How to Find the Perfect Home Auto Insurance Bundle

Utah homeowners can save hundreds of dollars annually by combining their home and auto coverage into a single policy. A home auto insurance bundle typically reduces costs by 10-25% compared to separate policies.

We at Direct Insurance Services help families navigate these bundling options to find maximum savings. The right bundle protects your most valuable assets while keeping premiums manageable.

How Do Home Auto Insurance Bundles Actually Work?

A home auto insurance bundle combines your homeowners and car insurance into a single policy from one provider. This arrangement streamlines your coverage management while it generates substantial discounts. When you purchase homeowners and auto insurance policies from the same company, you can typically qualify for savings of 5% to 30% off your premiums compared to separate policies. State Farm leads the market with discounts up to 25%, while American Family offers the highest potential savings at 40% for customers who qualify.

What Coverage Gets Combined

Your bundled policy maintains separate coverage limits for home and auto protection. Homeowners coverage includes dwelling protection, personal property, liability, and additional expenses for temporary housing. Auto coverage encompasses liability, collision, comprehensive, and uninsured motorist protection. The discount applies to your total premium across both policies, not individual coverage types.

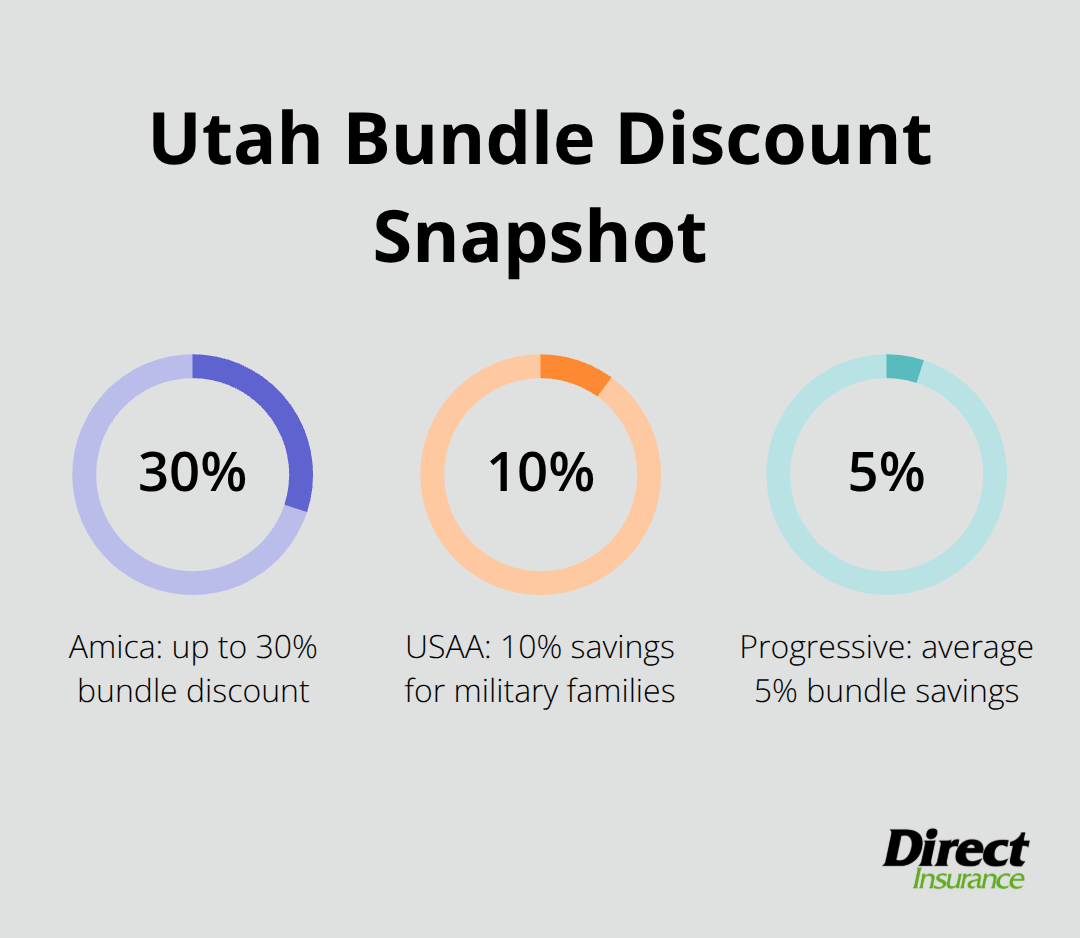

Real Savings Numbers Utah Families See

Utah residents typically pay around $2,200 annually for bundled coverage according to industry data. Separate policies would cost approximately $2,750 for equivalent protection. Amica delivers discounts up to 30% when customers combine multiple policies, while USAA offers military families 10% savings.

Progressive provides average bundle savings of 5%, though new customers can see over 20% reductions. The exact discount depends on your coverage limits, deductibles, and risk profile (factors that vary significantly between households).

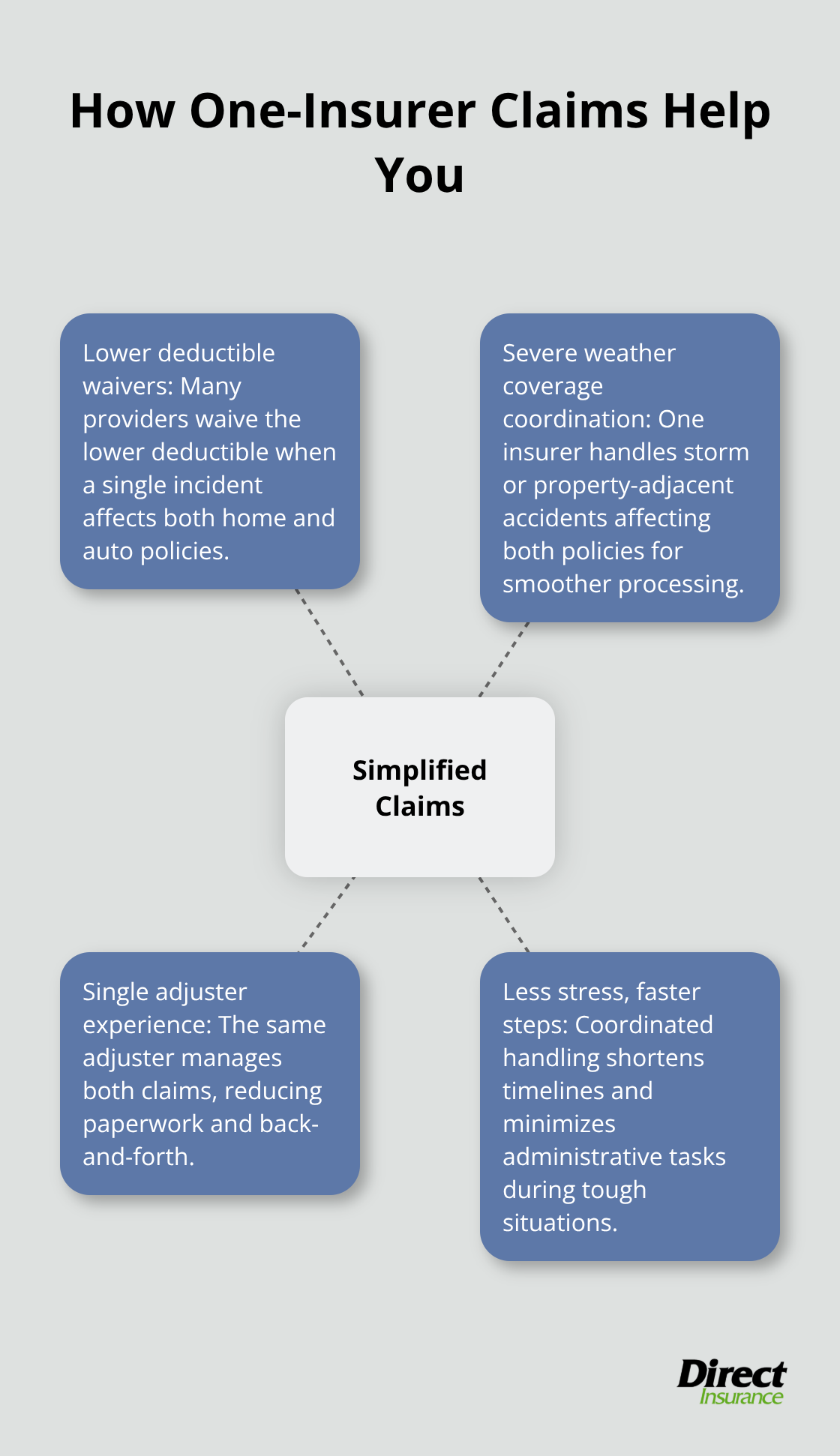

How Bundling Changes Your Claims Process

Single-insurer policies simplify claims when both your home and car suffer damage from the same incident. Many providers waive the lower deductible when you file claims that affect both policies simultaneously. This benefit proves valuable during severe weather events or accidents near your property. Your claims adjuster handles both policies, which reduces paperwork and coordination efforts during stressful situations.

Payment and Policy Management Benefits

Bundled policies consolidate your insurance payments into a single monthly or annual bill. This approach eliminates the need to track multiple due dates and payment methods (a common source of confusion for busy families). Most insurers also provide unified online portals where you can view both policies, update coverage, and file claims through one dashboard.

Now that you understand how bundles work mechanically, the next step involves comparing different bundle options to find the best fit for your specific needs and budget.

What Should You Compare When Shopping for Bundles

Smart bundle shoppers analyze three critical factors that determine actual savings and coverage quality. Start with premium comparisons across at least five providers, but calculate total costs that include fees, deductibles, and coverage gaps. State Farm’s 25% discount sounds impressive until you realize their base rates often exceed competitors by 15-20%. Geico typically offers lower starting premiums that make their smaller bundle discounts more valuable than higher-percentage savings from expensive carriers. Request quotes with identical coverage limits, deductibles, and policy terms to make accurate comparisons.

Coverage Gaps That Cost You Later

Many insurers partner with third-party companies for home coverage while they handle auto insurance directly. This arrangement creates coordination problems during claims and eliminates the single-deductible benefit for incidents that affect both properties. Farmers Insurance advertises 10% bundle savings but often uses separate companies for home coverage (which negates convenience benefits). Ask agents whether both policies come from the same underwriter and claims department. Verify that your bundle includes matching policy renewal dates, unified customer service, and consolidated billing systems that actually work together.

Questions That Reveal Hidden Problems

Ask agents specific questions that expose bundle limitations and additional costs. Demand written confirmation of discount percentages, renewal rate guarantees, and cancellation policies for both coverage types. Many providers require 30-day notice for policy changes, which complicates switching if rates increase significantly. Request examples of recent rate increases for bundled customers in Utah and ask about factors that trigger premium adjustments. Agents who avoid direct answers or provide vague responses about future pricing typically represent companies with poor rate stability (a red flag for long-term costs). Quality agents provide detailed breakdowns of coverage options, explain exclusions clearly, and offer multiple payment plans without hidden processing fees.

Rate Stability and Future Costs

Car insurance premiums have increased 55% since February 2020, while homeowners insurance rates approach $3,000 annually. These increases affect bundled policies differently across providers. Some companies raise both policy types simultaneously, while others stagger increases to retain customers. Ask for five-year rate history data and projected increases for your specific coverage profile. Companies that refuse to share this information often hide aggressive rate increases that eliminate bundle savings over time.

Once you identify providers with stable rates and genuine bundle benefits, you can focus on specific strategies to maximize your savings potential.

How Can You Maximize Your Bundle Savings

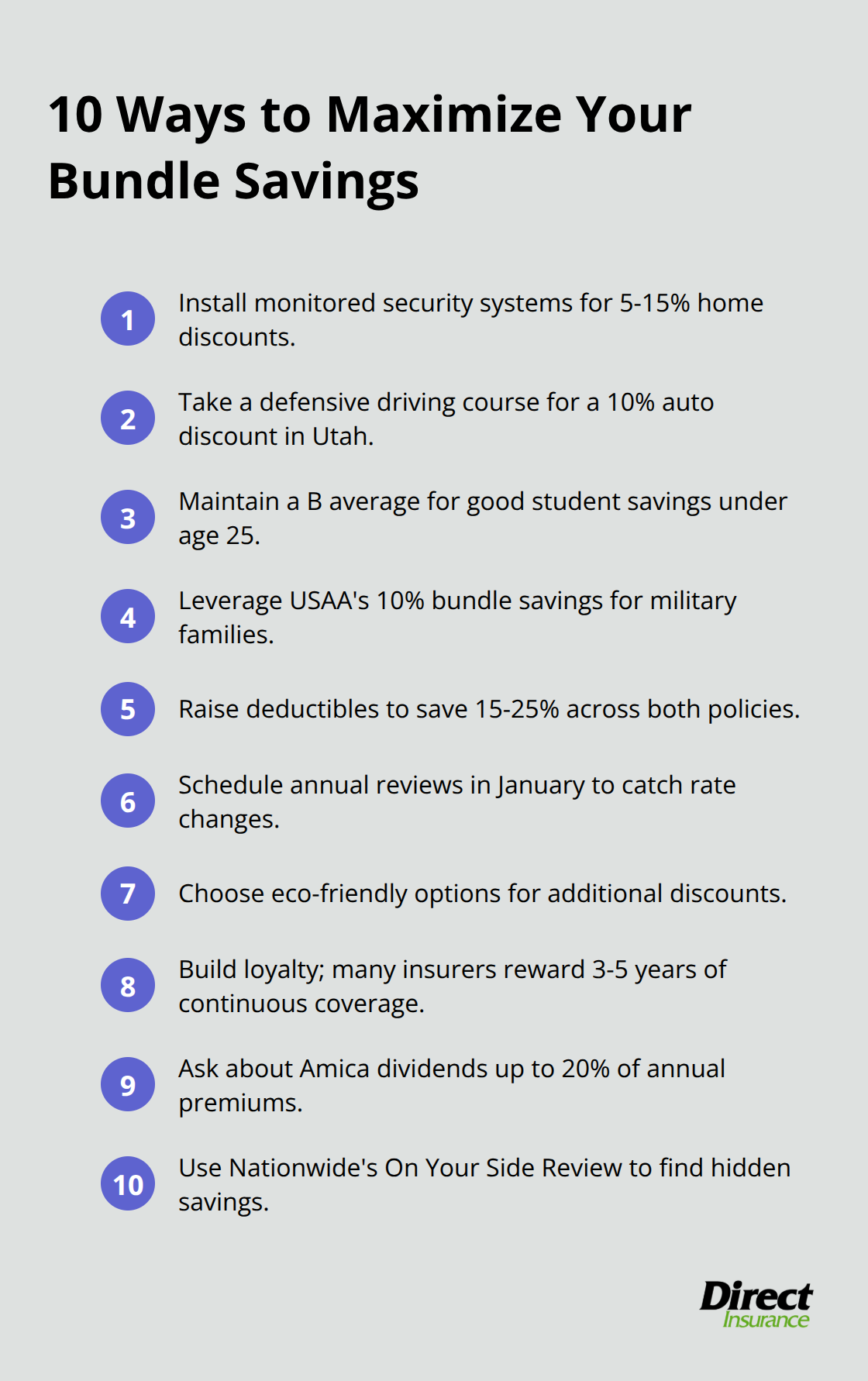

Utah residents can stack multiple discounts beyond basic bundling to save $800-1,400 annually. Start with security system installations that qualify for home insurance discounts of 5-15%. Most carriers including State Farm and Allstate recognize monitored alarm systems, smart doorbells, and security cameras as risk reducers. Auto insurance savings come from defensive driving courses that provide 10% discounts for three years in Utah. Good student discounts apply to drivers under 25 with B averages or better, while military families access USAA’s exclusive 10% bundle savings plus additional service member discounts.

Strategic Deductible Management Cuts Costs

Raise your deductibles from $500 to $1,000 to reduce premiums by 15-25% across both policies according to the National Association of Insurance Commissioners. This adjustment saves Utah families $300-600 annually while it maintains full coverage protection. American Family offers Diminishing Deductibles that reduce your deductible by $100 each claim-free year (which makes higher initial deductibles less risky over time).

Calculate your emergency fund capacity before you increase deductibles, but most households benefit from $1,000-2,500 deductibles that balance savings with manageable out-of-pocket costs.

Annual Reviews Prevent Rate Shock

Schedule annual bundle reviews in January when most carriers announce rate changes and new discount programs launch. Utah’s insurance market sees significant shifts each spring as weather patterns and claim costs influence pricing. Major life changes trigger immediate review needs including home purchases, marriage, new vehicles, or teenage drivers who join policies. Companies that increase rates above 15% annually often signal declining competitiveness (which makes comparison shopping essential for maintaining savings).

Additional Discount Opportunities

Look for eco-friendly discounts that reward hybrid vehicles, energy-efficient homes, and paperless billing preferences. Many insurers offer loyalty discounts after three to five years of continuous coverage. Professional association memberships, alumni groups, and employer partnerships frequently provide group discounts of 5-10%. Amica returns up to 20% of annual premiums in dividends to eligible policyholders, while Nationwide’s On Your Side Review helps customers find hidden savings during policy renewals.

Final Thoughts

The right home auto insurance bundle delivers substantial savings while it simplifies your coverage management. Utah families who choose quality bundles save $500-1,400 annually compared to separate policies, plus they gain streamlined claims processing and unified payment systems. Focus on total costs rather than discount percentages, since high-rate carriers often advertise impressive savings that don’t translate to actual value.

Accurate quotes require comparing identical coverage limits across multiple providers. Request written confirmation of all discounts and rate stability information before you commit to any provider. Weather patterns, state regulations, and regional risk factors affect your coverage needs and pricing options throughout Utah.

We at Direct Insurance Services shop multiple top-rated companies to find the best coverage at competitive rates for Utah families. Our team understands the specific challenges Utah residents face and provides personalized service that builds long-term relationships (something that matters when you need claims support). Start your bundle search today by requesting quotes from at least five providers to identify the best value for your specific situation.