Homeowners Insurance Rates Utah: What Affects Premiums

Homeowners insurance rates in Utah vary significantly based on where you live and what risks your home faces. At Direct Insurance Services, we’ve helped countless Utah homeowners understand why their premiums are what they are.

This guide breaks down the specific factors that shape your costs, from wildfire exposure to winter weather threats. You’ll also learn concrete steps to reduce what you pay.

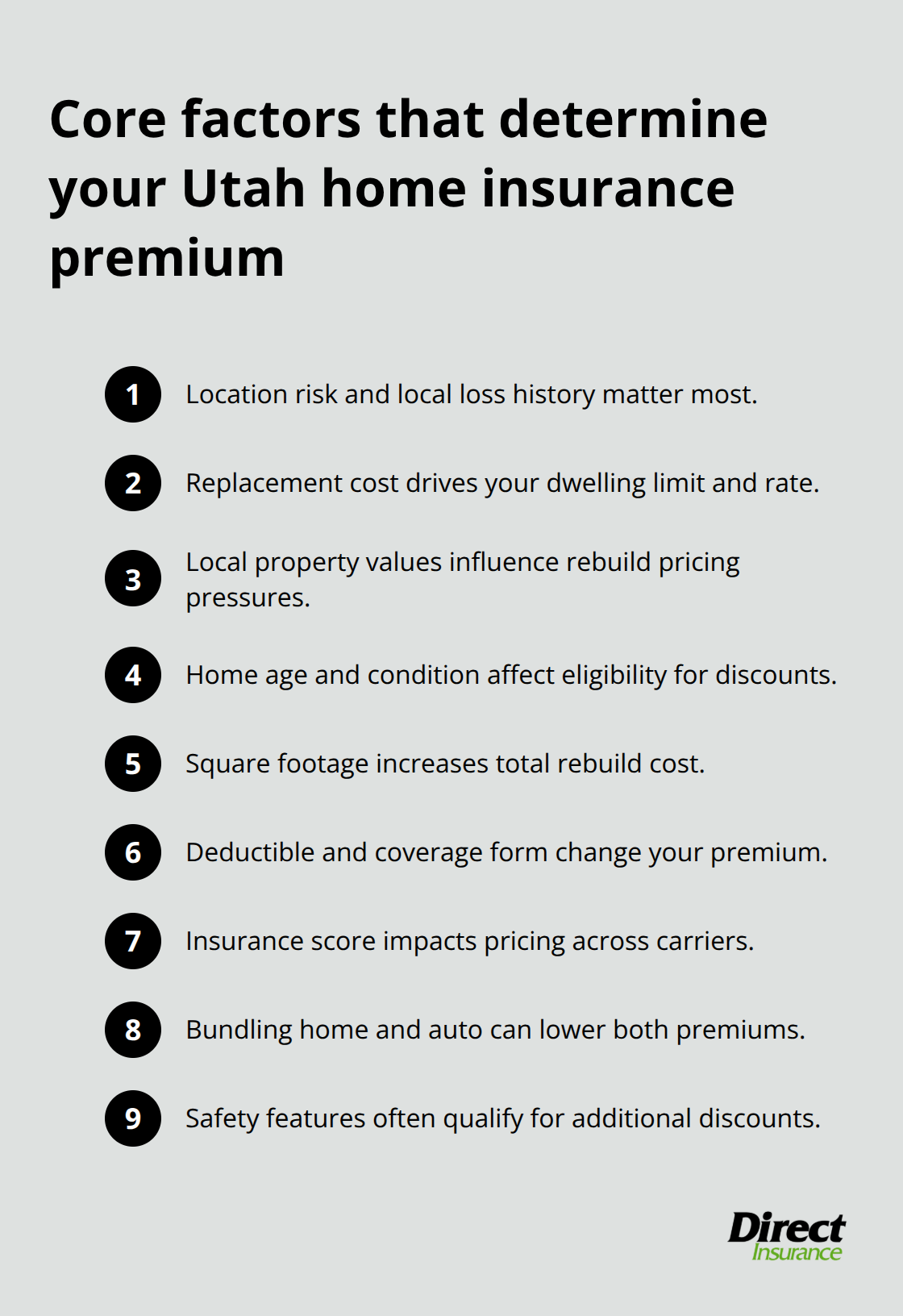

What Actually Determines Your Utah Home Insurance Premium

Location drives your premium more than any other factor, and Utah’s data tells a clear story. Utah still ranks in the top 10 states nationwide for the highest percent increase in homeowners insurance from 2020 to 2024. Insurers calculate premiums based on replacement cost (what it actually costs to rebuild your home), local property values, and risk factors specific to each area. If you live in a county with higher wildfire exposure or more severe winter weather, your premium reflects that reality.

How Home Age and Size Affect What You Pay

Your home’s age directly influences your premium. Newer homes qualify for more discounts because they have updated electrical, plumbing, and roofing systems that pose lower risk. Older homes often miss out on these discounts unless you invest in upgrades. Square footage matters equally. A 2,000 square foot finished home in Utah typically requires a rebuild cost estimate around $350,000, or roughly $175 per square foot, which directly feeds into your premium calculation.

Larger homes cost more to rebuild, so square footage drives premium increases regardless of how old your home is.

Your Deductible Shapes Your Monthly Cost

A higher deductible is the fastest way to lower your premium, but only if you can actually pay it out of pocket when a claim happens. Moving from a $500 deductible to $1,000 reduces what you owe monthly, yet many homeowners select a deductible they cannot afford when disaster strikes. Your coverage form also shapes your costs significantly. An HO-3 policy covers more perils than an HO-2, which means you pay more but receive broader protection. Replacement Cost Value coverage for your belongings costs more upfront than Actual Cash Value, but it pays you the current replacement price rather than depreciated value.

Coverage Limits and Insurance Scores Impact Your Rate

The Utah Insurance Department and the National Association of Insurance Commissioners both recommend matching your dwelling limit to actual replacement cost, not your home’s market value. Overinsuring wastes money on unnecessary premium; underinsuring leaves you exposed when you need it most. Your insurance score, often based on credit metrics, materially impacts your rate. Bundling your homeowners policy with auto coverage through the same insurer typically yields a multi-policy discount that reduces both premiums. Safety features like monitored security systems, deadbolt locks, and smoke detectors can qualify you for meaningful discounts-ask your agent specifically which ones apply to your situation.

These premium factors set the foundation for understanding your costs, but Utah’s unique environmental risks add another layer to the equation.

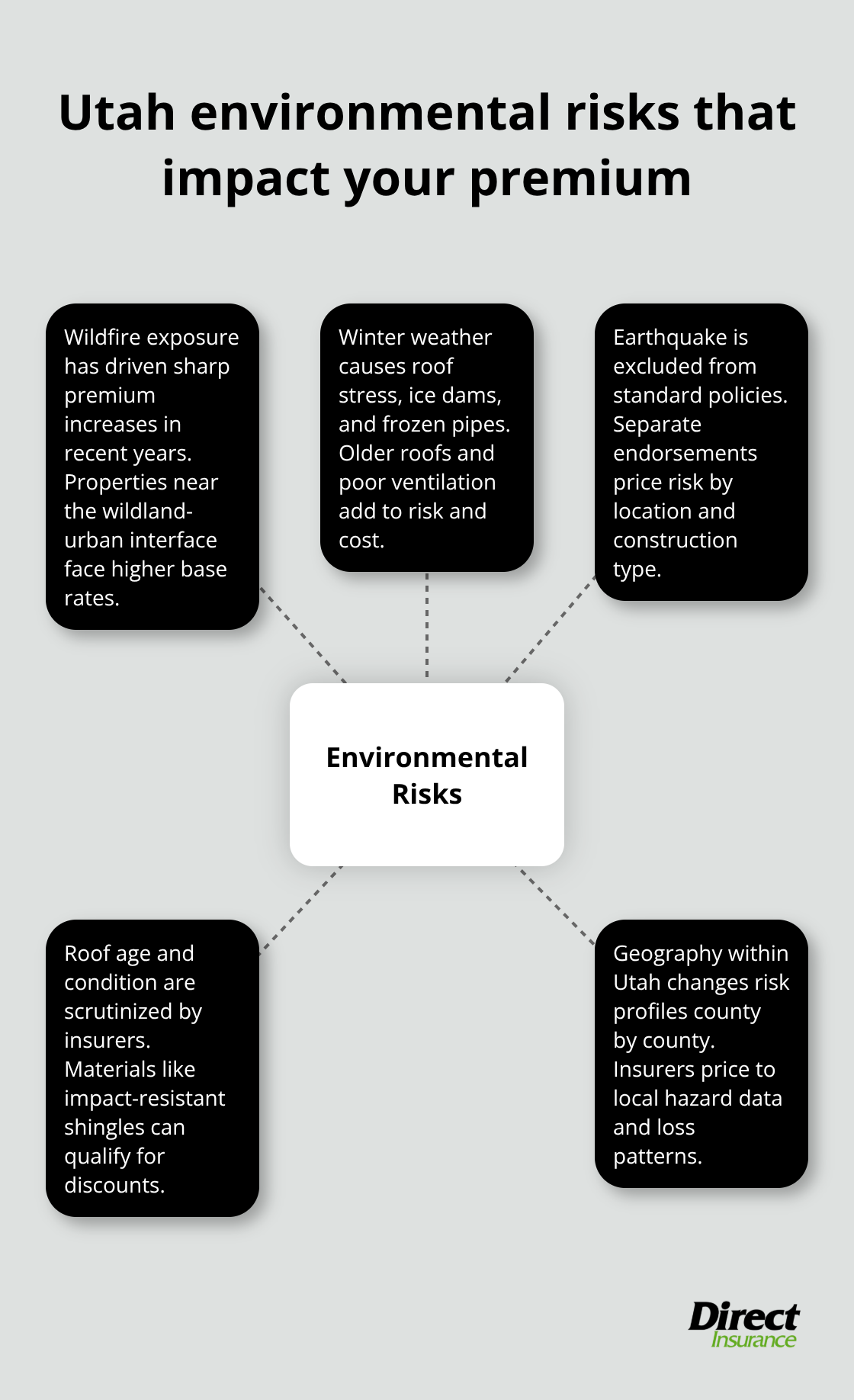

Utah’s Environmental Risks and Your Insurance Costs

Wildfire exposure stands as the single biggest reason Utah homeowners pay more for insurance than they did four years ago. According to the National Bureau of Economic Research analysis using CoreLogic data, Grand County saw the largest premium increase in Utah at 154.4 percent between 2020 and 2023, jumping from $773.09 to $1,966.88 annually. Summit County followed at 96.8 percent, and Weber County at 86.4 percent. These sharp increases reflect real wildfire risk. Homes in wildland-urban interface areas face genuine exposure, and insurers price that directly into your premium.

Wildfire Risk and Defensible Space

If your property sits in a high-risk wildfire zone, you can reduce your rate through defensible space measures. The Utah Insurance Department recommends clearing brush to at least 100 feet from your home and trimming trees that overhang your roof. This isn’t a guarantee of a discount, but many insurers recognize the effort and may offer reductions for documented risk mitigation. What matters most is that you take action before a fire season arrives-waiting until smoke fills the air accomplishes nothing.

Winter Weather and Roof Condition

Winter damage claims drive significant premium costs across Utah. Heavy snow loads stress roofs, ice dams cause water damage, and frozen pipes burst inside walls during cold snaps. Older roofing materials deteriorate faster under these conditions, which is why insurers scrutinize roof age and condition closely. If your roof exceeds 20 years old, expect higher premiums or potential coverage restrictions. Upgrading to impact-resistant shingles or metal roofing can qualify you for discounts in some cases, though the upfront cost is substantial. The cost of materials and labor to repair winter damage has climbed significantly alongside inflation, which pushes insurers to charge more for coverage. Homes with poor attic ventilation or inadequate insulation face higher interior moisture problems during freeze-thaw cycles, creating additional risk that shows up in your rate.

Earthquake Risk and Your Location

Utah sits on the Wasatch Front, one of the most seismically active regions in the interior western United States. However, earthquake risk pricing varies enormously depending on your exact location. Salt Lake County and Davis County experience different seismic profiles than rural areas further from fault lines. Standard homeowners policies exclude earthquake damage entirely, which means you must purchase a separate earthquake endorsement if you want that coverage. The cost of the endorsement depends on your home’s construction type, age, and proximity to known faults. Newer homes built with earthquake-resistant design standards often qualify for lower endorsement rates than older homes with unreinforced masonry or weak foundation connections. Most Utah homeowners skip earthquake coverage because they underestimate the risk or balk at the additional cost, but a single moderate earthquake can cause tens of thousands in damage. Understanding your specific seismic zone and whether the risk justifies the endorsement cost matters before disaster strikes-and that conversation with your agent should happen now, not after damage occurs.

How to Cut Your Utah Home Insurance Premium

The fastest way to lower your premium is to stop paying for coverage you don’t actually need. Many Utah homeowners carry overlapping policies or select coverage limits far above their home’s replacement cost, which means they waste money each month. Start by obtaining quotes from at least three different insurers, because rate variation across carriers is substantial. One insurer might quote $1,500 annually while another charges $1,800 for identical coverage on the same property. The National Association of Insurance Commissioners data confirms that shopping around remains the single most effective tactic to reduce what you pay.

Compare Quotes and Bundle Your Policies

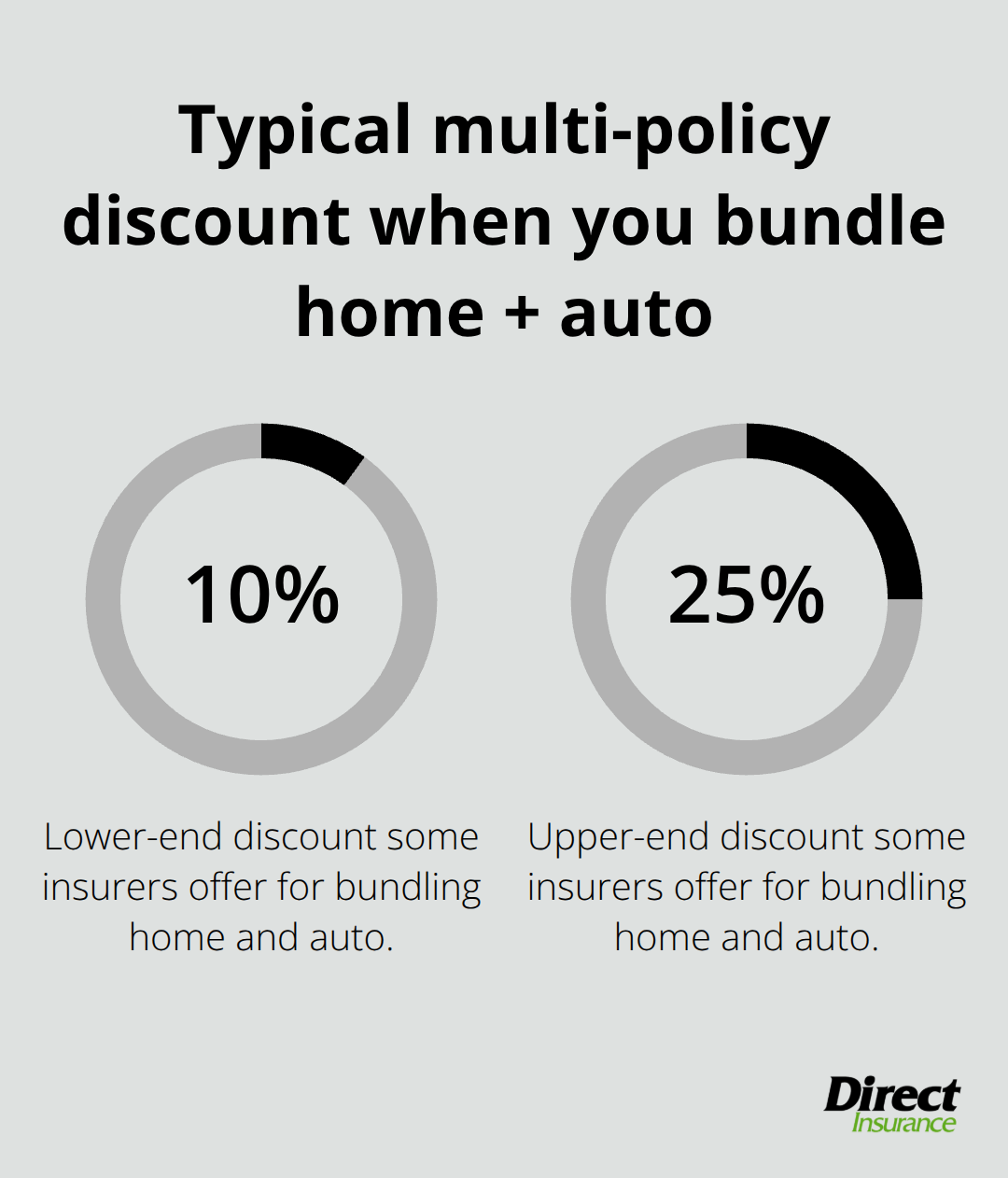

Next, bundle your homeowners policy with auto insurance through the same carrier. Multi-policy discounts typically reduce your total premium by 10 to 25 percent depending on the insurer, which translates to real savings. If you currently carry auto insurance with one company and homeowners with another, consolidating to one agent costs nothing and pays immediate dividends.

Then examine your deductible honestly. If you have $5,000 in liquid savings available, raising your deductible lowers your premium. The math works in your favor only if you can actually pay that deductible without financial stress when a claim occurs. Too many homeowners select a higher deductible to save premium dollars, then face genuine hardship when they file a claim and realize they cannot cover the out-of-pocket cost.

Leverage Safety Features and Discounts

Home safety features and recent upgrades deliver concrete premium reductions that many Utah homeowners ignore. Monitored security systems, deadbolt locks, and smoke detectors qualify for discounts at virtually every major insurer. Fire extinguishers and sprinkler systems reduce risk further and often provide additional savings. The key is telling your agent specifically which safety features your home has, because discounts don’t apply automatically. If you installed a new roof in the last five years, your premium should reflect that lower risk, but the insurer only knows if you report it.

Invest in Home Upgrades and Maintenance

Older homes miss discounts entirely unless you invest in upgrades to critical systems. Updating your electrical wiring, plumbing, roofing, and HVAC systems removes outdated risk factors that drive premiums higher. Homes with roofs under 20 years old pay substantially less than homes with aging roofs, especially in Utah’s snow-prone climate where roof condition directly affects winter damage claims. If your roof exceeds 15 years old, replacing it before shopping for insurance quotes saves more money than any discount negotiation ever will. Homes with poor attic ventilation or deteriorated insulation experience higher interior moisture damage during freeze-thaw cycles, which shows up in your rate. Addressing these maintenance issues before requesting quotes positions you to receive lower premiums from the start rather than fighting for discounts after the fact.

Final Thoughts

Your homeowners insurance rates in Utah reflect factors both within and outside your control. Location, home age, roof condition, and wildfire exposure shape your premium regardless of your choices, yet your deductible, coverage limits, safety features, and maintenance decisions directly affect what you pay each month. Utah premiums have climbed sharply since 2020, with some counties experiencing increases exceeding 80 percent, but you can take concrete action to reduce your costs.

Start by obtaining quotes from multiple insurers, since rate variation across carriers remains substantial. Bundle your homeowners and auto policies with the same company to capture multi-policy discounts that typically reduce your total premium by 10 to 25 percent, then raise your deductible if you have emergency savings to cover it. Upgrade aging roofing or electrical systems before requesting quotes, report every safety feature your home has to your agent so discounts apply automatically, and if you live in a wildfire-prone area, clear defensible space around your home and document the work.

Working with a local agent matters more in Utah than in most states because your risks are specific to this region. An agent who understands wildfire exposure in Summit County, winter damage patterns in Weber County, and seismic risk along the Wasatch Front can identify discounts and coverage gaps that national online quotes miss entirely. At Direct Insurance Services, we’ve served Utah homeowners since 1973 and understand the unique insurance needs of living here, so connect with our team to find the right policy for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation