiple top-rated insurance companies to find the best coverage at competitive rates. Local agents understand regional risks better than national call centers and can explain coverage options that match your specific situation. They provide personalized service and build long-term relationships rather than treat you as a policy number. Agent availability during claims matters significantly when you need immediate assistance (particularly during Utah’s severe weather events). Compare agent response times, local office hours, and their ability to handle complex coverage questions before you make your final decision.

Final Thoughts

The best home insurance prices come from thorough comparison shopping combined with strategic coverage decisions. Request quotes from at least three companies with identical coverage limits to make accurate price comparisons. Travelers averages $2,055 annually while American Family costs $2,745 for the same protection, which proves that research delivers real savings.

Local insurance experts provide advantages that online quotes cannot match. We at Direct Insurance Services shop multiple top-rated companies to find competitive rates while we understand regional risks like Utah’s severe weather patterns. Local agents provide personalized service during claims and build relationships that extend beyond policy sales.

Proper coverage selection creates long-term financial protection that justifies premium investments. Adequate dwelling coverage prevents devastating underinsurance while liability limits protect your assets from lawsuit exposure (the average homeowner saves $350 annually through quote comparison). Quality coverage from reputable companies with strong claims processing protects your most valuable asset and provides peace of mind that cheap policies cannot deliver.