Business Liability Insurance in Utah Explained

Utah businesses face unique liability risks that can threaten their financial stability. From slip-and-fall accidents to professional errors, these incidents can result in costly lawsuits.

We at Direct Insurance Services understand that navigating business liability insurance Utah options can feel overwhelming. This guide breaks down everything you need to know about protecting your company in the Beehive State.

What Business Liability Insurance Covers in Utah

General Liability Protection for Third-Party Claims

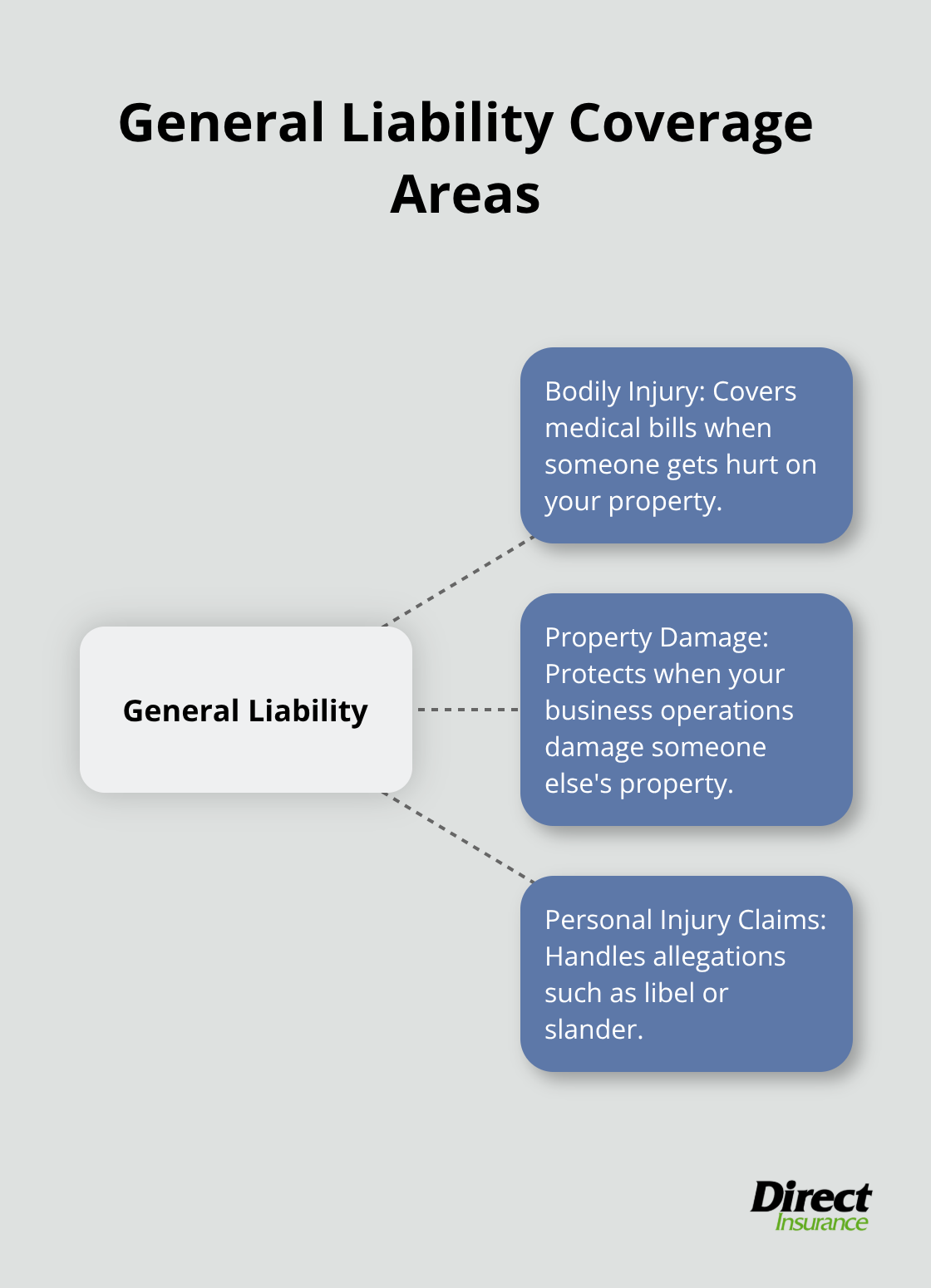

General liability coverage protects Utah companies from bodily injury and property damage claims that can bankrupt operations overnight. Utah businesses pay an average of $98 monthly for this protection, slightly below the national average. When customers slip on your premises or employees accidentally damage client property during service calls, general liability covers medical bills, repair costs, and legal defense expenses up to your policy limits.

This coverage handles three primary areas: bodily injury (when someone gets hurt on your property), property damage (when your business operations damage someone else’s property), and personal injury claims (such as libel or slander allegations). The standard coverage recommendation for most Utah small businesses is $1 million per occurrence and $2 million aggregate.

Professional Liability for Service-Based Businesses

Professional liability insurance becomes essential for service-based businesses like consultants, accountants, and IT professionals. Employment discrimination charges continue to rise across industries, demonstrating the increasing need for professional liability protection.

This coverage protects against allegations of errors, omissions, or failure to deliver promised services, even when you follow proper procedures. IT consultants face particular risks related to data security breaches and client system failures (making this coverage non-negotiable for tech professionals). Professional liability covers legal defense costs and settlements when clients claim your services caused financial harm.

Product Liability Coverage for Manufacturing Companies

Manufacturing companies need product liability coverage to handle claims from defective products that cause injury or property damage. Utah manufacturers face unique exposure since defective product claims carry a two-year statute of limitations compared to four years for general injury claims.

This coverage protects when products malfunction and cause harm after leaving your facility. The shorter statute of limitations means manufacturers must respond quickly when incidents occur (swift documentation becomes vital for claim resolution). Product liability extends beyond manufacturing defects to include design flaws and inadequate warning labels.

Understanding these three liability types helps you identify which coverage areas apply to your specific Utah business operations and potential risk exposures.

Utah-Specific Business Liability Requirements and Considerations

Utah operates without mandatory general liability insurance requirements for most businesses, but this freedom creates dangerous gaps that smart owners address proactively. Most municipalities don’t legally require general liability coverage, but specific local regulations may apply depending on your location and business type. Electricians represent a notable exception – they must carry minimum limits of $300,000 per occurrence to maintain their licenses (professional boards impose their own insurance mandates beyond state requirements).

Workers’ Compensation Stands as Utah’s Strictest Requirement

Utah requires all employers with one or more employees to carry workers’ compensation insurance, which makes this the state’s most rigid insurance mandate. The Utah Labor Commission tracks workplace injury statistics, with the majority occurring in private sector businesses. Sole proprietors without employees remain exempt, but the moment you hire your first worker, compliance becomes mandatory. Penalties for non-compliance include substantial fines and potential civil lawsuits that far exceed premium costs.

High-Risk Industries Face Elevated Premium Pressures

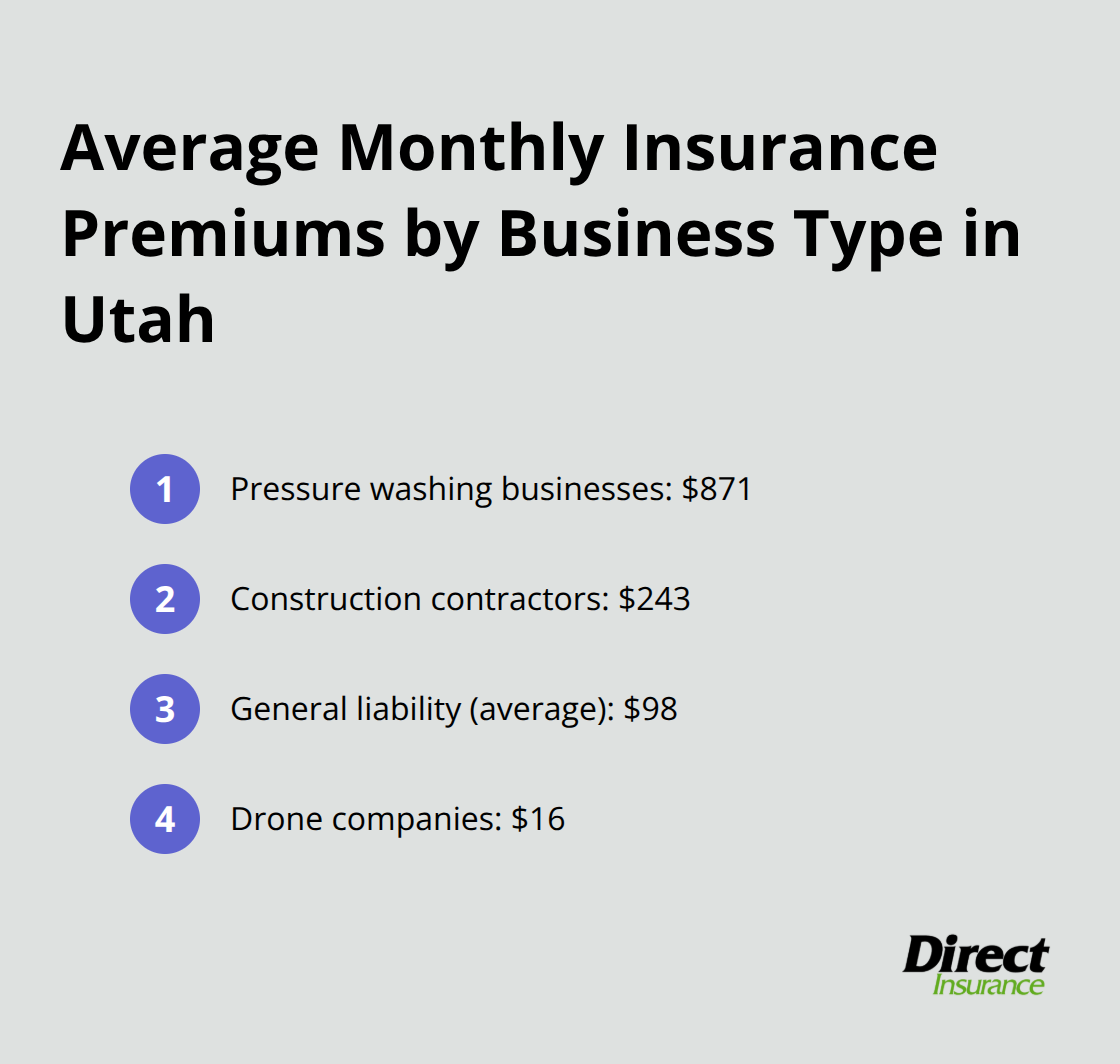

Construction contractors pay average monthly premiums of $243, while pressure washing businesses face extreme costs that average $871 monthly due to slip hazards and property damage risks. These dramatic variations highlight how industry classification directly impacts your insurance costs. Drone companies enjoy the opposite extreme, with premiums as low as $16 monthly, which reflects their minimal physical interaction risks. Utah’s diverse economy means your industry determines your insurance strategy more than any other factor.

Local Settlement Patterns Favor Comprehensive Coverage

Utah courts operate under a four-year statute of limitations for personal injury claims, which gives plaintiffs extended time to file lawsuits against your business. This extended timeline increases your exposure period compared to states with shorter limitations. The combination of Utah’s growing population and business-friendly environment creates more opportunities for liability incidents (making adequate coverage limits essential for long-term business survival).

These state-specific factors directly influence how you should structure your liability coverage and what limits provide adequate protection for your Utah business operations.

How to Choose the Right Business Liability Coverage

Utah businesses must assess their specific risk exposures and operational realities to select proper liability coverage. Companies need to examine their daily operations, customer interactions, and potential failure points that could generate lawsuits. High-traffic retail locations face slip-and-fall risks that require higher bodily injury limits, while consultants need robust professional liability coverage for errors and omissions claims. The Hartford leads Utah providers with a MoneyGeek score of 4.6 out of 5 and average monthly premiums of $86, while NEXT offers the most affordable option at $84 monthly. Coverage adequacy matters more than price differences for your specific risk profile.

Match Coverage Limits to Your Asset Exposure

Standard recommendations of $1 million per occurrence and $2 million aggregate work for most small businesses, but high-asset companies need higher limits to protect their wealth. Construction contractors pay $243 monthly due to elevated risk levels, which makes adequate limits essential for financial survival. Deductibles create immediate out-of-pocket costs when claims occur, so balance lower premiums against your cash flow capacity during crisis situations. Utah’s statute of limitations varies by case type, with some as short as six months while serious criminal offenses have no time limit, making comprehensive limits important for ongoing protection.

Evaluate Multiple Quotes from Different Providers

Business owners should collect multiple quotes and review policy terms before making decisions. Premium costs vary dramatically by industry – pressure washing businesses face average monthly premiums of $871 while drone companies pay as low as $16 monthly. These variations reflect different risk exposures and claim frequencies across industries. Compare not just prices but also coverage exclusions, claim handling procedures, and financial stability ratings of insurance companies.

Work with Local Insurance Professionals

Utah-based agents understand local court patterns, industry risks, and regulatory requirements better than online-only providers. These professionals know which insurers handle Utah claims efficiently and which companies create payment delays during critical periods. They can obtain coverage within hours using digital platforms while providing ongoing support when incidents occur. Local agents also help businesses navigate Utah’s specific requirements (such as the $300,000 minimum for licensed electricians).

Final Thoughts

Utah business owners face significant liability risks that require proactive insurance plans. The state’s four-year statute of limitations for personal injury claims extends your exposure period, while industry-specific requirements like the $300,000 minimum for electricians create additional compliance obligations. Premium costs vary dramatically by profession, from $16 monthly for drone companies to $871 for pressure washing businesses (making proper risk assessment essential).

Business liability insurance Utah coverage protects your company’s financial future when accidents, professional errors, or product defects generate costly lawsuits. The combination of general liability, professional liability, and product liability coverage addresses the primary risks that face Utah businesses across all industries. Proper coverage starts with multiple quotes from reputable providers and policy term comparisons beyond just premium costs.

Document your business operations thoroughly and maintain clean claims history to secure better rates over time. Local professionals provide advantages that online-only providers cannot match through their understanding of Utah’s unique business environment and regulatory requirements. We at Direct Insurance Services shop multiple top-rated insurance companies to find the best coverage at competitive rates for Utah businesses.