Vacation Rental Insurance Options in Utah

Utah’s vacation rental market generated over $400 million in revenue during 2024, making proper insurance protection more important than ever for property owners.

Standard homeowners policies typically exclude short-term rental activities, leaving owners exposed to significant financial risks. We at Direct Insurance Services see many Utah property owners operating without adequate vacation rental insurance Utah coverage, putting their investments at serious risk.

What Insurance Coverage Do Vacation Rentals Actually Need?

Vacation rental owners require three distinct coverage types that standard homeowners policies simply don’t provide. Property protection coverage must include replacement cost coverage for buildings and contents, with special cause of loss protection that covers guest-caused damage beyond normal wear and tear. Standard policies may help pay for repairs from incidents like pipe bursts causing water damage, but rental-related damages require specialized vacation rental insurance coverage. Property coverage must extend to furnishings, electronics, and decorative items that guests might damage or steal, with coverage limits that reflect actual replacement costs rather than depreciated values.

Guest Liability Protection Requirements

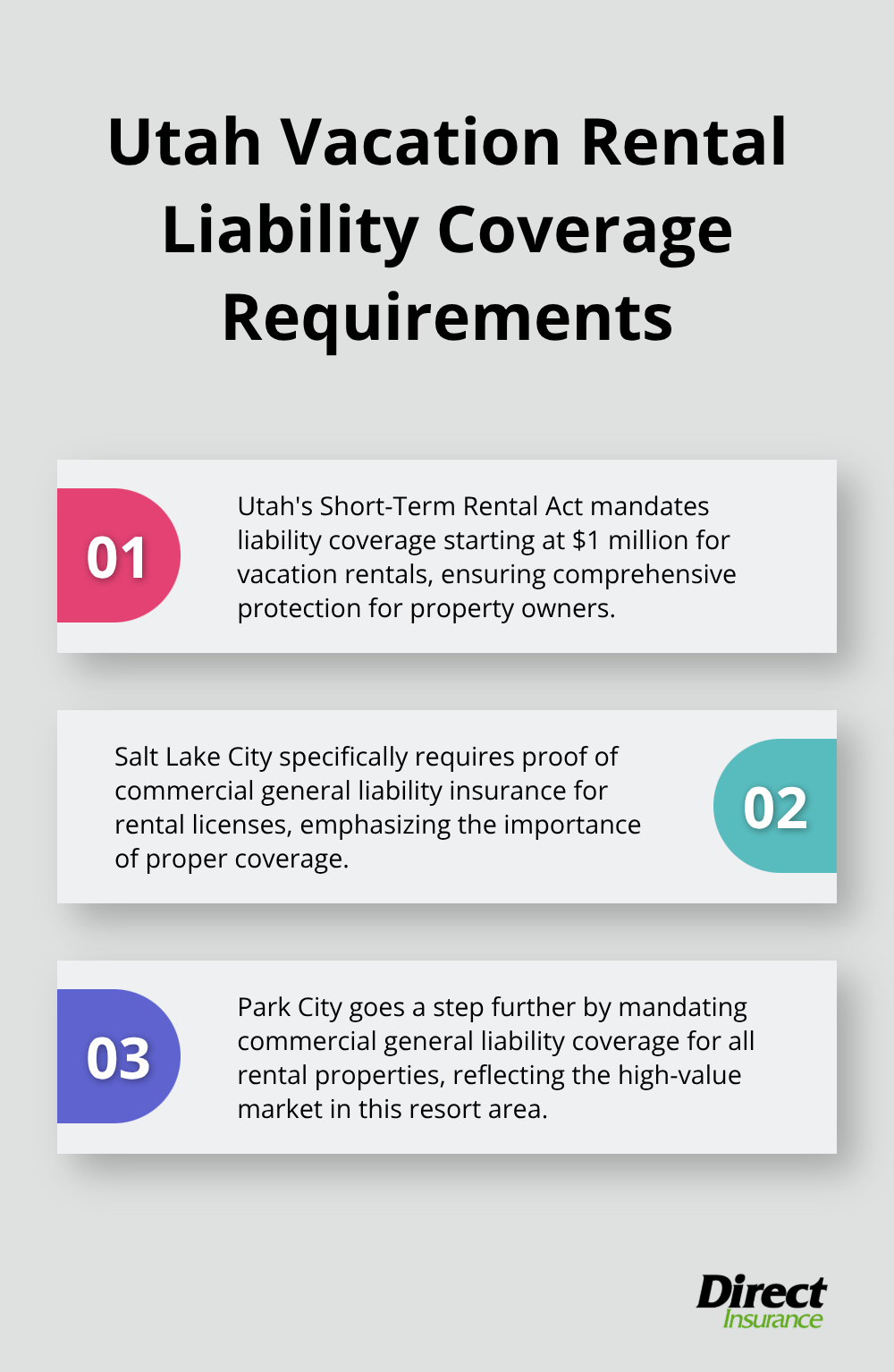

Liability coverage starts at $1 million for Utah vacation rentals, as mandated by the state’s Short-Term Rental Act. Salt Lake City requires proof of commercial general liability insurance for rental licenses, while Park City specifically mandates this coverage type for all rental properties. Guest injuries from slip-and-fall accidents can result in substantial claims, which makes robust liability protection essential. Coverage should include liquor liability for properties where alcohol consumption occurs, plus amenity liability for pools, hot tubs, or recreational equipment. Pet liability without breed restrictions protects owners who allow animals (a feature that addresses gaps standard policies often exclude).

Income Protection During Property Repairs

Lost rental income protection compensates owners when properties become unrentable due to covered damage. Utah’s vacation rental market experiences peak seasons where daily rates can exceed $300 in areas like Park City and Moab, which makes income interruption particularly costly. Business interruption coverage should include no time limits on claims and protection for canceled reservations when damage occurs before guest arrivals. Revenue protection becomes more valuable as Utah’s short-term rental market continues to grow, with hosts earning significant income from their properties.

Specialized Coverage for Unique Rental Risks

Standard policies fail to address specific vacation rental exposures that can result in substantial financial losses. Squatter protection covers legal costs when guests refuse to vacate properties after their stay expires (particularly important for longer bookings). Pest protection shields owners from extermination costs and revenue losses when bed bugs or other infestations force property closures. These specialized coverages address real risks that traditional homeowners insurance completely ignores, leaving property owners vulnerable to unexpected expenses that can quickly escalate into thousands of dollars.

The next consideration involves understanding how various factors influence your insurance premiums and coverage costs across different Utah markets.

What Drives Your Utah Vacation Rental Insurance Costs

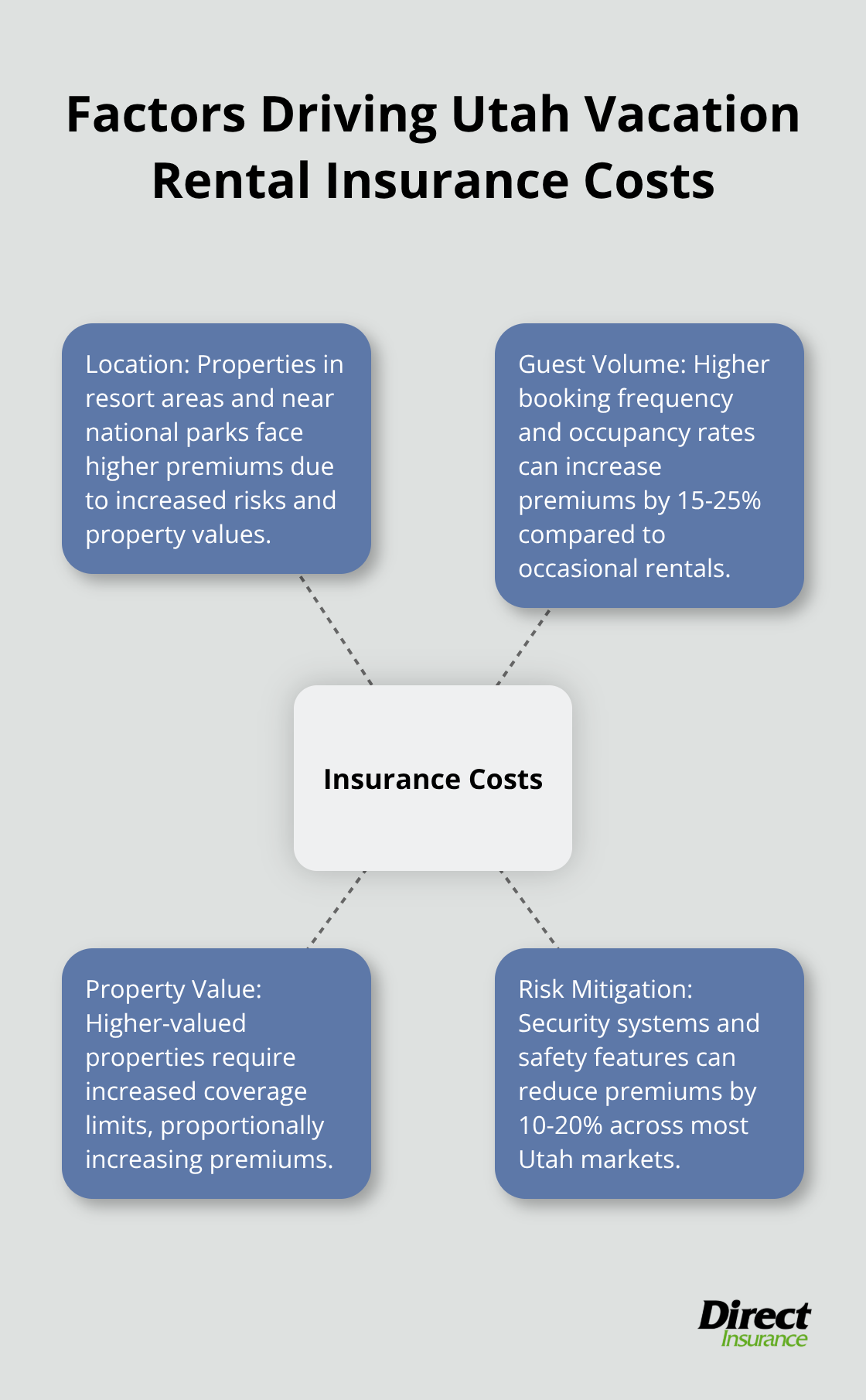

Insurance premiums for Utah vacation rentals vary dramatically based on location, with properties in resort areas paying significantly more than rural areas due to higher property values and increased liability risks. Mountain resort locations face elevated premiums because of weather-related claims, while properties near national parks like Moab command higher rates due to increased guest activity and potential for accidents. Salt Lake City vacation rentals typically fall in the middle range, with annual premiums between $800-$1,500, while luxury Park City properties can exceed $2,500 annually. Properties in flood-prone areas or wildfire zones face additional surcharges that can increase base premiums by 25-35%.

Guest Volume Directly Impacts Premium Calculations

Insurance companies analyze your booking frequency and occupancy rates when they calculate premiums, with properties rented more than 180 days annually facing commercial-level pricing. High-turnover properties with frequent guest changes present greater liability exposure, which results in premium increases of 15-25% compared to occasional rental properties. Properties that accommodate large groups or events face the highest rates, as insurers view these as elevated risk scenarios. Seasonal rentals that operate only during ski season or summer months may qualify for reduced premiums, though coverage gaps during off-seasons can create problems if incidents occur.

Property Value and Coverage Selections Drive Final Costs

Coverage limits significantly impact premium costs, with $2 million liability coverage costing approximately 40% more than the state-mandated $1 million minimum. Properties valued above $500,000 require higher dwelling coverage limits, which increases premiums proportionally to replacement cost estimates. Property owners who choose actual cash value over replacement cost coverage can reduce premiums by 20-30%, but this leaves them vulnerable to depreciation gaps during claims. Deductible selections also affect costs (with $2,500 deductibles reducing premiums by roughly 15% compared to $1,000 deductibles), though this shifts more financial responsibility to property owners when claims occur.

Risk Mitigation Features Lower Insurance Costs

Security systems, smoke detectors, and enhanced safety features can reduce premiums by 10-20% across most Utah markets. Properties with professional management companies often qualify for discounts because insurers view professional oversight as risk reduction. Pool fencing, hot tub covers, and other safety equipment demonstrate proactive risk management that insurers reward with lower rates. Some carriers offer additional discounts for properties that complete annual safety inspections or maintain detailed guest screening procedures.

These cost factors create significant premium variations that property owners must navigate when they select coverage levels, but understanding short-term rental insurance gaps proves even more important for protecting your investment.

Where Does Standard Insurance Leave You Exposed

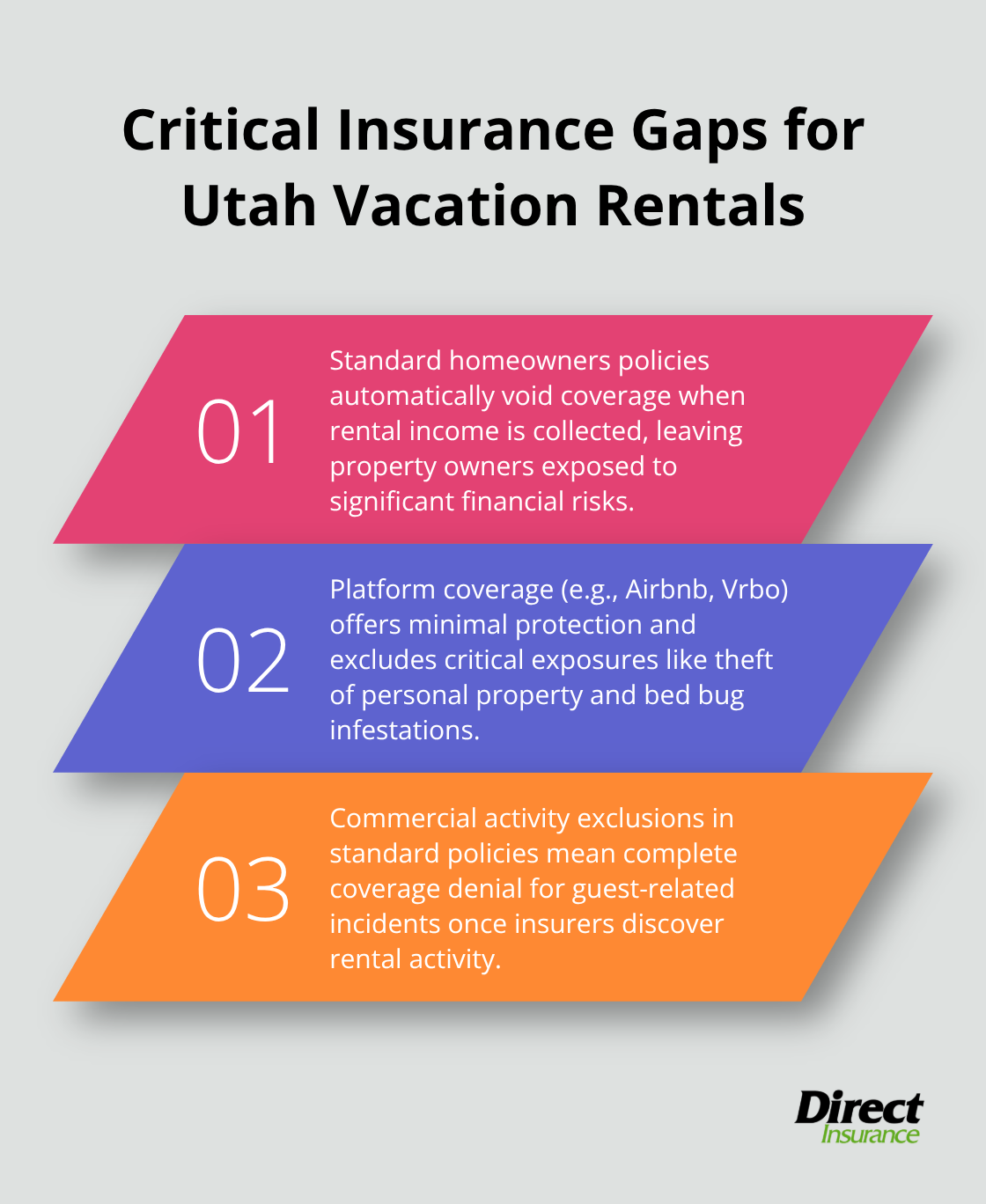

Standard homeowners insurance policies automatically void coverage the moment you collect rental income, which creates immediate exposure for Utah vacation rental owners. The Insurance Information Institute confirms that traditional policies exclude commercial activities, which means a single reservation transforms your covered property into an uninsured liability. Property owners often discover this gap only after they file claims, when insurers deny coverage and leave them with thousands in unprotected damages. Utah’s Short-Term Rental Act compounds this problem by mandating liability coverage between $500,000 and $1 million (levels that standard policies never provide for rental activities).

Platform Coverage Creates False Security

Airbnb and Vrbo host protection programs offer minimal coverage that stops far short of comprehensive protection, with Airbnb’s $1 million liability coverage that excludes property damage entirely. These platforms provide secondary coverage only, which means they pay claims only after your primary insurance denies coverage or exhausts limits. Platform coverage excludes critical exposures like theft of personal property, bed bug infestations, and squatter situations. Utah residents are being overrun by short-term rental property owners who risk paying a $650 fee if it means profiting over $1000 per night. The National Association of Insurance Commissioners warns that platform protection contains significant exclusions, such as intentional damage, normal wear and tear, and cash or securities theft. Property owners who rely solely on platform coverage face substantial gaps during the 60-day claims processing periods, when damaged properties remain unrentable and income stops completely.

Weather Extremes Expose Seasonal Properties

Utah’s extreme weather patterns create unique insurance challenges for vacation rental properties, particularly those that operate seasonally in mountain resort areas. Properties closed during winter months face frozen pipe risks that standard policies may exclude if the property appears unoccupied, while summer-only operations miss wildfire season protections when coverage lapses. The Utah Department of Insurance reports increased weather-related claims, with properties in Park City and Alta that experience 35% higher claim frequencies due to heavy snow loads and rapid temperature changes. Seasonal property owners often reduce coverage during off-seasons to save money, but this strategy backfires when unexpected incidents occur during supposedly quiet periods.

Commercial Activity Exclusions Hit Hard

Standard policies contain specific language that excludes any business use of residential properties, which means vacation rental activities void coverage immediately upon the first reservation. Insurers classify short-term rentals as commercial enterprises that require specialized coverage, not residential endorsements or add-ons. Property owners face complete coverage denial for guest-related incidents, theft, or property damage once insurers discover rental activity. This exclusion applies retroactively, which means insurers can deny previous claims if they later discover unreported rental income.

Final Thoughts

Utah vacation rental owners must secure proper insurance coverage before their next guest checks in. The state’s $400 million vacation rental market demands specialized protection that standard homeowners policies cannot provide. Property owners who operate without adequate vacation rental insurance Utah coverage face financial ruin from guest injuries, property damage, or income losses.

Contact insurance professionals who understand Utah’s unique rental requirements and local regulations. We at Direct Insurance Services have served Utah property owners for decades, and we shop multiple top-rated insurance companies to find the best coverage at competitive rates. Our local team understands the specific risks that face Utah vacation rental owners (from mountain weather hazards to tourist-heavy liability exposures).

Proper coverage selection requires you to balance adequate protection with reasonable costs. Property owners need $1 million minimum liability coverage, replacement cost property protection, and income interruption coverage that matches their rental income potential. The investment in specialized vacation rental insurance protects against catastrophic losses that could eliminate years of rental profits in a single incident.