Personal Umbrella Insurance in Utah Do You Need It?

Utah residents face unique liability risks that standard insurance policies often can’t handle. Personal umbrella insurance in Utah provides extra protection when lawsuits exceed your regular coverage limits.

We at Direct Insurance Services see many Utah homeowners surprised by how affordable this additional coverage can be. The question isn’t whether you can afford umbrella insurance-it’s whether you can afford to go without it.

What Personal Umbrella Insurance Covers in Utah

Liability Protection Beyond Standard Policy Limits

Your standard homeowners policy in Utah typically covers liability up to $300,000, while auto policies max out around $500,000. When a Park City accident results in $1.2 million in medical bills, or your teenage driver causes a multi-car collision with $800,000 in damages, these limits fall short. Personal umbrella insurance steps in to cover the gap and provides an additional $1 million to $5 million in protection. The Insurance Information Institute reports that 0.77 percent of people with liability insurance had a bodily injury liability claim in 2023, which leaves them financially exposed when standard policies reach their limits.

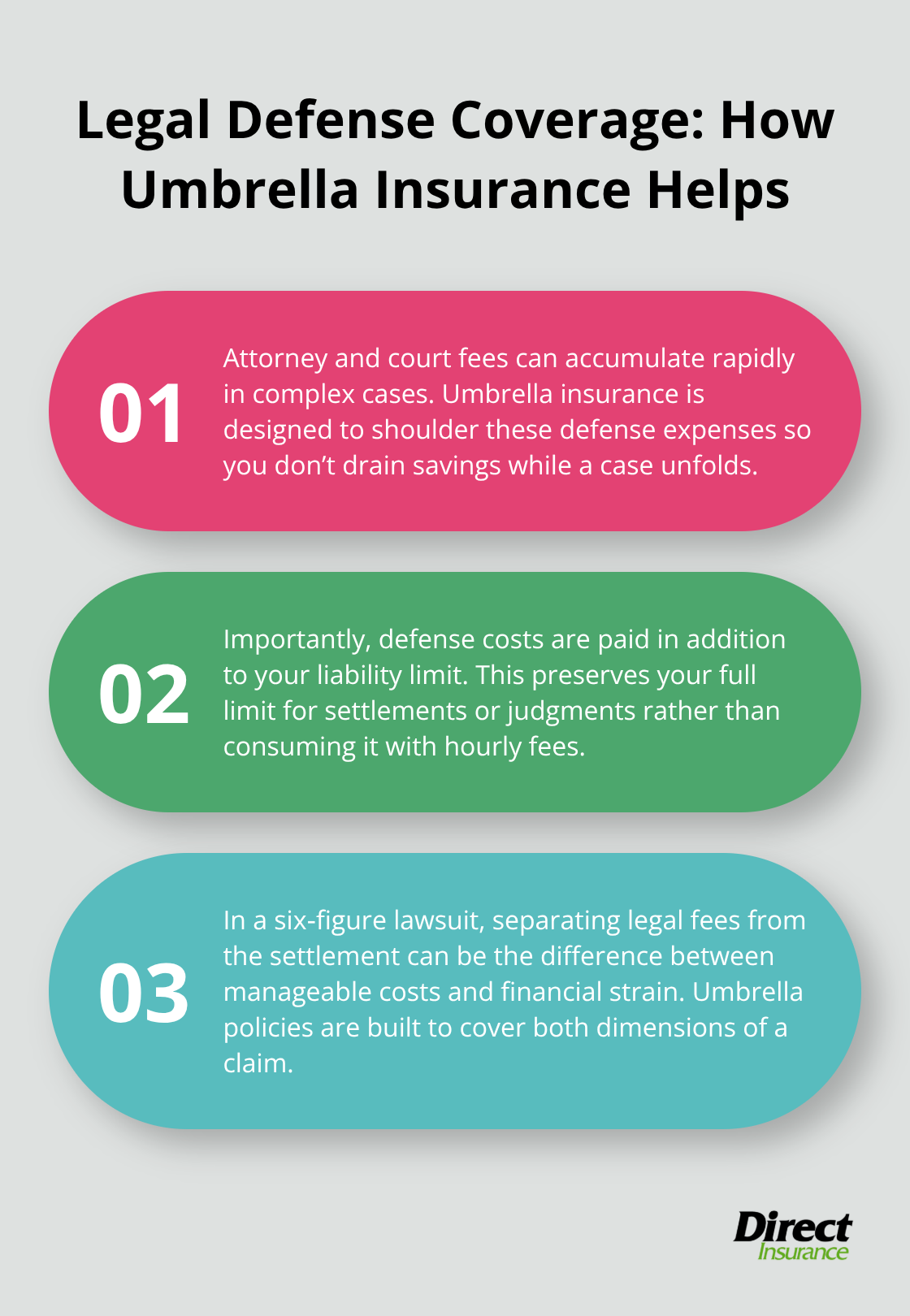

Coverage for Legal Defense Costs and Settlements

Court costs and attorney fees can devastate your finances even before any settlement occurs. Legal fees in Utah range from $200 to $1,000 per hour according to the U.S. Bureau of Labor Statistics, and complex liability cases often require months of litigation. Umbrella policies cover these defense costs in addition to your coverage limits (not as part of them).

This means if you face a $500,000 lawsuit, your umbrella insurance pays both the settlement and the $150,000 in legal fees separately.

Protection Against Utah-Specific Risks

Utah’s outdoor recreation culture creates unique liability exposures that standard policies often exclude. Water recreation incidents contribute significantly to homeowner liability claims according to the National Safety Council, particularly relevant for Utah residents with hot tubs or pools. The state’s high uninsured driver rate of 8.5% increases your risk of underinsured motorist claims. Umbrella insurance also covers liability from recreational vehicles, boats, and off-road equipment popular in Utah, plus rental property exposures for those with vacation homes in ski areas or national park regions.

These coverage areas become particularly important when you consider who actually needs this protection and when the investment makes financial sense.

When Utah Residents Should Consider Umbrella Insurance

High Net Worth Individuals and Asset Protection

Utah residents with significant assets face the greatest risk from liability lawsuits. The Insurance Information Institute states that nearly 40 percent of Americans lack sufficient liability coverage to protect their assets, which leaves them vulnerable to financial devastation. Creditors can seize your home, retirement accounts, and future earnings to satisfy debt when you face a $1.2 million judgment but own property worth $800,000. Your standard homeowner policy covers only $300,000 and exposes you to $900,000 in personal liability.

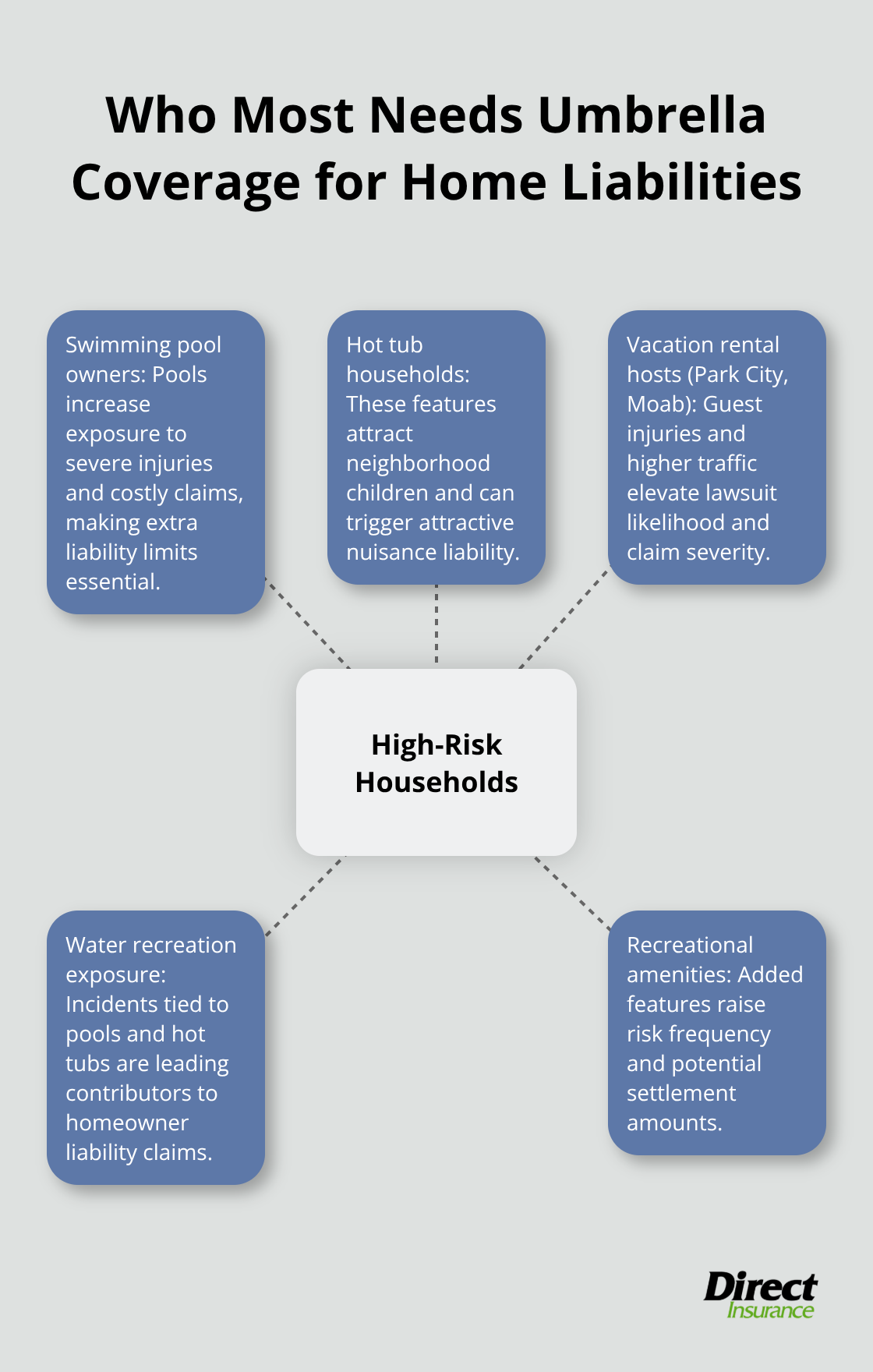

Homeowners with Swimming Pools or Recreational Properties

Swimming pool owners face dramatically increased liability exposure, with incidents that result in settlements. Utah homeowners with hot tubs encounter similar risks, as these features attract neighborhood children and create attractive nuisance liability. Vacation rental owners in Park City or Moab face even higher exposure with guest injuries that frequently result in lawsuits.

The National Safety Council reports that water recreation incidents rank among the top contributors to homeowner liability claims nationwide.

Business Owners and Professional Service Providers

Utah business owners who operate from home offices need umbrella coverage because standard homeowner policies exclude business activities. Real estate agents, consultants, and healthcare professionals face professional liability claims. Small business owners with teenage employees face elevated risks, as teen workers have accident rates three times higher than adult employees. Professional service providers who meet clients at their homes or maintain public profiles through social media face additional defamation and personal injury exposures that standard policies won’t cover.

These risk factors directly impact how much you’ll pay for umbrella coverage and what discounts you might qualify for in Utah’s competitive insurance market.

Cost Analysis of Umbrella Insurance in Utah

Average Premium Costs Deliver Outstanding Value

Utah residents pay between $150 to $300 annually for $1 million in personal umbrella coverage, which makes it one of the most cost-effective insurance investments available. ACE Private Risk Services data shows the national average for $1 million umbrella coverage runs $383 per year, so Utah residents enjoy below-average rates. Each additional $1 million in coverage costs approximately $75 more annually, which means $2 million in protection typically runs $225 to $375 per year. When you consider that a single serious accident can generate $1.2 million in medical bills and legal costs, you pay $200 annually for protection that represents exceptional value.

Risk Exposure Factors Determine Your Premium

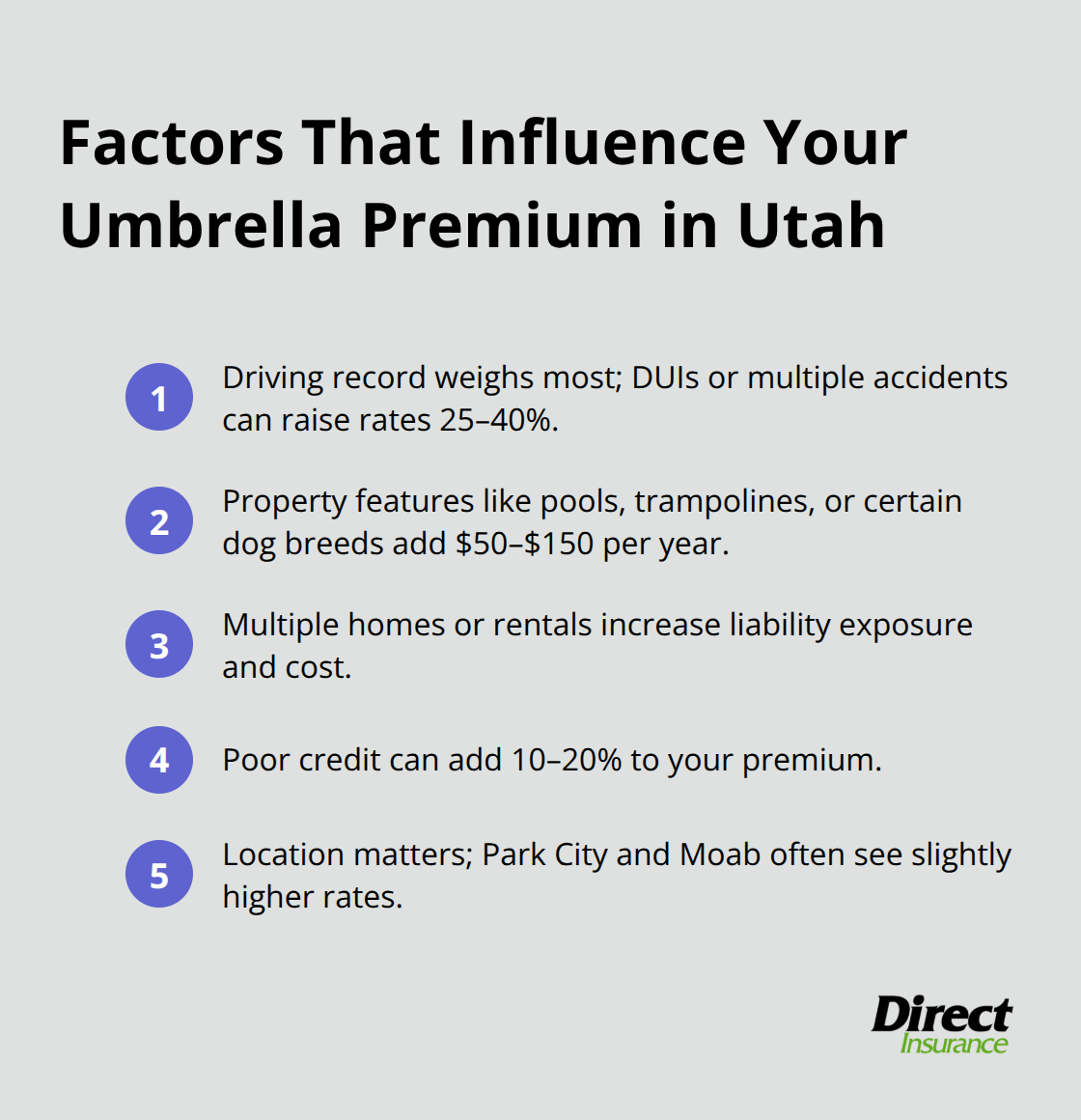

Insurance companies calculate your umbrella rates based on specific risk factors that directly impact your liability exposure. Your motor vehicle history carries the most weight, with DUI convictions or multiple accidents that increase premiums by 25 to 40 percent. Property features like pools, trampolines, or aggressive dog breeds add $50 to $150 annually to your premium.

Multiple homes or rental properties increase costs because each property creates additional liability exposure. Your credit score also affects rates (with poor credit that adds 10 to 20 percent to your premium). Location matters too, with Park City and Moab residents who pay slightly higher rates due to increased recreational activity risks.

Bundle Discounts Cut Your Total Insurance Costs

Utah insurers offer substantial discounts when you bundle umbrella insurance with current policies, which typically reduces your total premium by 5 to 15 percent. Most carriers require minimum liability limits on your underlying policies before they issue umbrella coverage, usually $300,000 for homeowners and $250,000/$500,000 for auto insurance. You need to shop multiple carriers because umbrella rates vary significantly between companies (with some insurers that offer 30 percent lower rates than competitors for identical coverage). Try to obtain quotes from at least three top-rated carriers to secure optimal rates for your specific risk profile.

Final Thoughts

Personal umbrella insurance Utah residents need depends on their specific risk profile and asset exposure. Utah’s outdoor recreation culture, high uninsured driver rates, and vacation rental properties create liability risks that standard policies can’t handle. The math is straightforward: you pay $200 annually for $1 million in protection when a single accident can generate $1.2 million in damages.

The key benefits justify the investment for most Utah homeowners. Legal defense costs alone can reach $150,000 before any settlement occurs (and that’s separate from the actual judgment). Pool owners, business operators, and high net worth individuals face the greatest exposure, but even modest asset holders benefit from protection against wage garnishment and future earnings seizure.

You need coverage that starts with an evaluation of your current liability limits and identification of coverage gaps. We at Direct Insurance Services help you determine appropriate coverage levels for your specific situation. Contact us today to protect your financial future with affordable umbrella coverage that fits your budget and risk profile.