Utah Auto Insurance Quotes: A Simple Way to Compare Rates

Utah auto insurance quotes vary wildly between companies. The same driver can see rate differences of hundreds of dollars annually, depending on which insurers they compare.

At Direct Insurance Services, we’ve seen firsthand how many Utah drivers overpay simply because they never shop around. Getting multiple quotes takes less than an hour and can save you real money on your premiums.

How Utah Auto Insurance Quotes Work

What Information Insurance Companies Need From You

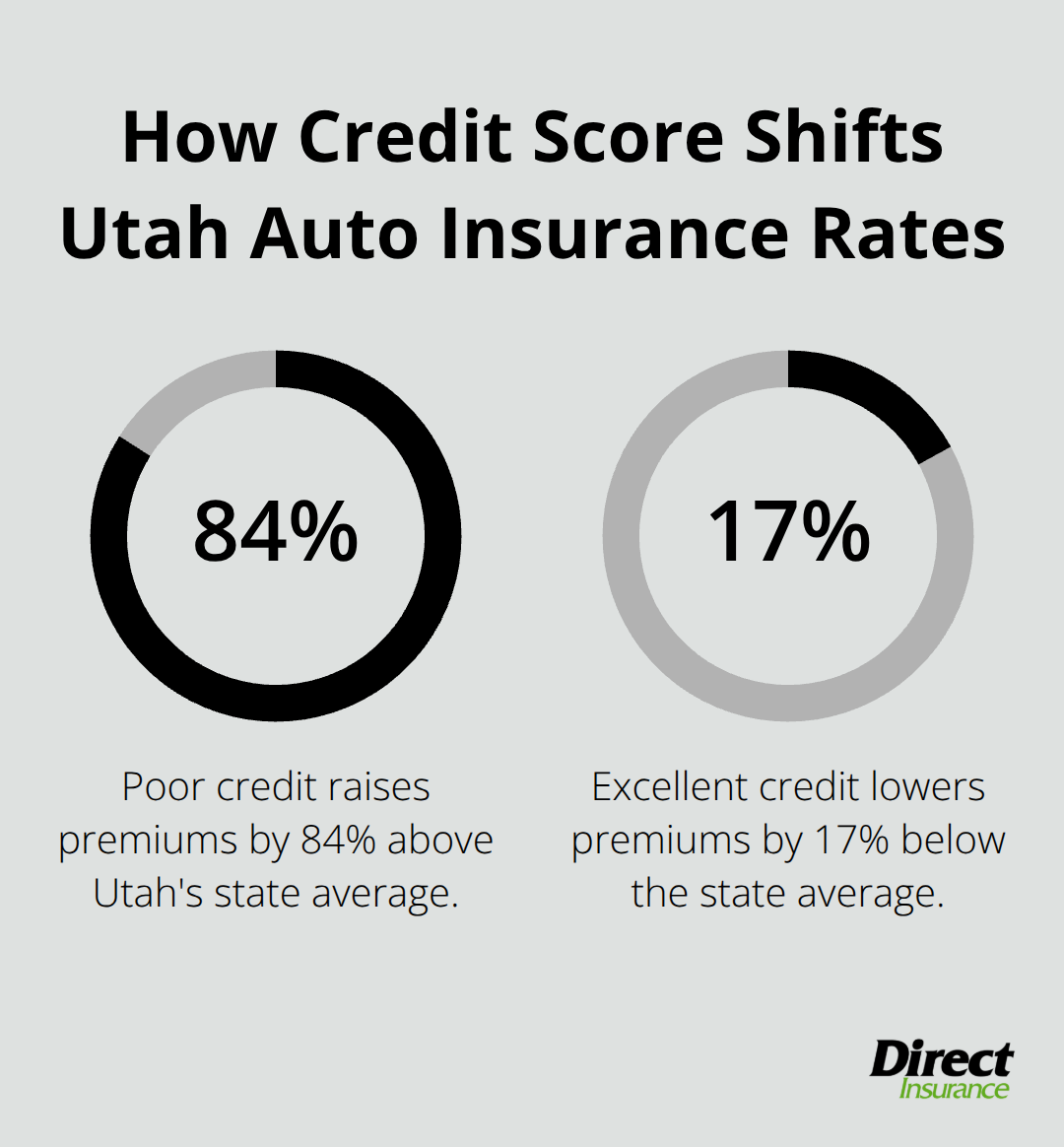

Insurance companies request specific details to calculate your Utah rate, and the information you provide directly impacts your quote accuracy. When you request a quote, you’ll answer questions about your location within Utah, your vehicle’s make and model, your age and driving history, annual mileage, and the coverage limits you want. Some insurers ask about your credit score, marital status, and whether you’ve had prior insurance. This data matters because insurers use it to assess risk. A driver in Salt Lake City with an average full-coverage premium of around $2,375 per year might pay significantly less in Saint George, where rates average roughly $1,987 annually according to Bankrate analysis. Your vehicle type also shifts the calculation dramatically-a BMW 330i costs about $2,661 per year for full coverage while a Honda Odyssey runs approximately $2,008, both in Utah with standard driver profiles. Driving history carries substantial weight in this equation. A clean record costs around $2,188 per year for full coverage, but a speeding ticket jumps that to $2,701, an at-fault accident raises it to $3,140, and a DUI pushes it to $4,275. Credit score matters too-poor credit can inflate your premium to about $4,033 (roughly 84% above the state average), while excellent credit can reduce it to around $1,818 (about 17% below average). The faster you provide accurate information, the faster you receive real quotes to compare.

Why Multiple Quotes Reveal Hidden Savings

You need to shop multiple quotes if you want a competitive rate. A nationwide survey from October 2024 through September 2025 showed drivers switching to certain carriers saved over $700 annually, with examples like $817 less than GEICO, $731 less than Progressive, $839 less than State Farm, and $758 less than Allstate. USAA offers the lowest average rate in Utah at about $1,244 per year, roughly $753 below the state average, though eligibility requires military service or family connection. GEICO ranks second with rates around $1,287 annually. The spread between the cheapest and most expensive major insurers in Utah is substantial-USAA at $1,244 versus Farmers at $2,618 represents a $1,374 annual difference for identical coverage. This gap exists because insurers price risk differently based on their claims data, underwriting philosophy, and available discounts. One carrier might offer a 30% discount for good driving through telematics programs, while another doesn’t participate in usage-based insurance at all. You can obtain quotes from at least three major carriers in roughly five minutes per company. Rates vary significantly based on where you live in the state, your vehicle type, age, and driving history, making direct comparison the only reliable way to find your best price.

How Insurance Companies Calculate Your Rate

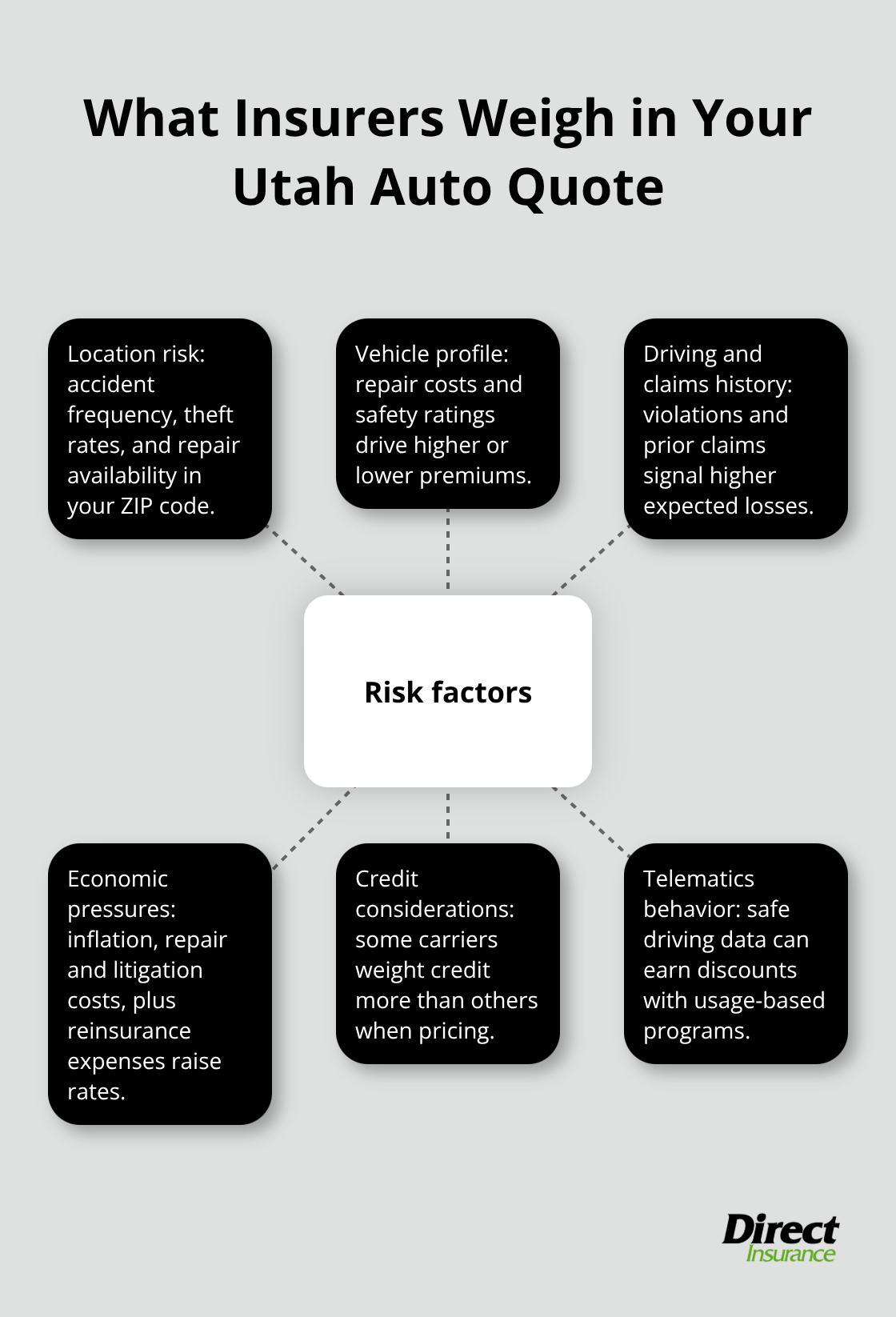

Insurance companies apply different formulas to the information you provide, which explains why identical drivers receive vastly different quotes. Insurers consider your location’s accident frequency and theft rates, your vehicle’s repair costs and safety ratings, your age and driving experience, and your claims history. They also factor in construction and repair costs (higher in dense areas when supply is tight), inflation, litigation costs, and their own reinsurance expenses. Some insurers weight certain factors more heavily than others-one company might prioritize your credit score while another focuses primarily on driving record. Telematics devices that monitor your actual driving behavior (speeding, hard braking, acceleration) can lower your premium with carriers that offer usage-based programs.

The Utah Insurance Department requires that rates not be excessive, inadequate, or unfairly discriminatory, but this regulation still allows substantial variation between carriers. Understanding these calculation differences helps explain why shopping around matters so much for Utah drivers.

Common Factors That Affect Your Utah Auto Insurance Rates

Your Driving Record Determines Your Premium More Than Anything Else

Your driving record stands as the single most influential factor in your Utah auto insurance quote. Insurance companies treat violations as concrete evidence of future risk. Claims history matters equally-if you’ve filed claims in the past, insurers view you as statistically more likely to file again. Safe driving directly translates to lower premiums, and even one violation can cost you thousands over several years.

Vehicle Type and Location Create Dramatic Cost Differences

Your vehicle choice and where you live in Utah create substantial premium swings that most drivers underestimate. A BMW 330i costs roughly $2,661 annually for full coverage while a Honda Odyssey runs about $2,008-a $653 difference for identical driver profiles, according to Bankrate data. The Odyssey’s lower repair costs and superior safety ratings make it cheaper to insure. Geographic location within Utah matters enormously too. Salt Lake City drivers pay approximately $2,375 per year for full coverage, while Provo averages about $2,220 and Saint George approximately $1,987-differences driven by accident frequency, theft rates, and repair shop availability in each area.

Age and Credit Score Impact Your Rate Significantly

Your age compounds these factors significantly. An 18-year-old on their own policy averages $7,384 annually for full coverage versus $4,467 on a parent’s policy-a $2,917 gap simply from age and experience. A 70-year-old pays around $2,234 per year. Credit score wields surprising power over your rate too. Poor credit inflates premiums to about $4,033 (84 percent above state average) while excellent credit reduces them to approximately $1,818 (17 percent below average).

Coverage Limits You Select Shape Your Final Quote

Coverage limits you select directly impact your quote. Minimum coverage averages roughly $69 monthly while full coverage runs about $182 monthly in Utah. These aren’t theoretical differences; they’re concrete costs that separate affordable insurance from budget-breaking policies. Understanding how each factor influences your rate helps you make informed decisions about which coverage levels make sense for your situation and budget.

How to Shop Utah Auto Insurance Quotes Effectively

Getting multiple quotes is non-negotiable if you want a competitive rate, but how you shop matters just as much as that you shop. Start by collecting your information once and reusing it across quotes rather than answering the same questions repeatedly for each insurer. You’ll need your vehicle identification number, current coverage details if you have existing insurance, and your driving history. Enter your ZIP code first because location determines which carriers will quote you and heavily influences your rate. Bankrate data shows Salt Lake City drivers pay $2,375 annually for full coverage while Saint George residents average $1,987 for identical coverage, making your specific location critical to accurate quotes. Get quotes from at least three major carriers to see real variation in pricing. USAA offers the lowest average rate in Utah at $1,244 per year if you qualify through military service, GEICO ranks second at $1,287, and Progressive specializes in insuring drivers with DUI history at rates around $1,773 for that specific situation. The difference between the cheapest quote and the most expensive can easily exceed $1,000 annually for the same coverage, which is why comparing matters. Most quote tools take roughly five minutes per company, meaning you can obtain three solid quotes in about fifteen minutes total.

Discounts Often Matter More Than Base Rates

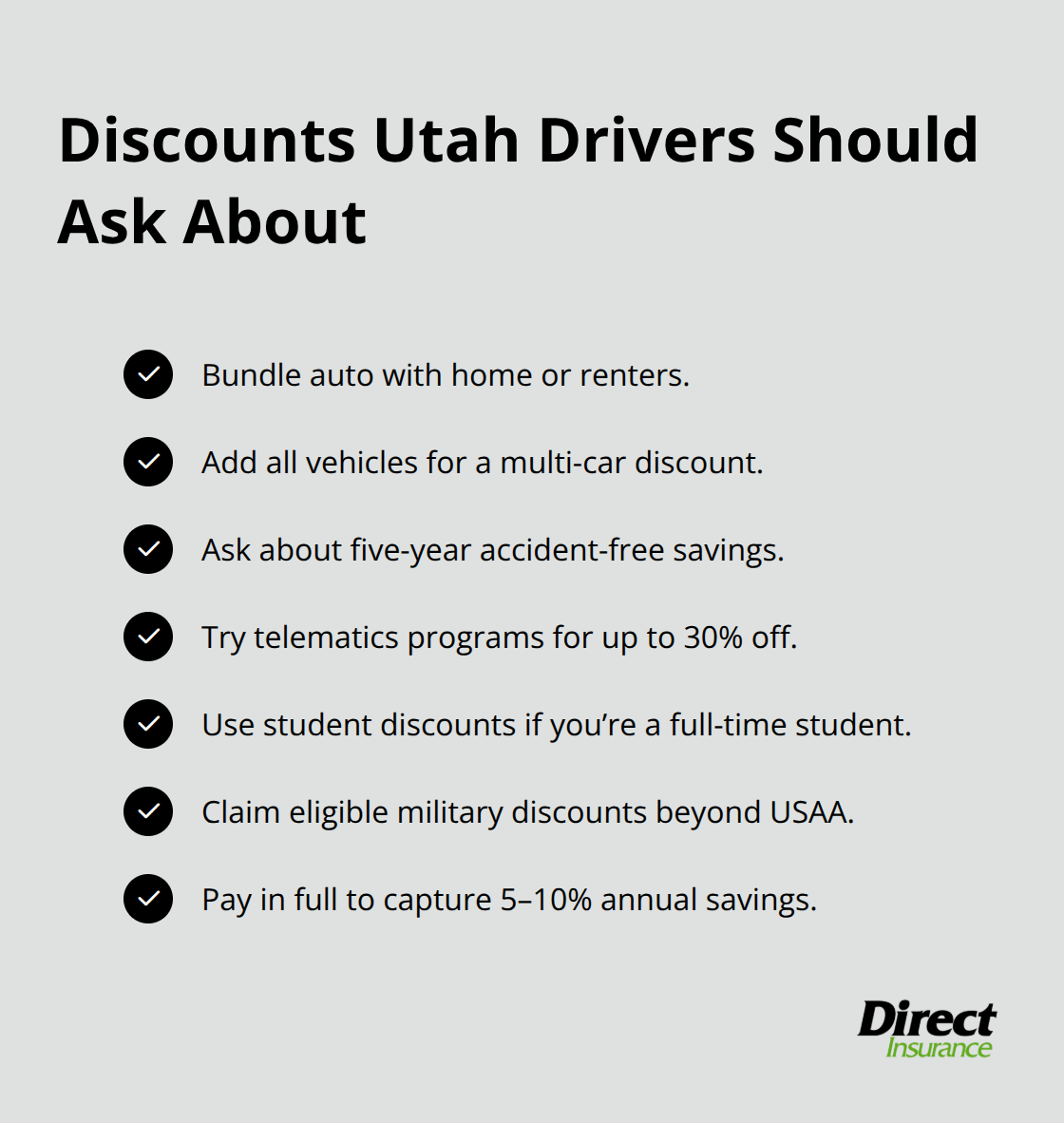

Many Utah drivers focus entirely on the base premium and ignore available discounts, which is a critical mistake. Ask every insurer about bundling auto with home or renters insurance, which can yield substantial savings if you qualify. Multi-car discounts apply if you insure multiple vehicles with the same company, and some insurers offer five-year accident-free discounts that reduce your premium significantly. Telematics programs like Liberty Mutual’s RightTrack can cut premiums by up to thirty percent if you maintain safe driving habits and participate in the monitoring program. Student discounts exist for full-time college students, and military discounts apply beyond USAA to carriers like GEICO. The critical action here is asking directly rather than assuming these discounts apply automatically. When comparing quotes, ensure you compare identical coverage levels and deductibles across all quotes, otherwise you won’t see true price differences.

A quote with a two thousand five hundred dollar deductible will naturally cost less than one with a five hundred dollar deductible, but they’re not equivalent products. Paying your premium in full rather than in monthly installments sometimes qualifies for a discount worth five to ten percent annually.

Timing Your Quote Shopping Strategically

Shop annually as your policy renewal approaches to gain leverage for negotiating or switching carriers. Your driving record improves each year you remain violation-free, which should lower your quote. However, if you’ve had a recent accident or ticket, waiting six months to a year before shopping can save you money since these incidents age off your record gradually. When you obtain new quotes, ask your current insurer if they’ll match a lower quote from a competitor rather than automatically switching. Some insurers will adjust your rate to retain you, though this doesn’t always work. Test different deductible levels during your quote process to understand how they affect your price. Increasing your deductible from five hundred to one thousand dollars typically lowers your premium noticeably, though you must be able to pay that deductible out of pocket if you file a claim. For older vehicles with minimal value, run quotes both with and without comprehensive and collision coverage to see if dropping these coverages makes financial sense. A vehicle worth three thousand dollars might not justify paying five hundred dollars annually for collision coverage, though your lender will require it if you have an active loan.

Compare Coverage Levels Accurately

Accurate comparison requires matching coverage across all quotes you receive. Many drivers accidentally compare apples to oranges by requesting different deductibles or coverage limits from each insurer. This practice masks true price differences and leads to poor decisions. When you request quotes, specify the exact same coverage limits and deductibles for each company so you see genuine pricing variation. Minimum coverage in Utah averages roughly $69 monthly while full coverage runs about $182 monthly, representing a substantial difference that reflects your actual protection level. Understanding this gap helps you make informed decisions about which coverage levels make sense for your situation and budget.

Conclusion

Shopping multiple Utah auto insurance quotes isn’t optional if you want a competitive rate. The data proves it: drivers who compare quotes from at least three carriers save hundreds of dollars annually. USAA charges $1,244 per year while Farmers averages $2,618 for identical coverage, and that $1,374 gap exists because insurers calculate risk differently and offer varying discounts.

Your driving record, vehicle type, location, age, and credit score all influence your rate, but no single factor matters more than shopping around. One carrier might provide a telematics discount that cuts your premium by thirty percent while another doesn’t offer usage-based programs at all. You won’t know your best option without requesting quotes, and the process takes roughly fifteen minutes for three solid comparisons. Enter your ZIP code first since location heavily influences your rate, then provide consistent information across all requests so you see genuine pricing variation rather than coverage differences.

At Direct Insurance Services, we’ve specialized in comparing top-rated insurance companies to help Utah drivers find the best coverage at competitive rates. Contact us today to discuss your options and confirm you’re not overpaying for protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation