Airbnb Insurance in Utah A Guide for Hosts

Utah’s short-term rental market has grown 47% since 2020, making proper insurance coverage more important than ever for hosts.

Standard homeowners policies don’t cover commercial rental activities, leaving many Airbnb hosts exposed to significant financial risks. We at Direct Insurance Services see hosts facing liability claims up to $1 million when guests get injured or damage occurs.

This guide covers everything you need to know about Airbnb insurance in Utah to protect your investment and guests.

What Insurance Requirements Must Utah Airbnb Hosts Meet?

Utah State Mandates $1 Million Liability Coverage

Utah’s Short-Term Rental Act requires hosts to carry liability insurance with minimum coverage of $500,000 to $1 million. This requirement applies statewide, but individual cities add their own layers of complexity. Salt Lake City requires hosts to provide proof of insurance during the license application process, while St. George demands health and safety inspections alongside insurance documentation.

Park City takes a stricter approach and requires hosts to maintain commercial general liability policies specifically for rental properties. These regulations exist because standard homeowners insurance contains business activity exclusion clauses that void coverage when you rent your property for commercial purposes.

Airbnb’s Host Protection Creates Coverage Gaps

Airbnb’s Host Protection Insurance provides liability coverage up to $1 million, which technically meets Utah’s minimum requirement. However, this coverage only activates when guests occupy your property and excludes property damage to your home and belongings. The platform’s AirCover program offers up to $1 million in damage protection, but it doesn’t cover vacant periods, natural disasters, or mold damage.

Most concerning for Utah hosts is that AirCover requires you to negotiate directly with guests before you file claims. This creates delays when you need immediate repairs during peak ski season or summer tourist periods (when bookings are most valuable).

Standard Homeowners Policies Exclude Rental Activities

Traditional homeowners insurance excludes short-term rental activities entirely due to commercial use restrictions. This means any guest-related incident, theft, or property damage won’t receive coverage under your existing policy. Utah hosts who operate without proper coverage face personal liability for medical bills, legal fees, and property repairs that can easily exceed $100,000.

Renters insurance provides no protection for hosts, which leaves you completely exposed when guests damage your property or injure themselves during their stay. These coverage gaps make specialized short-term rental insurance not just recommended but necessary for Utah hosts who want to protect their investment and avoid financial disaster.

What Coverage Do Utah Airbnb Hosts Actually Need?

Liability Protection for Guest Incidents

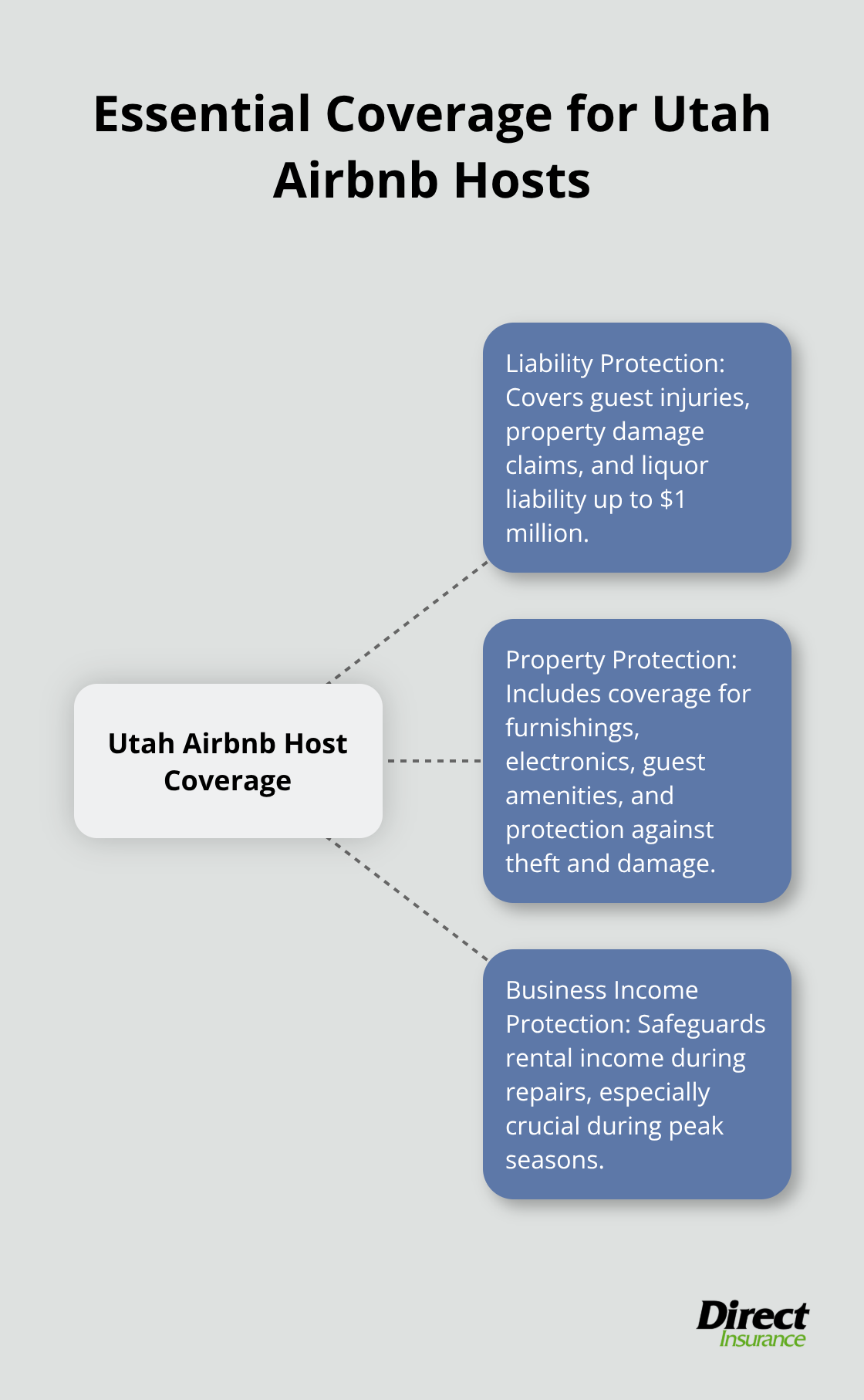

Utah Airbnb hosts need three types of specialized coverage that standard policies won’t provide. Proper Insurance offers policies that start at $1 million in Commercial General Liability protection, which covers guest injuries from hot tub accidents, slip-and-fall incidents, and property damage claims that can easily reach six figures. Their coverage includes liquor liability protection when guests consume alcohol during stays, plus bed bug and flea extermination costs up to $25,000 per incident.

This specialized approach addresses real risks that hosts face daily, unlike generic policies that exclude rental activities entirely. Standard homeowners policies contain business activity exclusions that void coverage the moment you accept rental income.

Property Protection Beyond Basic Coverage

Property protection must extend beyond basic dwelling coverage to include furnishings, electronics, and guest amenities that standard homeowners policies exclude. Proper Insurance covers guest-caused theft and damage with no deductible for items under $3,000, plus squatters protection that provides legal support and income coverage when guests refuse to leave.

Utah hosts face unique risks from seasonal guests who may damage ski equipment storage areas or outdoor amenities during winter months. Standard policies exclude these rental-related damages entirely, which leaves hosts personally liable for replacement costs.

Business Income Protection

Business interruption coverage protects rental income during repairs. Utah’s seasonal rental market makes this protection vital during peak ski season and summer months when daily rates can exceed $400. Revenue protection kicks in immediately when property damage prevents bookings, unlike platform coverage that requires lengthy negotiations with guests before any reimbursement begins.

Peak season bookings in Park City and Moab generate the highest annual income for most hosts, making income protection essential when repairs coincide with high-demand periods. While sites like Airbnb do offer some property protection for hosts against damage by a guest, it does not include liability insurance. The right insurance provider will understand these seasonal revenue patterns and structure coverage accordingly.

Which Insurance Provider Should Utah Hosts Choose?

Utah Airbnb hosts face a clear choice between commercial insurance policies and specialized short-term rental coverage, with specialized policies proving superior in almost every scenario. Commercial insurance policies typically cost 30-40% more than specialized options while they provide less comprehensive coverage for rental-specific risks. Proper Insurance, endorsed by Vrbo, offers policies that start at $1 million in liability coverage with no deductible for items under $3,000, while traditional commercial policies often carry $5,000-$10,000 deductibles that make small claims financially impractical.

Specialized Policies Beat Commercial Coverage

Proper Insurance includes unique protections like bed bug extermination coverage up to $25,000 and squatters protection with legal support, features completely absent from standard commercial policies. Traditional commercial insurers exclude liquor liability and pet damage, two common claims that specialized providers cover automatically. The revenue protection that specialized insurers offer has no time limits and covers the full amount hosts choose, while commercial policies typically cap business interruption coverage at 12 months with complex calculation methods that often shortchange hosts during peak seasons.

Utah Insurance Companies With STR Experience

Local agents who specialize in short-term rentals can structure policies that account for Utah’s seasonal revenue patterns and specific municipal requirements. Many cities and counties require local permits or licenses, which makes proper insurance coverage essential to protect these investments. The key advantage of working with experienced local agents is their understanding of Utah’s patchwork of regulations (where St. George fines unlicensed operators $750 per day while Park City requires commercial general liability policies specifically for rental properties).

Cost Factors That Actually Matter

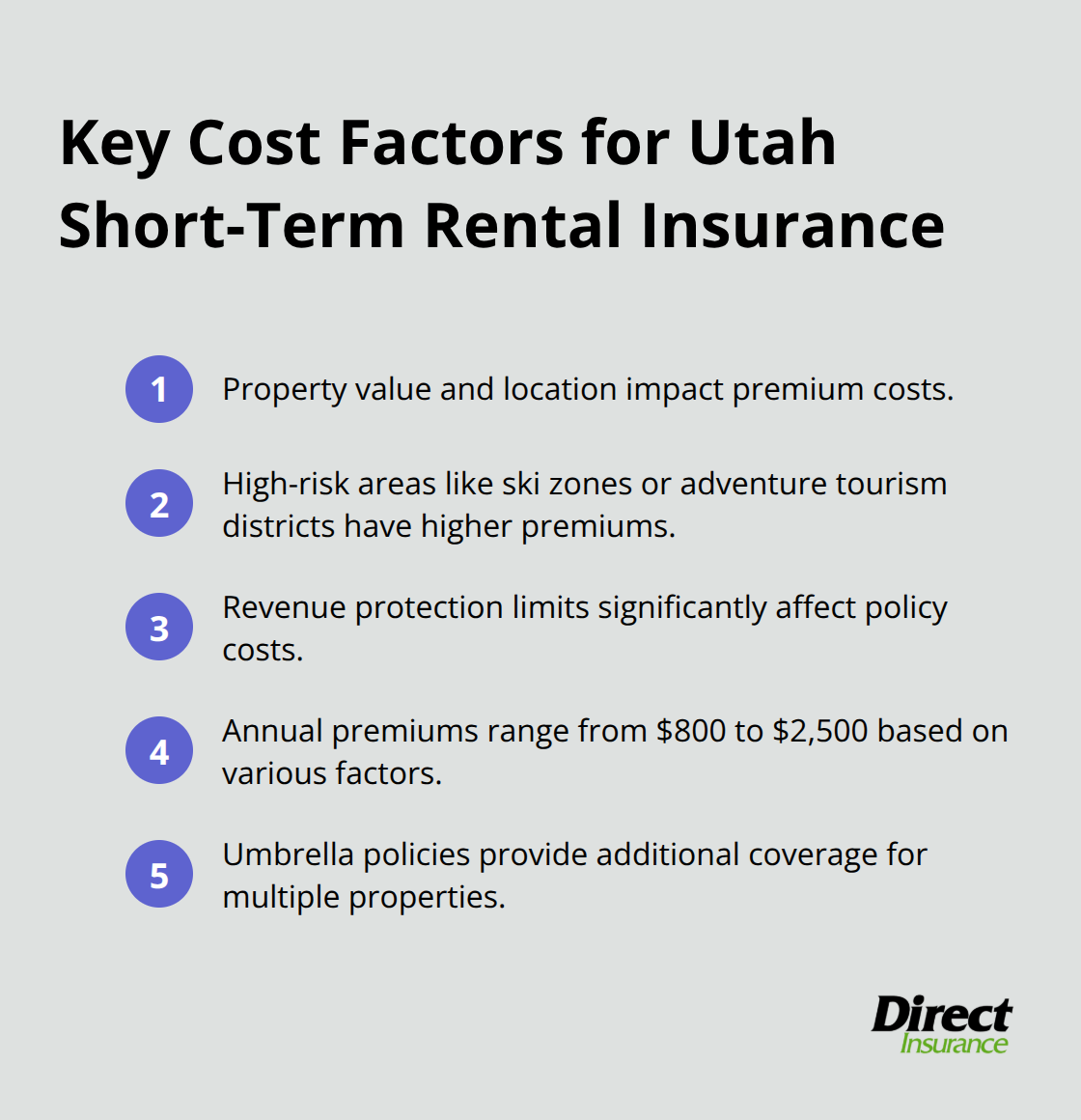

Annual premiums for specialized short-term rental insurance in Utah range from $800-$2,500 based on property value, location, and coverage limits. Properties in high-risk areas like Park City’s ski zones or Moab’s adventure tourism districts command higher premiums due to increased liability exposure. The most significant cost factor is revenue protection limits, with policies that cover $100,000 in annual rental income costing approximately $400 more than basic liability-only coverage. Hosts who operate multiple properties should consider umbrella policies that provide additional liability coverage above standard limits (particularly important when they manage properties that generate combined annual revenues exceeding $200,000).

Final Thoughts

Utah Airbnb hosts must carry minimum $1 million liability coverage to meet state requirements, but specialized short-term rental insurance provides far better protection than basic compliance. Standard homeowners policies exclude rental activities entirely, which leaves hosts personally liable for guest injuries, property damage, and lost income during repairs. Proper Airbnb insurance Utah coverage includes liability protection, property damage coverage for furnishings and amenities, plus business interruption insurance that protects rental income during peak seasons.

Specialized providers like Proper Insurance offer comprehensive policies that start around $800 annually, while commercial alternatives cost 30-40% more with higher deductibles and coverage gaps. The most effective approach involves work with experienced local agents who understand Utah’s complex municipal requirements and seasonal revenue patterns (where St. George fines unlicensed operators $750 per day while Park City requires commercial general liability policies). These agents can structure policies that account for your specific property risks and revenue goals.

We at Direct Insurance Services help Utah property owners shop multiple carriers to find optimal coverage at competitive rates. Take action now by review your current coverage, obtain quotes from specialized providers, and consult with local insurance professionals who understand short-term rental risks. Your investment and guests deserve protection that actually works when claims occur.